- Buysiders

- Posts

- A Well Dressed Deal

A Well Dressed Deal

Plus: Monomoy Gets Lubed Up and 3M does the most complex deal of the year.

Short Squeez

March 24, 2026

Together with

Good evening! The market is getting hammered as the war continues in the Middle East while some of the world’s largest energy infrastructure takes a beating.

Regardless, Wall Street came in hot this week, and for once, the headline deals have nothing to do with AI data centers, streaming wars, or a Japanese billionaire crying about Nvidia.

Instead, the market served up a private equity carve-out of America’s most recognizable oil change chain, a decades-long hostile takeover finally crossing the finish line, and a joint venture so structurally creative it took three press releases to explain.

Whether you’re a PE associate who just found out what a carve-out means, a strategic banker trying to explain to your MD why uniforms are “a high-margin recurring revenue business with pricing power,” or you’re just sitting in a Jiffy Lube waiting room reading this on your phone, this one’s for you.

Cintas Acquires UniFirst for $5.5 billion

Monomoy Acquires Jiffy Lube for $1.3 billion

3M and Bain Do the Most Complex Megadeal of the Year

The way sponsors execute and manage financings - private credit or broadly syndicated - has evolved. See how Termgrid enhances your financing infrastructure and boosts your deal team productivity. Request a demo today.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

A Well Dressed Deal

If you have ever tried to acquire a company that doesn’t want to be acquired, you know that patience is not just a virtue, it’s a budget line item.

Cintas and UniFirst are the two largest uniform and workwear services companies in the U.S. Think the companies that supply, launder, and deliver uniforms to factories, hospitals, restaurants, and auto shops across the country.

Cintas is the dominant player with a market cap of $72 billion. UniFirst is the scrappy number two, family-controlled, and apparently allergic to being bought.

Cintas Corporation and UniFirst Corporation announced on March 11 that they have entered into a definitive agreement under which Cintas will acquire UniFirst for $310.00 per share in cash and stock, representing an enterprise value of approximately $5.5 billion.

For those keeping score: in December 2025, UniFirst received an acquisition proposal from Cintas for $275 per share in cash, valuing the company at about $5.2 billion, which UniFirst’s board rejected.

Cintas came back with a higher number, structured the deal as part cash, part stock, and negotiated a $350 million reverse termination fee — payable if the deal dies on antitrust grounds — which apparently was the magic combination that finally got the Croatti family off the fence.

Under the terms, UniFirst shareholders will receive $155 in cash and 0.7720 shares of Cintas stock for each UniFirst share they own, representing a combined value of $310 per share based on Cintas’ closing price on March 9. RIP to your printer for this investor presentation…

