- Buysiders

- Posts

- Denny’s Hits a Grand Slam

Denny’s Hits a Grand Slam

Plus: A $12.8 billion shale merger and Bending Spoons revives AOL.

Short Squeez

November 10, 2025

Together with

Good morning! Mamdani is officially mayor, so hopefully you made some money on Kalshi betting on him. If you find a good realtor in Miami, please let us know, we are also in the market.

On the flip side, Elon just had a $1 trillion pay package approved… but even with his $483 billion net worth, he still isn’t the richest man in history. That title belongs to John D. Rockefeller, the railroad titan whose fortune was worth about $630 billion (inflation-adjusted) back in 1913.

If you’re feeling left out of the trillionaire club, don’t worry, Michael Burry and Deutsche Bank are already betting it all ends badly: shorting AI (we’ve definitely seen this movie before). So whether you’re stressing about the AI bubble or getting margin-called on your shorts, here’s your reprieve for the month:

Denny’s gets acquired for a 52% premium

Bending Spoons Resurrects AOL

SM Energy and Civitas Resources merge for $12.8 billion

9fin delivers debt market intelligence 60 minutes before competitors move. Learn how.

First time reading? Sign up here.

Have feedback? Respond here.

PE DEAL OF THE MONTH

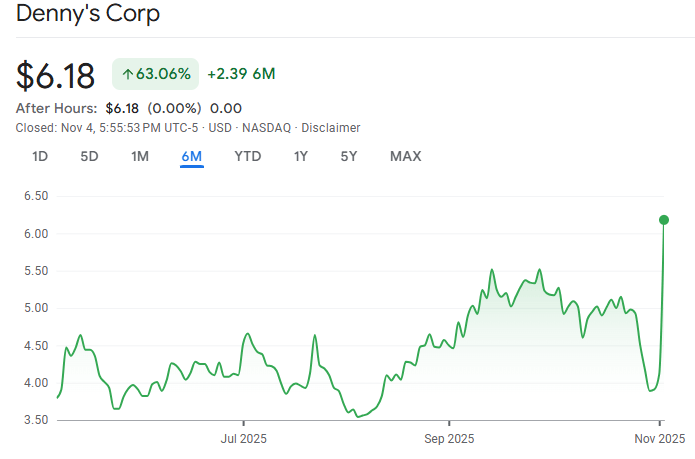

Denny’s Hits a Grand Slam

Late‑night diners are apparently the hottest asset class. Denny’s Corporation struck a deal to go private in an all‑cash transaction valued at about $620 million. (And no, not by Roark finally!)

Shareholders will receive $6.25 per share, a 52.1% premium to the pre‑announcement close and 36.8% above the 90‑day volume‑weighted average (do I smell overpayment or is that my bacon burning?).

The buyout group is an eclectic trio: TriArtisan Capital Advisors, the private‑equity firm behind P.F. Chang’s and other full‑service dining concepts; Treville Capital Group, an alternative‑asset manager with a knack for bespoke financing; and Yadav Enterprises, which runs about 550 restaurants and is one of Denny’s largest franchisees.

The board launched a broad auction, contacting more than 40 potential buyers before deciding that the TriArtisan‑led offer maximized value (shocking that the 52% premium offer got approval).

Management said the consortium’s restaurant know‑how and access to capital outweighed other bids and that the cash price provides certain value for shareholders (once again, like a 52% premium).

It’s pretty clear why the 71‑year‑old American staple has attracted private‑equity interest. Denny’s derives 96% of its revenue from franchised restaurants.

