- Buysiders

- Posts

- Ferrero Does a Sweet Deal

Ferrero Does a Sweet Deal

Plus: A $3.5 billion royalty deal, and the most-drama filled tech deal of the year.

Short Squeez

July 22, 2025

Together with

Good morning! There has been over $40 billion of M&A announced in July, the Chainsmokers raised a $100 million VC fund, Jamie Dimon opened up about getting fired from Citi, and Goldman Sachs is beta-testing a direct intern-to-IB-to-PE pipeline.

If you are feeling like the “confusion never stops” and your bullpen is just “closing walls and ticking clocks”, don’t worry, we are a “part of the cure” coming at you with some sweet deals this week:

Ferrero Acquires WK Kellogg for $3.1 billion

Royal Gold Acquires Sandstorm Gold Royalties and Horizon Copper Royalties for $3.5 billion

Google Outbids OpenAI for Windsurf

Discover how Carta is pioneering AI for private equity; download the PE whitepaper to see how your firm can lead by 2030.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

A Sweet Deal for Kellogg

This might just be a me thing, but I haven’t evolved past my ten-year-old palate. If I weren’t so self-absorbed, I’d probably weigh 1,000 pounds thanks to the brands we’re covering today.

That’s right, it’s time for another food deal.

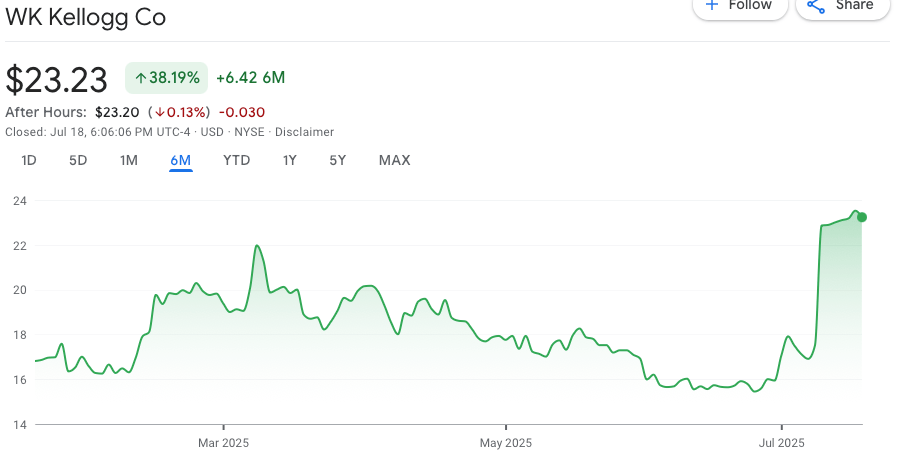

Just a couple of weeks ago, The Ferrero Group announced that it was acquiring WK Kellogg for $23 per share, or an enterprise value of $3.1 billion.

The acquisition price represents almost a 50% premium to Kellogg’s unaffected share price, something that has left Kellogg shareholders saying “that’s gr-r-reat!”

Kellogg’s share price has actually traded up above the acquisition price, which means that either some shareholders are going to actually be losing money on the deal, or investors think that there is room for a potential renegotiation.

If you ask me, I would have sold out at $23 and bought a couple of boxes of Fruit Loops to watch this unfold.