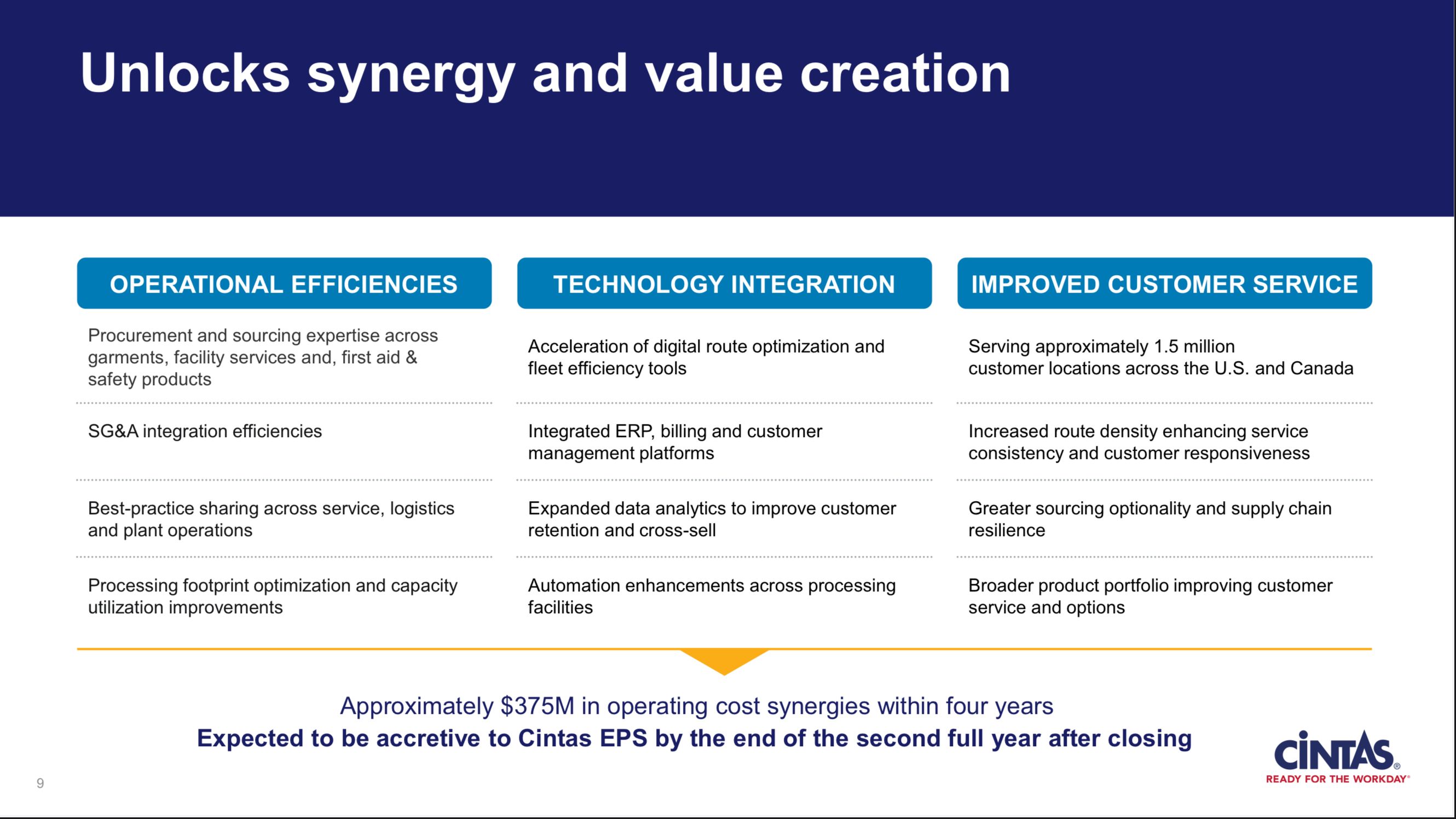

The implied total enterprise value of $5.5 billion represents a multiple of 8.0x run-rate trailing twelve months EBITDA, including approximately $375 million of operating cost synergies.

The synergies come from route optimization, plant consolidation, and procurement scale, which is a polite way of saying: when you run half of North America’s uniform delivery routes, you can probably cut some duplicate truck stops.

Here is the thing about the uniform rental business that nobody talks about at dinner parties: it is shockingly good. Cintas already generates over $10 billion in annual revenue, and the “Uniform Rental and Facility Services” segment accounts for approximately 77% of total revenue, operating on a recurring contract basis where drivers visit client sites weekly to pick up soiled uniforms and deliver clean ones. Does someone smell an LBO target next year?

Route density is everything - the more stops per mile, the more profitable each truck. Acquiring UniFirst’s routes doesn’t just add customers; it makes Cintas’s existing routes more efficient by filling in geographic gaps.

The combined company will deliver products and services to approximately 1.5 million business customers across North America. To contextualize that number: there are only about 33 million registered businesses in the United States.

Cintas and UniFirst together will be dressing, cleaning, and supplying roughly one in twenty of them. If that’s not a moat, I don’t know what is.

The regulatory situation is, shall we say, colorful (hopefully not blue like this pitch deck).