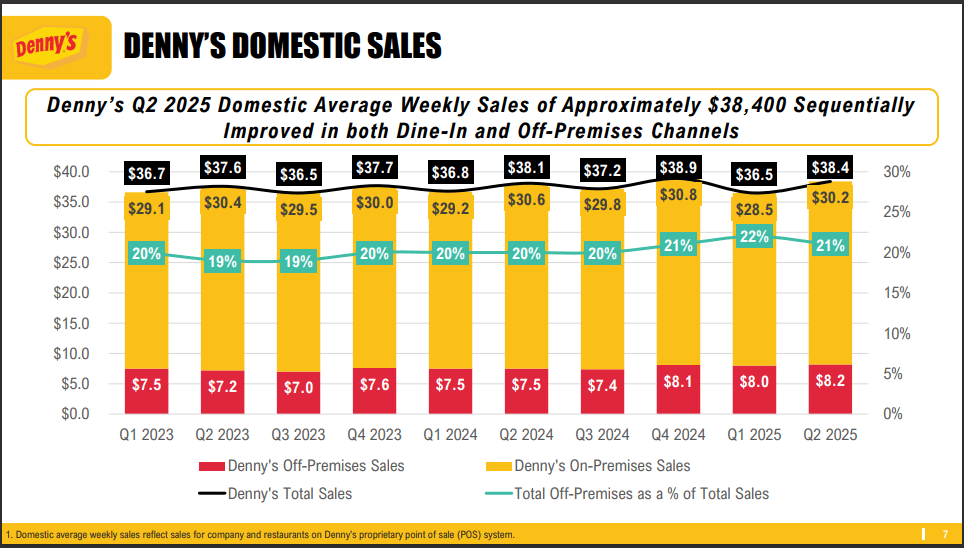

It also enjoys an off‑premises sales mix of ~20% and aims for 5% to 7% adjusted EBITDA growth with 3% net unit growth, partly through its newer Keke’s breakfast chain.

Yadav, which has a 30‑year track record operating Denny’s franchises, will bring operational expertise, while TriArtisan will leverage its experience with P.F. Chang’s and other brands to invest in digital ordering and off‑premises capabilities. Because who doesn’t want a lukewarm grand slam breakfast delivered?

CEO Kelli Valade said the company had made progress across both brands but saw the sale as a way to deliver “significant, near‑term and certain cash value” to shareholders. Hard hitting analysis at a 52% premium.

Only time will tell if TriArtisan is cooking or getting cooked.

PRESENTED BY 9FIN

The Credit Intelligence Platform Buyside Investors Trust

When credit markets move, seconds matter. 9fin delivers breaking alerts 30–60 minutes ahead of the competition, giving you time to act, not just react.

From CLO impact to covenant risks, 9fin offers real-time restructuring intel, private credit data, and deep distressed coverage; all backed by 20 years of historical data.

AI-powered tools compress hours of research into minutes:

Comparable analysis

Earnings breakdowns

Credit screening

Thousands of buyside credit investors rely on 9fin to evaluate risk and seize opportunities before the rest of the market.

Please Support Our Partners!

NEWS ROUNDUP

Top Reads

Apollo Global Management will invest $6.5 billion for a 50% stake in the world's largest wind farm

Plymouth Industrial REIT taken private by Ares and Makarora for $2.1 billion

Blackstone partners with Humain for $3 billion data center venture

Arlington Capital raises $6 billion defense fund focused on national security

Andreessen Horowitz aims to raise $10 billion to back AI and defense tech start-ups

STRATEGIC DEAL OF THE MONTH

You’ve Got (Bent) Mail

Usually bending spoons is a parlor trick reserved for bad magicians and the psychic your marketing girlfriend sees because Mercury is in retrograde, but in this case it’s also AOL’s lifeline.

Bending Spoons, the Milan‑based tech studio behind Evernote and Remini, reached a deal to acquire AOL from Yahoo and arranged $2.8 billion in debt financing to pay for the purchase and fuel further R&D and M&A.

People familiar with the matter peg the purchase price at around $1.4 billion, leaving plenty of dry powder to overhaul the 1990s stalwart and maybe resurrect those classic trial CDs.

The financing is split between Term Loan A and Term Loan B facilities plus a new revolving credit line and is backed by a syndicate that reads like a Davos seating chart: Banco BPM, BNP Paribas, Crédit Agricole CIB, Goldman Sachs, HSBC, Intesa Sanpaolo, JP Morgan, Mitsubishi UFJ, Mizuho, Société Générale, UniCredit and Wells Fargo.