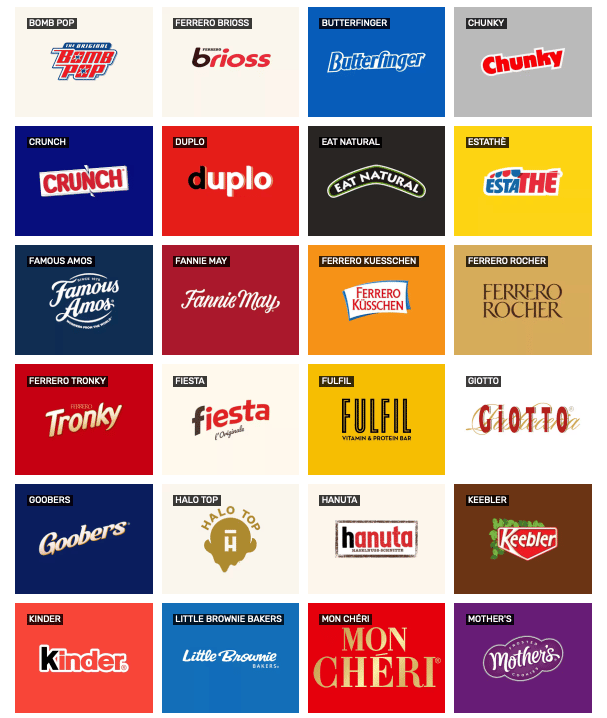

Generally, at least for us diabetic Americans, we are less familiar with Ferrero as a brand, even if we have eaten all of their candies before.

Ferrero is probably most known for Nutella, but that is not all they own. They also own iconic brands like Kinder, Halo Top, Crunch, Butterfingers, and a few more.

Select Ferrero Brands

So what is Ferrero really buying?

WK Kellogg dropped preliminary Q2’25 EBITDA guidance of $43–48 million, a step down from Q1. That puts Ferrero’s buyout at ~13x run rate H1’25 EBITDA, not a steal, but not outrageous either, considering they’re scooping up a well-known (albeit struggling) brand.

If Ferrero can revitalize Kellogg, this could be a sweet strategic win. Until then, here’s hoping the deal delivers a little Snap, Crackle, and Pop for Ferrero shareholders, and that Kellogg keeps dropping cereals that keep me borderline diabetic.

NEWS ROUNDUP

Top Reads

Goldman offers interns jobs in private equity within the firm

Neuberger Berman closes its fifth co-investment fund on $2.8 billion

Edtech company McGraw-Hill is seeking to raise around $537 million in its IPO

Citadel acquires Morgan Stanley’s US Equity Options Market Making Unit

One Rock Capital Closes $4 billion in largest fundraise to-date

PRESENTED BY CARTA

Why Some PE Firms Will Thrive (And Others Won’t Survive)

By 2030, AI won’t just be a competitive advantage, it will be the gold standard. And, the firms that don’t adopt it will likely go extinct.

Insert Carta.

They are helping top PE firms automate reporting, cut errors, and unlock deeper insights with a platform built for the future.

Their new whitepaper reveals:

The three models of PE back-office operations—and why their hybrid tech-services approach is the future

How their AI-driven platform is transforming fund reporting, due diligence, and deal flow for leading firms

What agentic AI means for scaling productivity, accuracy, and service to LPs

Don’t let your firm fall behind. See how Carta is helping PE leaders set the pace for the next decade.

STRATEGIC DEAL OF THE MONTH

Royal Gold’s Golden Ticket

While I like to think of myself as finance royalty for the value I provide to you all, this month there is an actual royalty deal that hit the market.

For those who haven’t spent as much time staring at rocks as I have, royalty companies don’t operate mines. Instead, they finance mining projects and in return collect a share of the revenue (royalties) or a portion of the metal produced (streams). It’s basically passive income on an industrial scale.