A combined Cintas-UniFirst entity would own nearly half of the market, which may require divestitures of specific local routes or branches in concentrated geographic areas. Cintas is “highly confident” on regulatory approval and has already staged a $350 million reverse termination fee as proof of conviction.

Whether that confidence is warranted or just well-dressed optimism remains to be seen. The DOJ has been known to take a close look at markets where “Big Three to Big Two” consolidation is on the table.

The transaction was unanimously approved by both boards, and entities affiliated with the Croatti family.

Pro forma leverage at closing is expected to be approximately 1.5x debt to EBITDA, preserving Cintas’s investment grade credit profile. The firms were advised by Goldman Stanley (who cares who represented who), but this will be a good one for the league tables for both.

The deal is expected to close in the second half of 2026. And somewhere in Wilmington, Massachusetts, the UniFirst family is quietly putting their lawyers on speed dial just in case.

PRESENTED BY TERMGRID

The Platform Leading PE Firms Use for Their Financing Workflows

Termgrid is how private equity sponsors, advisors, and lenders execute financings.

Their vertical-focused collaboration platform centralizes debt raises and equity co-invest processes, giving you better insights and faster execution.

With Termgrid, investment firms can:

Boost productivity: increase deal team capacity by up to 84% (see case studies here)

Reduce financing risk: access the largest financing ecosystem (1,600+ institutions and 30,000+ professionals)

Make faster, data-driven decisions: analyze terms and credit negotiations in real time

Lower transaction costs: reduce data sharing and legal inefficiencies

Build institutional knowledge: automatically capture data across relationships, transactions, and precedent terms

The best sponsors (from mid market to mega funds) are using Termgrid for their financing infrastructure. See why today.

SPONSOR DEAL OF THE MONTH

Monomoy Gets Lubed Up

For once, a PE shop buying a bunch of lube might not be just because bonus season is coming up for juniors.

Shell has been quietly trying to convince itself that owning a chain of quick-lube shops makes sense for a global oil major for twenty-four years. On March 9th, it finally stopped pretending.

Monomoy Capital Partners announced it has entered into a definitive agreement to acquire Jiffy Lube International from Pennzoil Quaker State Company — a wholly owned subsidiary of Shell USA — through its Fund V for approximately $1.3 billion.

Shell acquired Jiffy Lube in 2002 for reasons that probably seemed clever at the time: vertical integration, brand synergy, guaranteed lubricants demand, banker needed fees, nepo baby corp dev guy needed a win, and has spent the two decades since discovering what every oil major eventually discovers: owning retail is a very different business from drilling holes in the ground. Turns out the customers at a Jiffy Lube don’t care whose barrel the oil came from.

What makes this deal more interesting than a CIM you would use for modeling is that practice is the structure. Monomoy is acquiring both Jiffy Lube International — including the registered trademark and the franchisor business — and Premium Velocity Auto (PVA), identified as the second-largest Jiffy Lube franchisee, which runs more than 360 locations across approximately 20 states.

So you’re not just buying a franchise system; you’re buying the franchisor and the second-largest franchisee simultaneously, which gives Monomoy an immediate owned-and-operated base to work from while also collecting royalties from the other 1,600-plus independently-owned stores. If you squint, that is a pretty elegant platform structure (and I bet it banged on the structure chart page).

For Monomoy, this is squarely in their wheelhouse. Monomoy Founder and Co-CEO Dan Collin described it as a “complex corporate carve-out transaction,” noting that the firm has executed these for global corporations for over twenty years.

The carve-out complexity here is real: Shell’s lubricants supply agreement had to be negotiated separately, Pennzoil brand relationships had to be ring-fenced, and the franchise system needed new standalone infrastructure for everything from IT to HR to legal. None of that is simple, and most PE firms can’t actually execute it.

Monomoy’s pitch is essentially: we can. Which, given their track record, is at least credible. Don’t forget, when the spreadsheet says the deal works, you still have to make that happen in practice.