CEO Luca Ferrari calls AOL “iconic” and notes it still boasts about 30 million monthly and 8 million daily users, ranking among the top ten email providers. Remember your AOL screenname from 10 years ago? I don’t.

Bending Spoons plans to invest heavily: the company never sells the businesses it buys and typically overhauls their technology, redesigns the interface, accelerates feature releases and optimizes marketing and monetization.

Its portfolio already includes Brightcove, Evernote, WeTransfer, Komoot, Meetup, Remini and StreamYard, and together these products serve over 300 million monthly users and 10 million paying customers.

With AOL expected to close by year‑end 2025, Ferrari says the acquisition “strengthens our ability to continue acquiring and transforming digital businesses worldwide with a long‑term view,” adding that the support of so many banks endorses Bending Spoons’ strategy.

There is speculation that a U.S. listing could be next, but for now the only bell ringing you’ll hear is the iconic “You’ve Got Mail” greeting.

DEAL OF THE MONTH

Frack to the Future

All cowboys love a shootout, even the shale ones.

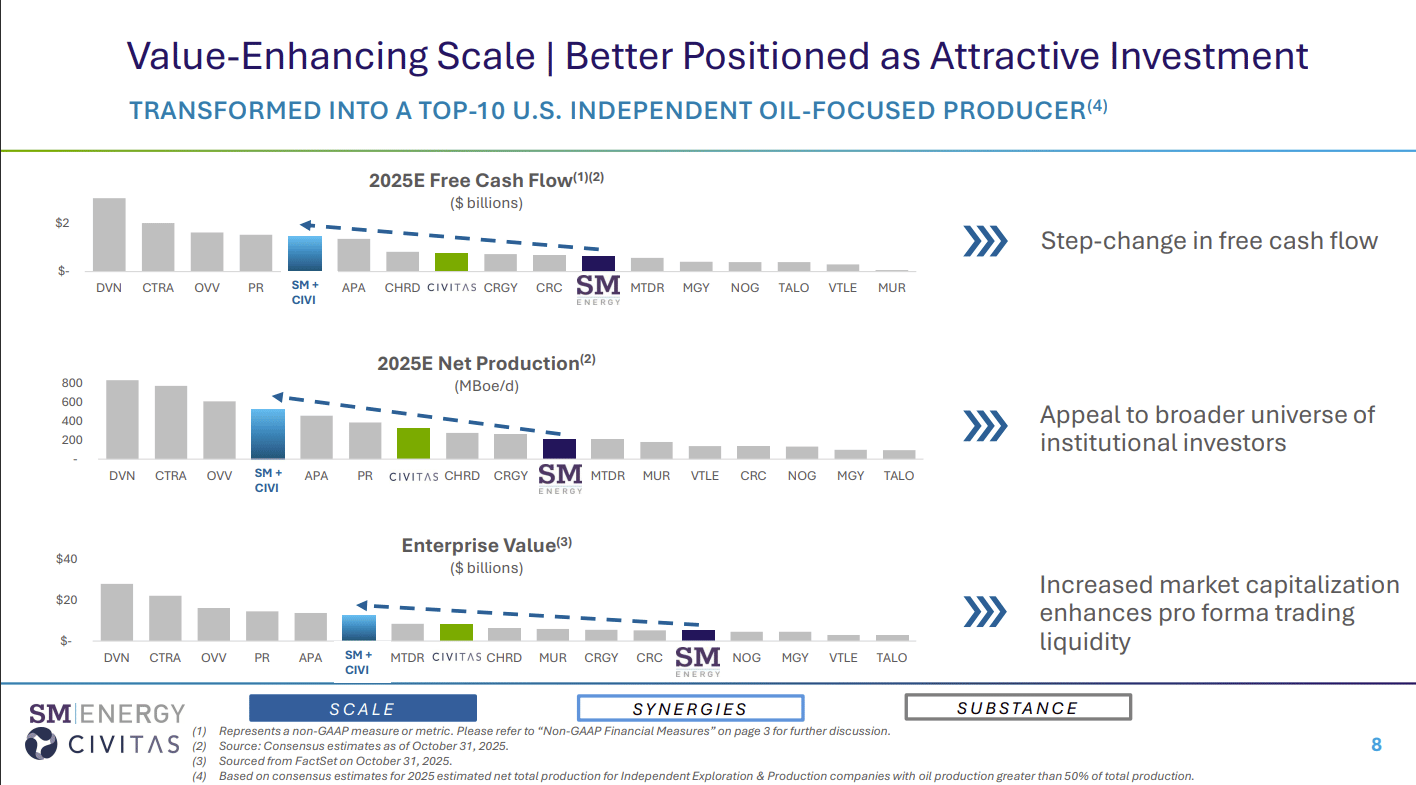

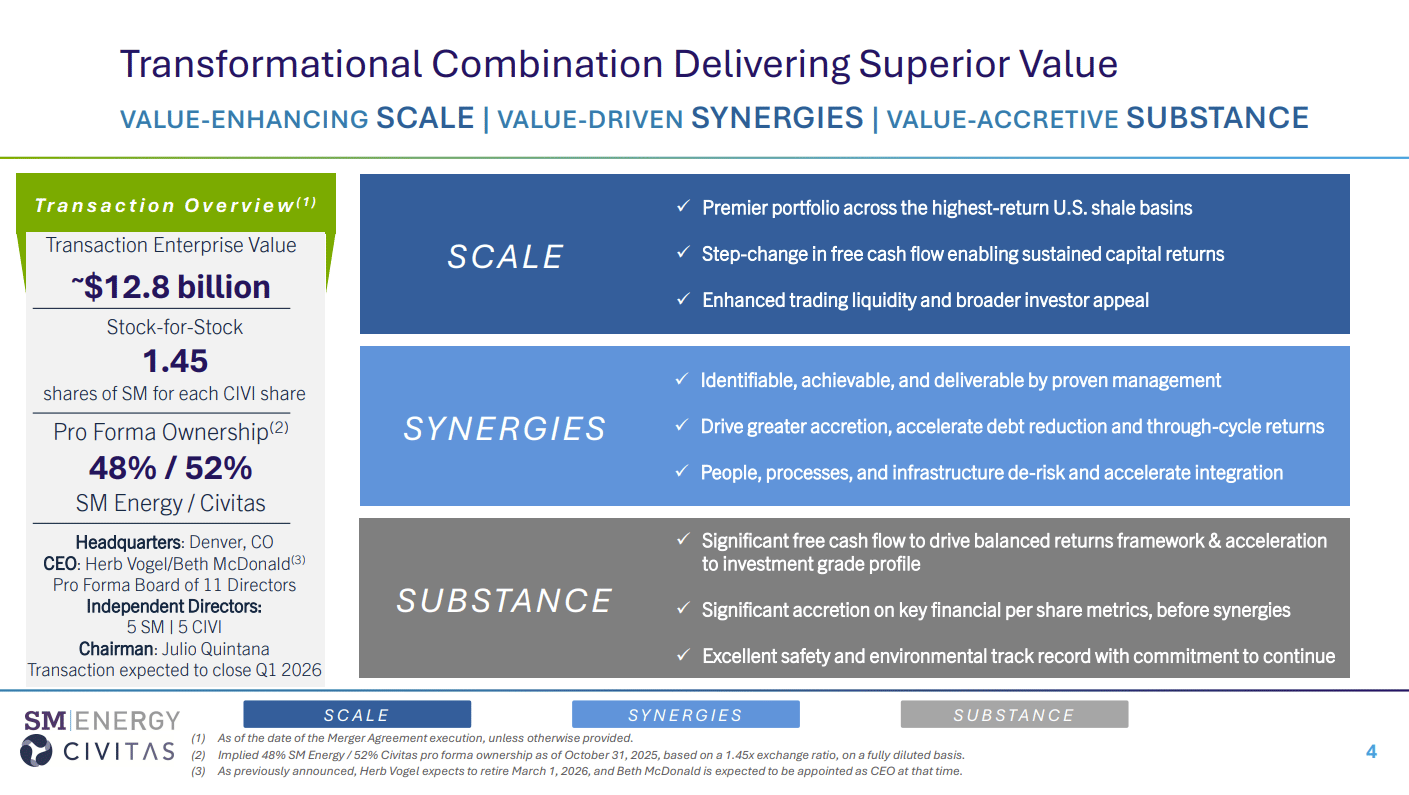

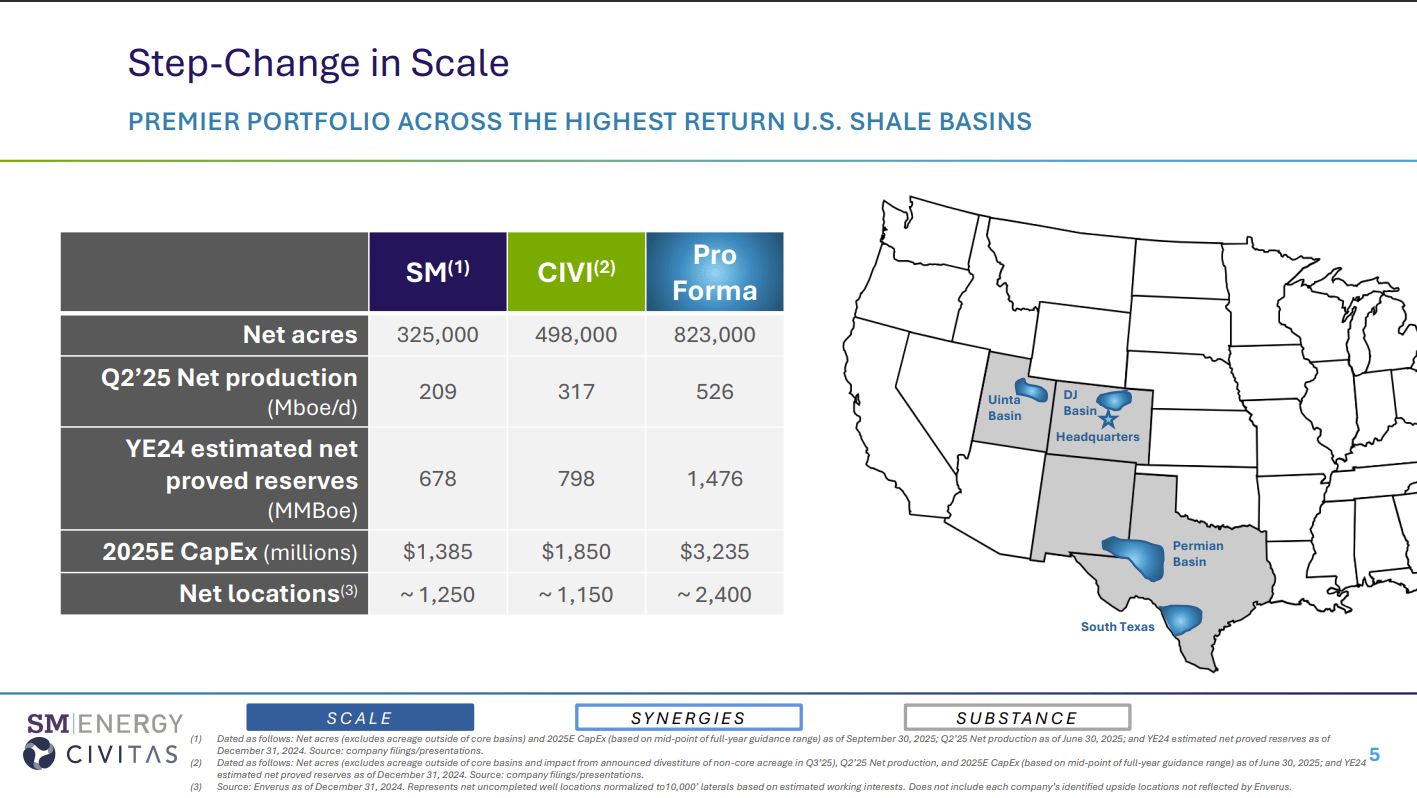

This week’s high noon standoff involved SM Energy and Civitas Resources. They unveiled a stock‑for‑stock merger valued at about $12.8 billion, including debt, to forge one of the largest independent oil producers in the Permian Basin.