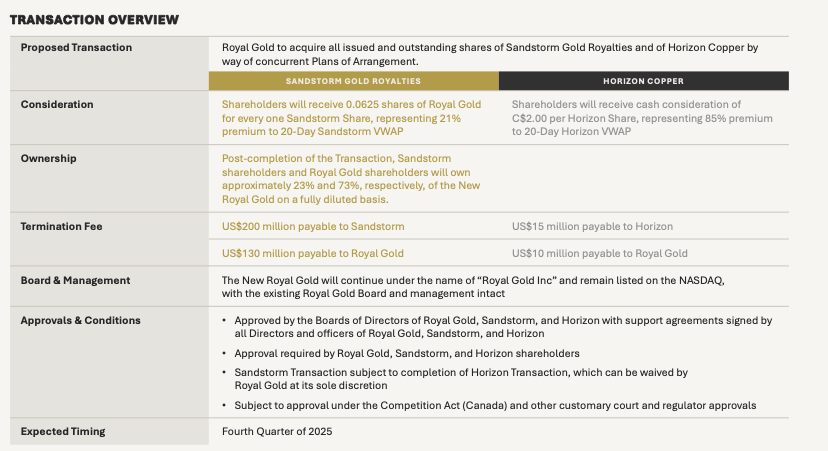

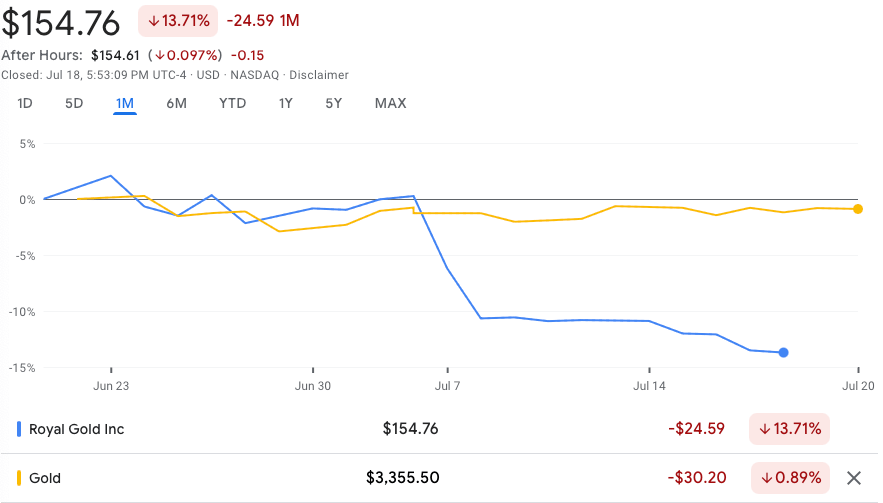

Royal Gold, one of the biggest players in the space, just agreed to acquire Sandstorm Gold and Horizon Copper for a combined $3.5 billion, paying a 21% and 85% premium, respectively.

Post-transaction, Royal Gold shareholders will retain 77% ownership on a fully diluted basis.

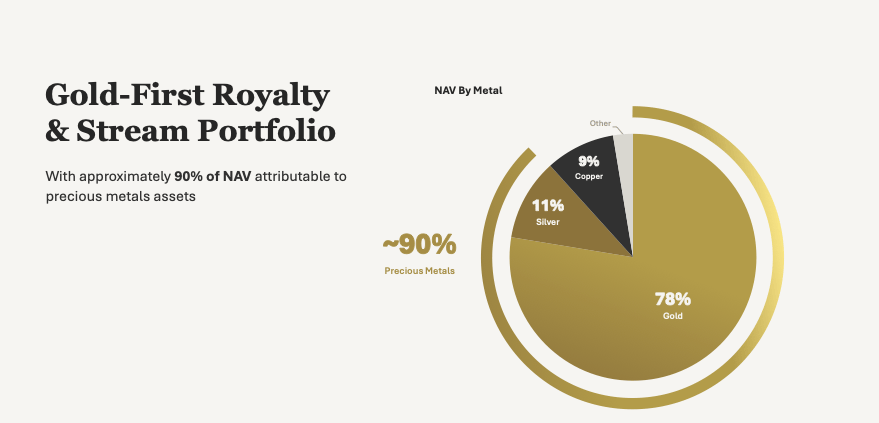

In the mining industry, the gold standard is…well the gold standard. Gold is much less volatile than other precious metals like silver, and is always in demand, so if you can buy a full portfolio of gold royalties, you are…golden.

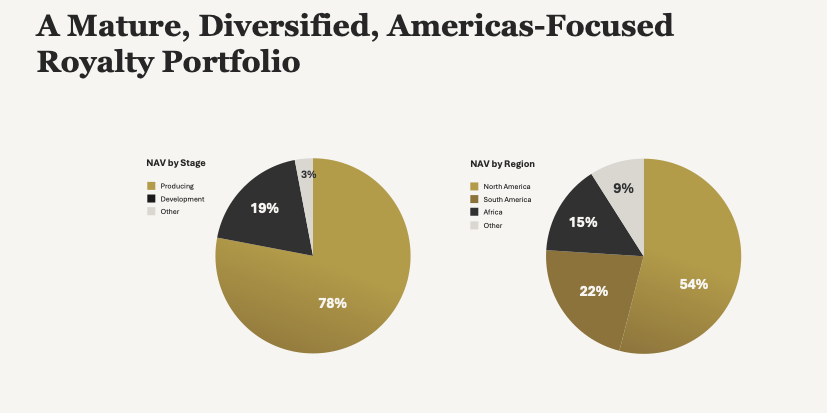

The new Royal Gold will have 78% of its net asset value (NAV) tied to gold, with most revenue coming from producing assets in safe jurisdictions - translation: cash flow from Canadian mines that aren’t running out anytime soon.