As part of the transaction, Shell’s subsidiary Pennzoil Quaker State has entered into a long-term lubricants supply agreement with Monomoy, which is Shell’s way of saying: we sold the business but we’d still like to sell you the oil that goes in the cars.

You have to respect the hustle. Shell loses the headache of running a retail franchise, keeps the lubricants volume, and pockets $1.3 billion. Monomoy gets a household brand with 19 million annual customers, a turnaround opportunity, and locked in supply to support its business.

The deal is expected to close in the second half of 2026, pending regulatory approval. In the meantime, if you walk into a Jiffy Lube and the guy under your car is in a suit, it means Monomoy underwrote some aggressive cost cutting.

COMPLEX DEAL OF THE MONTH

3M and Bain Do the Most Complex Deal of the Year

There is a category of M&A transaction that defies easy description. It is not a straight acquisition. It is not a merger. It is a simultaneous acquisition-and-contribution joint venture where one party buys an outside business, folds in an existing one to create a new entity, while receiving cash proceeds on the same day they write a check. It is the M&A equivalent of a Rubik’s Cube. 3M and Bain Capital solved it on March 19th.

3M announced that it has entered into a definitive agreement to acquire Madison Fire & Rescue from Madison Industries, in partnership with Bain Capital, for $1.95 billion and that it will be forming a new joint venture focused on fire, safety, and rescue solutions.

Here is where it gets interesting: 3M and Bain Capital will establish a new joint venture in which 3M will contribute its existing Scott Safety business, receive $700 million of cash proceeds upon closing, and own 50.1% of the new company, with Bain Capital owning 49.9%.

Read that again. 3M is spending money and receiving money on the same transaction.

It is buying a fire and rescue equipment company, contributing its own safety business into the deal, and walking away with $700 million in cash on day one while retaining majority ownership of the combined entity.

Credit where it’s due, whoever modeled this one earned their carry.

Madison Fire & Rescue’s portfolio includes Amkus and Holmatro, makers of hydraulic and battery-powered rescue tools (the ones you see cutting people out of cars on the highway); Task Force Tips, a maker of high-performance nozzles for fire hoses; and Waterax, which makes mobile water pumps for wildland firefighting. These are not glamorous products.

They are the products that exist specifically for the moments when everything else has gone wrong. Scott Safety, which 3M acquired in 2017 for approximately $2 billion, makes self-contained breathing apparatus systems, the tanks and masks that firefighters wear when they enter burning buildings.

Together, the portfolio covers essentially the entire toolkit of a first responder: the truck, the hose nozzle, the breathing apparatus, the rescue cutters. If you are a fire department purchasing director, this new JV is now your one-stop shop for almost everything except the actual firefighter.

The acquisition allows 3M to expand its safety and fire protection product offerings, which are high-margin businesses that can provide steady cash flow, while Madison Fire & Rescue’s emergency vehicle manufacturing business complements 3M’s existing personal protective equipment lines.

For Bain, the story is simpler: they get nearly half of a cash-generative, defensible industrial business with a captive government customer base (every fire department in the country), funded largely by 3M’s asset contribution and the deal’s cash-in structure.

In a week dominated by carve-outs and consolidations, the 3M-Bain deal stands out as the most structurally interesting. It is not the biggest number on the tape. But it is the one your corporate finance professor would have used as a case study, if your corporate finance professor had ever spent time thinking about fire trucks, which, statistically: they probably have not.

NEWS ROUNDUP

Top Reads

Shell sells Jiffy Lube to Monomoy Capital Partners for $1.3 billion

3M and Bain Capital to buy Madison Fire & Rescue for $1.95 billion

Cintas-UniFirst faces antitrust scrutiny as combined entity nears 50% market share

Megadeal volume up 57% year-over-year as 2026 M&A hits full stride

Middle market M&A set to rise in 2026 as PE funds sit on $2.1 trillion of dry powder

What'd you think of today's newsletter? |

*Partner sponsored post.