- Buysiders

- Posts

- A Song of Networks and Streams

A Song of Networks and Streams

Plus: M&A Goes Plus Sized and Vodacom builds in Africa

Short Squeez

December 16, 2025

Together with

Good morning! Just as I thought I could coast it into the holidays, it turns out that another mega deal dropped…which turned into a bidding war. Great if you are a WBD shareholder, awful if you write a newsletter that has to be redone to account for the deal changing.

Of course, we also have Elon being Elon (I feel like I say that once a week), as he runs at the largest IPO of all time, looking to raise $30 billion at a $1.5 trillion valuation in 2026 for SpaceX.

As you hopefully dodge staffings heading towards the holiday season, here are some deals that made my nice list going into the (hopeful) winter slowdown.

Warner Bros bidding war heats up as Paramount re-enters the fray

M&A goes plus sized as DestinationXL and FullBeauty merge

Vodacom expands in African presence acquiring an additional 20% stake in Safaricom

Deal teams are cutting diligence time by 75% with the most advanced AI agent for Excel on the market. See how F2 accelerates analyst work in PE and credit.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

Game of Thrones - A Song of Networks and Streams

Years after Game of Thrones ended, Warner Bros finds itself in the middle of its own game as it becomes the hottest takeover target on the Street.

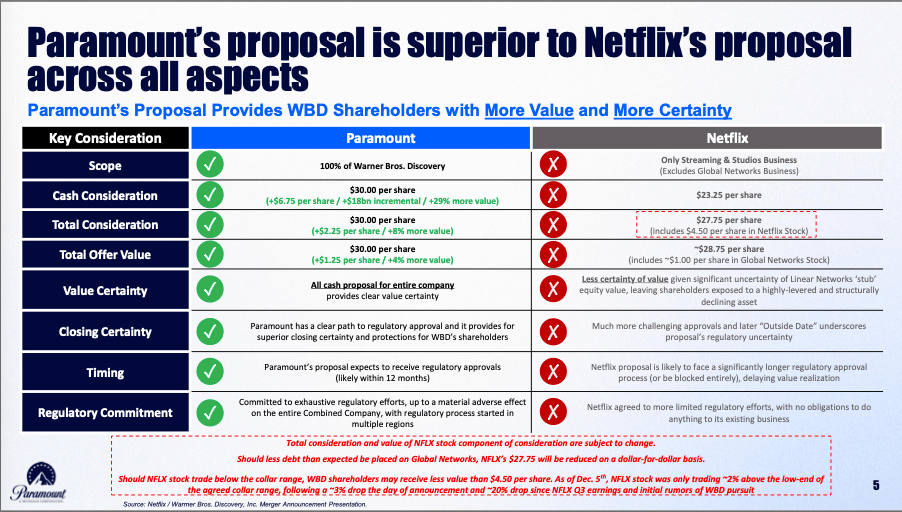

On Dec. 5, Netflix announced it had agreed to buy WBD’s TV and film studios and the HBO Max streaming service for about $72 billion in equity value, or $82.7 billion including debt, which is an eye-popping 14.3x 2026E EBITDA (including synergies).

The cash‑and‑stock offer will give each WBD shareholder $23.25 in cash plus roughly $4.50 of Netflix stock per share, valuing the stock at $27.75, a cool 121% premium to WBD’s price before rumors emerged.

Netflix expects $2 billion - $3 billion in cost savings (that’s a lot LinkedIn updates) within three years. In fact, the CFO of Netflix even said that a majority of the $2.5 billion of synergies would come from SG&A reductions on the announcement call.

The deal hinges on WBD spinning off its Discovery Global networks by Q3 2026, but regulators are already sharpening their pencils: antitrust experts warn of major pushback given Netflix’s dominance.

Investors liked the concept (shocking that a 120% premium was enough). WBD shares rose 3.2% while Netflix slipped 0.2%.

But not all romances play out like they do in the movies…and this break up could cost ~$3 billion.

Who is our other suitor? Paramount Skydance.

On Dec. 8 it lobbed a $30‑per‑share all‑cash offer, which is roughly $108 billion including debt, financed by Jared Kushner’s Affinity Partners, Middle Eastern sovereign wealth funds and backstopped by the Ellison family.

Paramount claims its bid offers WBD investors $18 billion more cash than Netflix’s proposal and promises fewer regulatory headaches and a rosier future for Hollywood.

WBD’s board said it would evaluate the offer but urged shareholders to take no action yet. The premium is genuinely offensive – 139% over WBD’s pre‑rumor price – and the market reacted accordingly: WBD shares jumped another 5.3%, Paramount’s rose 7.3%, and Netflix slid 4%.

The market has made it clear that Netflix must up its price, with shares now trading just shy of $30 per share. Implying that Paramount is the leading bidder until Netflix comes back with something better.

Paramount touts potential synergies of about $6 billion, but Netflix’s co‑CEO has cheekily asked where those synergies come from (“cutting jobs?”)…but you know, glass houses.

Antitrust hawks say a Paramount‑WBD tie‑up would be a “five‑alarm fire” given the combined broadcast and cable footprints, while the Netflix deal would consolidate streaming and studio assets. So really, the only people winning here are the lawyers.

Wall Street now has front‑row seats to a rare, high‑stakes auction playing out on their Bloomberg terminals rather than the Silver Screen.

Netflix’s offer mixes cash and stock and offers a safety net in the breakup fee; Paramount’s is bigger and all‑cash but relies on political favor and Gulf capital.

Netflix says bundling HBO Max with its streaming service will lower subscription costs and create more jobs, whereas Paramount argues its takeover would safeguard theatrical releases and support Hollywood unions.