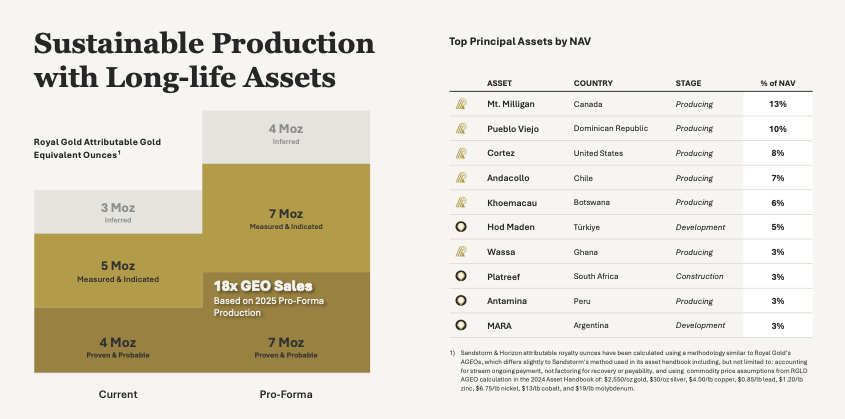

If you are curious how long “anytime soon” is, there are millions of ounces of gold in reserves at these operations, which is enough gold for your grandkids to still be shareholders of this company.

While this deal is obviously a screamer for the Sandstorm and Horizon shareholders, it is a bit less so for the Royal Gold shareholders, with the Royal Gold share price dropping 14% in the past month (I will let you guess when they did the announcement).

Before you try to defend them and ask about gold price changing, don’t worry, I already thought of that and gold is basically flat over the same period.

As a mining nerd, this is a fun deal to think about, but it does come cross a bit like empire building at the peak of the market.

Gold prices are near all-time highs, so the thought of buying a gold royalty at the peak of the commodity cycle is…interesting. Especially at such a high premium.

This take will either age well or like milk, really depends on what the next geopolitical issue is…

TECH SHENANIGANS OF THE MONTH

Google Out Angles OpenAI

In a world where just putting AI in your name adds 10 turns to your revenue multiple and a few hundred million to your net worth, it is not shocking that Big Tech is having a big d*ck contest about who will lead the AI revolution.

This month’s showdown? OpenAI vs. Google.

Earlier this month, OpenAI offered $3 billion to acquire Windsurf (the AI coding assistant). Why the guys behind ChatGPT couldn’t just have their bot rewrite it is beyond me, but let’s continue.

Interestingly, OpenAI was actually already invested in the rival coding assistant, Cursor, so this could have resulted in OpenAI cannibalizing one of its own investments in its Startup Fund. What did Masa and the Soft Bank Vision Fund advise on this deal?

Not to be outdone, Google came in with a Silicon Valley special, $2.4 billion to license Windsurf’s tech and hire its top talent, including the CEO.

This structure is not uncommon in the AI space, where a company hires the start-up’s talent and a license rather than outright acquire the company. Google did this with Character.AI CEO Noam Shazeer about a year ago.

So what happened to the rest of Windsurf? The leftovers (IP, engineers, and enterprise customers) were scooped up by Cognition in a $300 million stock deal.

The remaining employees, many of whom learned the news via Slack and were locked out of systems, were offered accelerated vesting and soft landings, but the damage was done. Even Vinod Khosla said he wouldn’t work with the founders again.

This just goes to show that maybe the SF tech bros know something that us bankers don’t. After all, how many bankers do you hear getting poached for a multi-billion dollar pay package while “vibe modeling” at the bar?

What'd you think of today's newsletter? |