Civitas shareholders will receive 1.45 SM shares for each Civitas share, leaving them with roughly 52% ownership of the combined company and valuing their holdings at around $30.29 per share, a modest 5% premium.

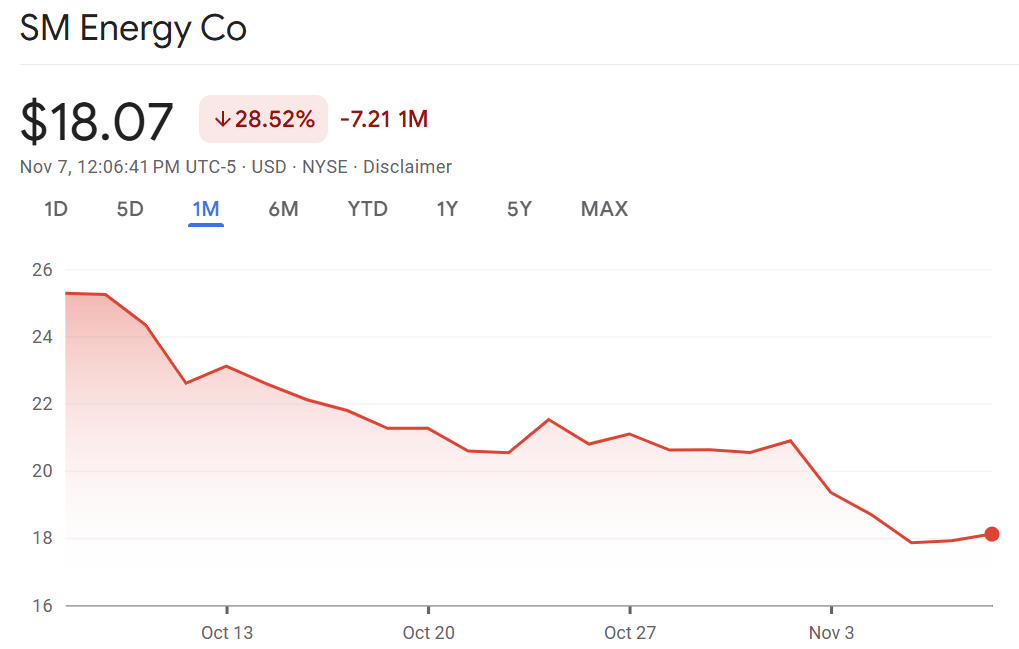

The exchange ratio left some on Wall Street scratching their heads: SM shares slid nearly 6% while Civitas barely budged.

Let’s do a little drilling on the transaction to understand why the Street maybe didn’t love this one.

On a pro‑forma basis the combined company will pump 526 thousand barrels of oil equivalent per day, hold 1.476 billion barrels of proved reserves and spend about $3.2 billion in 2025 capital expenditures.

Net acreage will swell to 823,000 acres across the Permian, DJ, Uinta and South Texas basins, giving the duo scale in nearly every high‑return shale play.

CEO Herb Vogel will helm the ship until his planned retirement in March 2026 (talk about going out with a bang), when Civitas chief Beth McDonald takes the reins.