Expect months of lobbying, Senate hearings and industry hand‑wringing. For now, the only clear winners are M&A bankers, lawyers, and anyone who bought WBD before it shot up.

PRESENTED BY F2

Data Room to IC in 75% Less Time

Whether you're a private credit analyst spreading financials for covenant analysis, a PE associate building LBO models, or a commercial banker preparing credit committee materials, F2 handles the technical work.

The platform processes Excel models, synthesizes data room documents, integrates market sources like FactSet, and generates investment-grade materials with full transparency. Analysts and Associates reclaim their time. VPs and Principals get better prepared analysis. MDs and Partners see faster deal flow.

Used across private credit, private equity, commercial banking, and investment banking. Teams evaluate deals 75% faster while maintaining the standards investment committees demand.

Please Support Our Partners!

STRATEGIC DEAL OF THE MONTH

M&A Just Got A Little Bit Heavier

M&A has already been plus sized this year…but now plus sized is taking on M&A. After all, who doesn't prefer a Lizzo ad to a Sydney Sweeney ad?

Destination XL Group and FullBeauty Brands inked a merger of equals that will create one of North America’s largest plus‑size apparel retailers.

The deal produces the unambiguous heavyweight champion of big and tall retail. Not “inclusive.” Not “size-diverse.” Just big. Very big. The combined company will sell jeans, shirts, and athleisure to a customer base that has never once worried about European sizing.

The all‑stock deal will see FullBeauty shareholders own a voluptuous 55% of the combined company and DXL investors getting a diluted to an anemic 45%.

Together, the companies generated about $1.2 billion in net sales over the last year and expect $25 million in annual cost synergies by 2027. Adjusted EBITDA was roughly $45 million, implying the merger could lift EBITDA to around $70 million once synergies kick in.

The combined firm will operate 296 stores and command a database of 34 million households, giving it scale to negotiate better sourcing and launch new brands.

Strategically, this is more than just economies of scale. DXL dominates Big & Tall menswear, while FullBeauty runs inclusive-sizing brands like Woman Within and Roaman’s.

Together, they aim to capture the growing market for plus‑size clothing at a time when body positivity is booming and GLP‑1 weight‑loss drugs are turning customers into shape‑shifters.

DXL shares have also been hammering Ozempic, down roughly 58% year to date and trade at about $1.56, giving it a market cap of just $62 million – so partnering with FullBeauty, which emerged from bankruptcy in 2019, offers a lifeline.

This tie‑up proves size matters in more ways than one. Between Ozempic customers buying new wardrobes and plus‑size shoppers demanding more choice, DXL and FullBeauty are betting that bigger can indeed be better.

If the synergy math doesn’t work out, at least investors can console themselves by calculating just how many elastic waistbands you can buy with $25 million.

INTN’L DEAL OF THE MONTH

Vodacom Phones a Friend

I think we call all agree there are certain industries that we forget exist from time to time. For me, that one is usually telecom. I have AT&T, so I have accepted the fact that the odds of my phone working anywhere are less than 50%, and I just live life like that.

Every once in a while, though, the telecom industry decides not to completely phone it in and announces a deal that reminds you it’s still alive. I mean, just look at how fun this transaction structure diagram is!

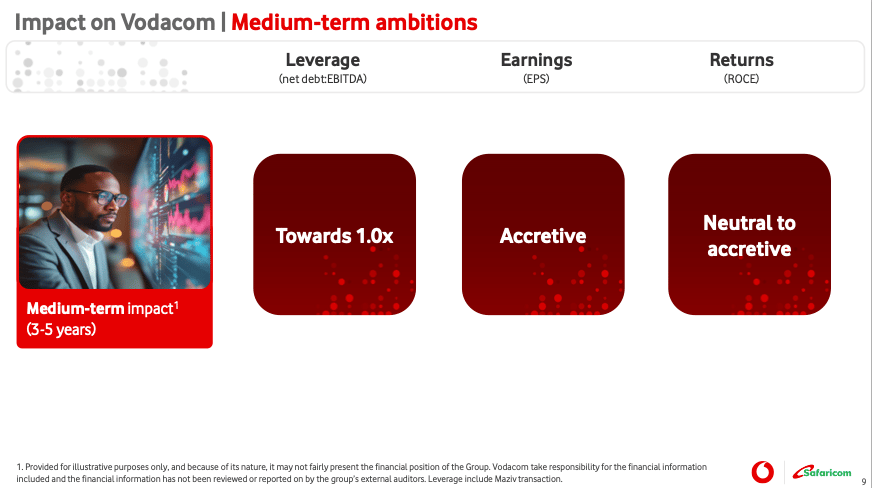

Vodacom is acquiring an additional 20% stake in Safaricom for ~$2.1 billion, bringing its total stake to just under 55%. The deal is being struck at 6.9x TEV/2026E EBITDA and is being financed by term debt.

Interestingly, Vodacom is not pitching this as a home run by any means. It is acknowledging that the returns will only be neutral to accretive, with EPS only turning accretive in 3-5 years.

Now I am sure most of you don’t care about Vodacom acquiring more shares in some random African telecom company, but these guys spit off margins that make European and American telecom companies look like charities.

One of the key drivers is M-Pesa (Safaricom’s mobile money platform) which processes billions in transaction volume, touches everything from rent to remittances, and operates with regulatory protection that fintech founders can only dream about.

Vodacom increasing its influence here isn’t flashy, but it’s smart.

The market treated it accordingly, with Safaricom shares steady to up and Vodacom investors are quietly reminded that boring emerging market infrastructure often beats whatever AI adjacent nonsense is trending this week.

This isn’t a growth story, it is a control story. Those tend to age way better.

What'd you think of today's newsletter? |