- Buysiders

- Posts

- A $100 Billion Week

Together with

Good morning! We have had the hottest week in M&A history since May 2021, right when everyone is gearing up for their vacations. Awesome. But don’t worry, you got allocated 1 share of Figma, so you can probably retire now, right?

Over $115 billion of M&A was announced this week, with the largest deal of the year also being announced.

Additionally, OpenAI is looking to do a share sale at a $500 billion valuation, and BofA is joining other banks in cracking down on on-cycle recruiting.

If you feel like you’re jumping on the crazy train, just wait until you see the deals we cover this week:

Union Pacific to acquire Norfolk Southern for $71.5 billion.

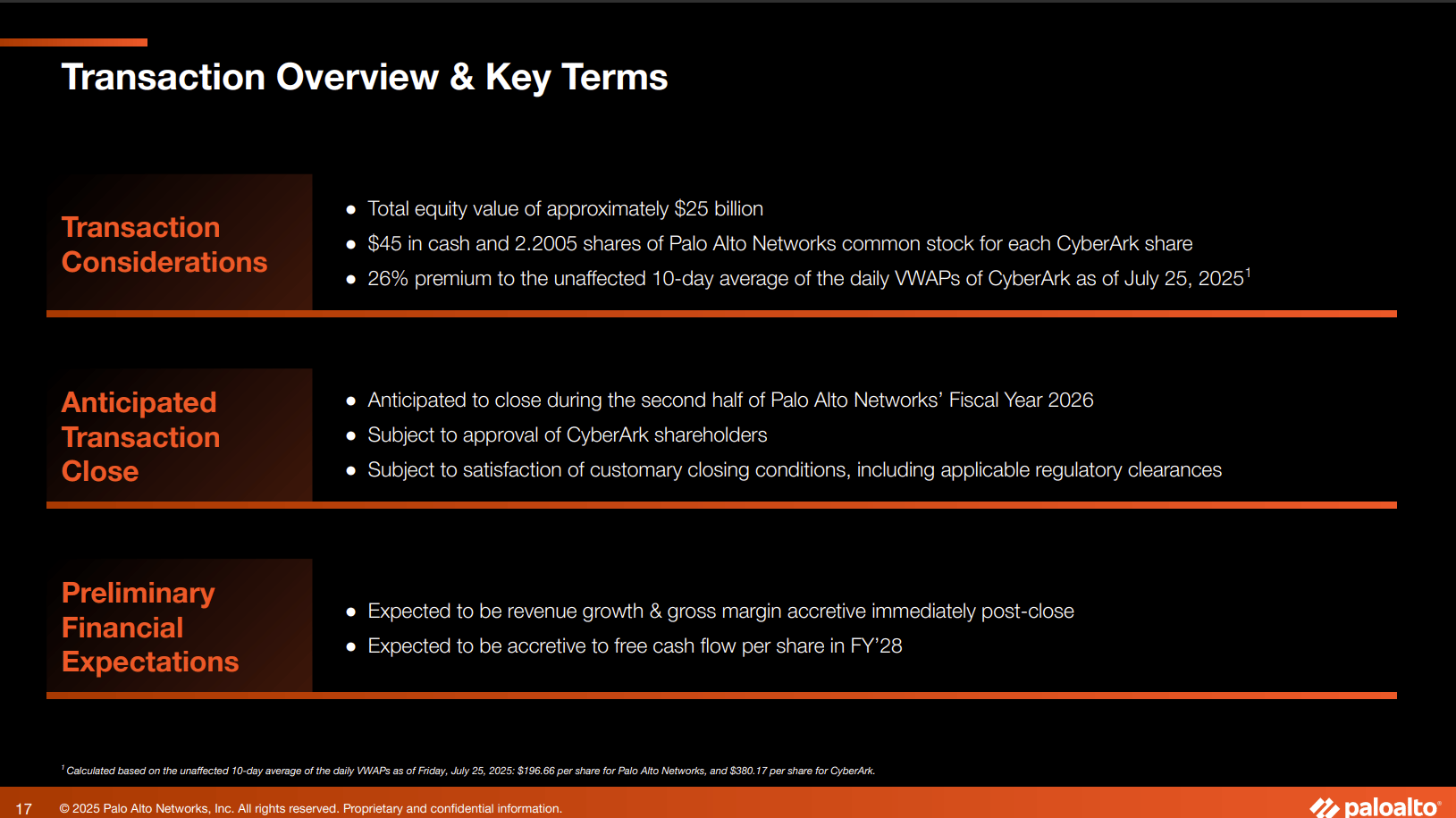

Palo Alto Networks to acquire CyberArk for $25 billion

Baker Hughes to acquire Chart Industries for $13.6 billion

Learn equity comp strategies from 2,000+ PE-backed companies in Carta’s new PE Executive Equity Report. Download it here.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

The Little Railroad That Could

In the immortal words of the Prince of Darkness - ALL ABOARD!

Union Pacific just took the express train to the top of the league tables after it announced the largest deal of the year, its $71.5 billion acquisition of Norfolk Southern.

The deal creates the United States’ first transcontinental railroad since we stopped going through Promontory Summit in 1904.

The combined company will generate over $18 billion of EBITDA and cover over 50,000 miles of track. At a $71.5 billion valuation, Union Pacific is paying ~$3.7 million per mile of track, or 13x EBITDA, whichever keeps your train on the rails.