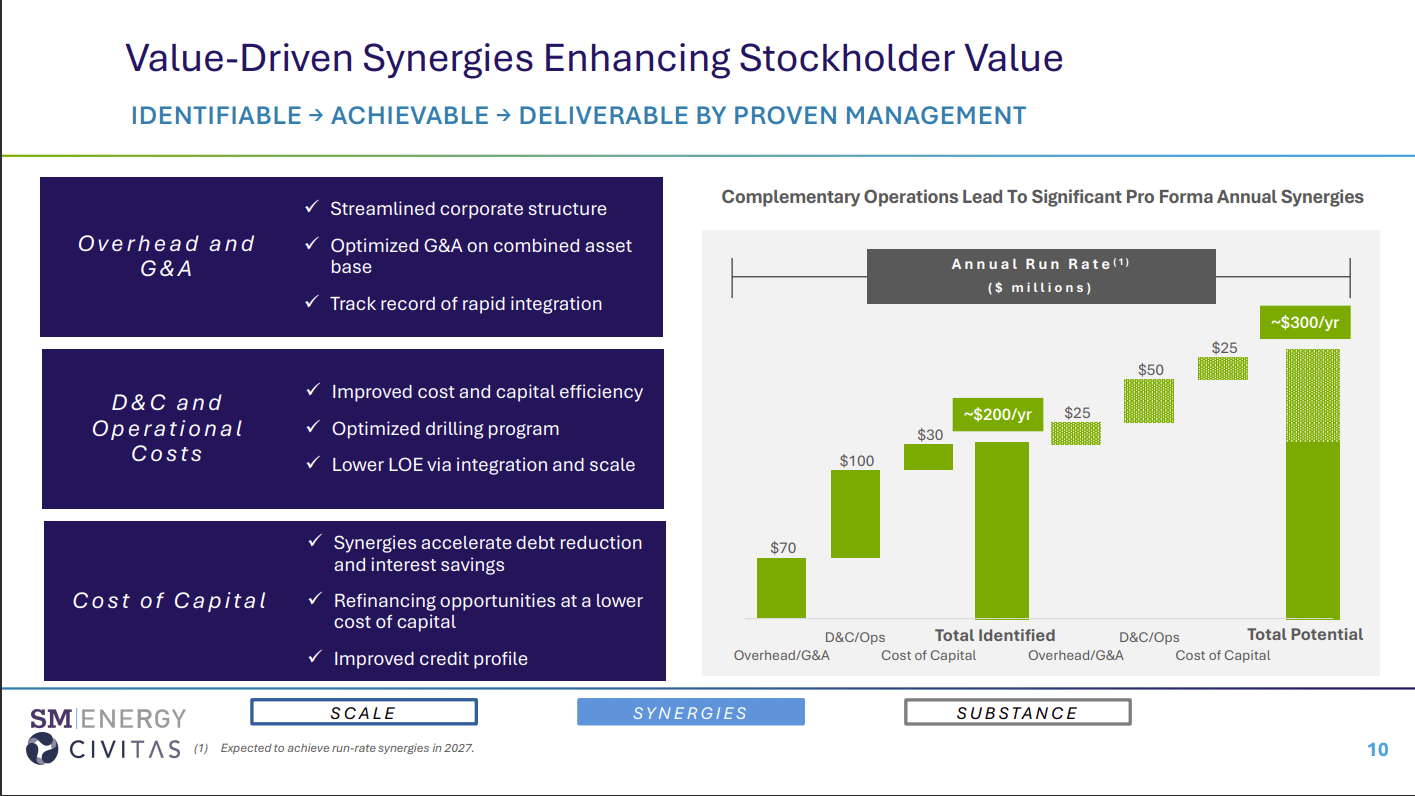

Scale isn’t the only prize. The companies estimate annual cost synergies of $200 million to $300 million by 2027 across three buckets: trimming overhead and general & administrative expense, wringing efficiency from drilling and completion operations, and lowering the cost of capital.

Roughly $70–$100 million in attributed to corporate overhead savings, $50–$75 million from drilling and operational efficiencies and $25–$30 million from cheaper financing (RIP private credit).

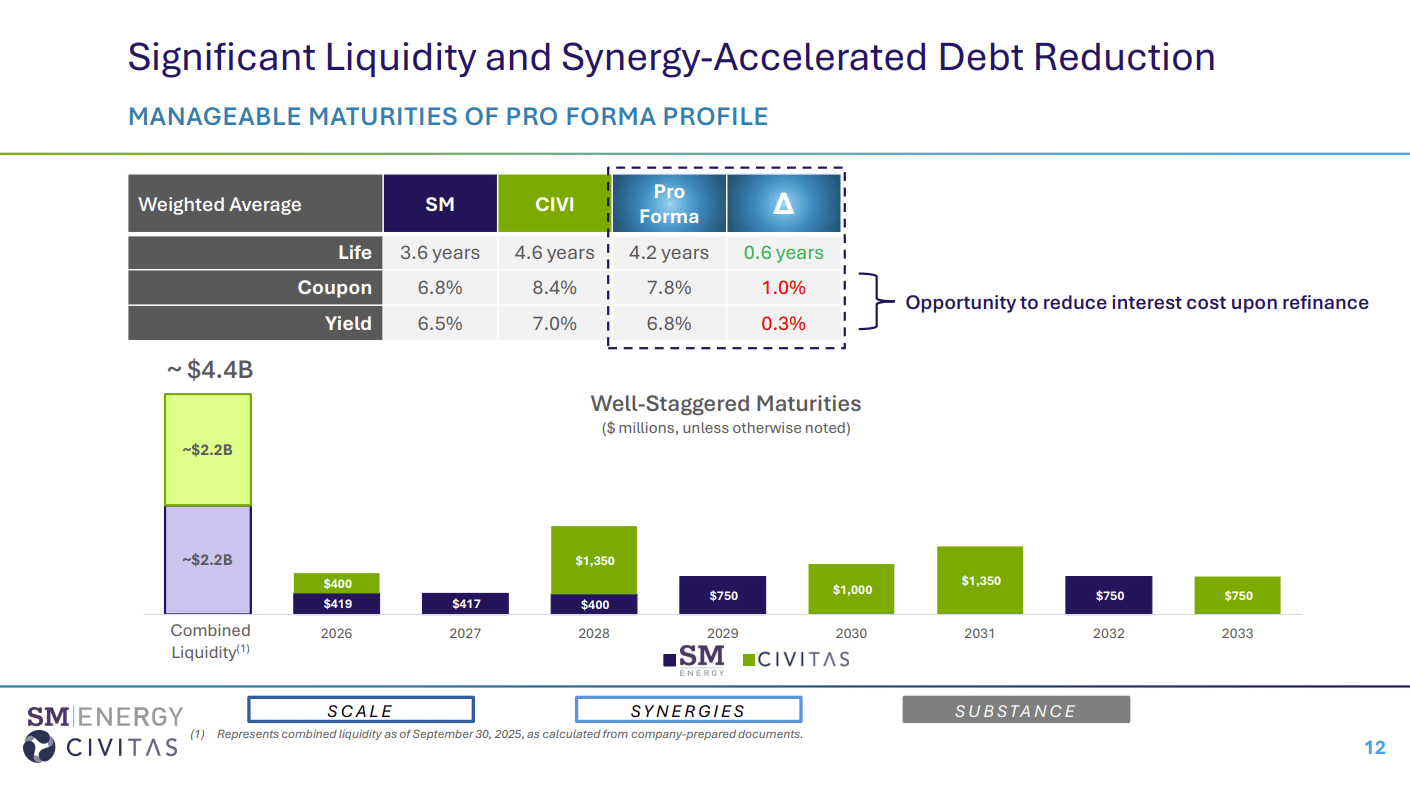

Those savings will help fund a debt diet and sustain SM’s fixed $0.20 quarterly dividend while preserving a $500 million share repurchase program, with a goal of driving net leverage down to 1.0x by 2027.

Management insists the combination will improve trading liquidity and broaden the investor base, setting up the new company as a top‑ten independent E&P producer. Still, the market’s not buying the “bigger is better” story just yet. Execution will be key, especially as integration risk looms and oil prices stay volatile.

With production poised to soar and a cash‑flow gusher, the only thing bigger than this merger might be the year‑end party… cowboy boots and hat optional.

What'd you think of today's newsletter? |