Now let’s point ourselves on the valuation track. The deal is structured at an implied valuation of $320 per share, which represents a 25% premium to the 30-day VWAP.

The consideration consists of 72% stock at a 1:1 exchange ratio and 28% cash funded through existing cash on hand and some new debt.

If you have followed along long enough, you will know what I am going to call out next…the significant increase in Debt / EBITDA ratio and the associated pausing of share repurchases. This may give investors some pause as it tends to with these old economy businesses. So, we have to take a look at how both stocks have traded as a result.

First, Union Pacific is down ~5% for the month and ~3% since the transaction was announced.

It is likely that some shareholders saw this deal as more empire building and a less efficient use of capital than share buybacks.

Additionally, it is important to note that a company typically does share buybacks when it believes its shares are undervalued. Turning these off and using shares as a currency would send a signal to the market the shares are at least fairly valued, not exactly recipe for stock price appreciation.

On the Norfolk Southern side of the tracks, its share price is up ~8% over the month to $279 per share.

If you paid attention in your corporate finance class, or have been reading this newsletter ;ong enough, you will probably understand why the shares are not at $320 yet, nor are they likely to ever get there.

Remember, public market shareholders always price in some risk that the transaction doesn’t close. In fact, Union Pacific and NS don’t even expect the transaction to close until early 2027…

All in all, this deal shows that sometimes deals that were on the M&A wishlist for years just take the right market timing to work. What mega deal comes next? I couldn’t tell you, but with $100 billion of M&A announced this week, anything is on the table.

NEWS ROUNDUP

Top Reads

PRESENTED BY CARTA

So… Who Really Gets The Equity In PE-Backed Companies?

Compensation strategies at private equity-backed companies aren’t one-size-fits-all. In this multi-trillion dollar industry, incentive structures can make or break outcomes.

Read Carta’s PE Executive Equity Report to learn how over 2,000 private equity-backed companies align equity with performance:

Trends in carry, co-investment, securities, and vesting schedules

Why incentives are increasingly tied to value creation

How much equity CEOs are getting (spoiler: the median is over 2%)

If you’re a PE investor, GP, or portfolio leader, this report is your cheat code.

STRATEGIC DEAL OF THE MONTH

Palo Alto Networks Completes its Growth Ark

Since we’ve already covered the old economy in this issue, let’s jump to something sexier. After all, it’s pretty straightforward that more track = better business. The cloud and all its infrastructure? Much easier to understand… right?

Well, put on your raincoats because we have a cloud deal that really made it rain this week.

Who’s the rainmaker? Palo Alto Networks, which announced the second-largest deal of the week at a measly $25 billion with its acquisition of CyberArk.

I’ll be honest - I had never heard of these two companies until I started to look into this deal, which is probably how most of you feel when I talk about some random old economy deal, so don’t worry…it happens to the best of us (me).

The deal itself is structured somewhat similarly to the Union Pacific x Norfolk Southern deal, where the consideration is a mix of cash and stock, with CyberArk shareholders receiving $45 per share, paid in cash and 2.2005 Palo Alto shares for their trouble. The deal represents a 26% premium to the 10-day VWAP.

The deal is expected to be revenue and gross margin accretive immediately (read: at least one company has negative EBITDA) but should be free cashflow accretive by FY’28.

Interestingly, CyberArk has actually traded off 6% since the deal was announced. Not the outcome that Palo Alto Networks was hoping for when it announced the deal and also not a good sign for this one getting over the line at the agreed price either.

The good news is Palo Alto Networks has performed worse and has dropped 16% in the past week…talk about going off the rails.

The share price performance of both companies after the deal was announced likely means that both sides will have to come to the table to negotiate a different structure.

They say the best compromise is where neither party is happy (great advice from someone who just got married) but given this appears to be a deal of opportunity not necessity, both sides may be happy if they just walk away.

INT’L DEAL OF THE MONTH

Baker Hughes Charts a Course

Listen, you guys may not find this as exciting as I do, but getting to write about ~$115 billion of transactions, all of which have investor presentations, is literally something I dream about.

To round out our deals this month, Baker Hughes is buying Chart Industries for $13.6 billion in an all cash deal valued at $210 per share.

The deal is being done at 9x 2025E EBITDA, which itself isn’t totally offensive until you realized that is fully synergized.

Given they tell us the expected synergies are $325 million, that implies the actual multiple is closer to 11-12x. That still isn’t offensive, but it is a full valuation to say the least.

Assuming you don’t want to learn the ins and outs of the piping business, we can skip to the good part.

Baker Hughes is up big over the month (~12%) but is down ~6% since the transaction was announced (ouch). The price has since stabilized though, so shareholders may be coming around on the transaction.

Absolute screamer on the other hand for Chart though, which is up 21.6% over the month. Go ask your intern to point to the graph and tell you when the deal was announced.

Similar to the Union Pacific deal, you can see that the Chart shareholders are still pricing in some potential that the deal does not close, which is why the price has stabilized around $200 per share rather than the full $210 that is being offered.

All in all, it appears that Baker Hughes is charting a course towards closing this one, and, honestly, it may be the only one of the three that actually gets over the line.

What'd you think of today's newsletter? |