- Buysiders

- Posts

- Kimberly-Clark Swallows Kenvue

Kimberly-Clark Swallows Kenvue

Plus: A $7 billion gold rush and Enhanced Games get a juiced-up valuation

Short Squeez

December 04, 2025

Together with

Good morning! Hope everyone had a wonderful Thanksgiving. Even if you took Thursday off, you still probably worked harder than Europeans during the summer.

Winter is fast approaching with snow forecasted to hit NYC, but don’t worry there are still plenty of deals to keep you warm. Even if the market is down, HSBC estimates that OpenAI will have to raise another $207 billion in funding to cover its losses, and of course Elon is back raising for xAI...@grok is this true?

If that isn’t enough to tide you over on this snow day, here are this month’s top 3 deals:

Kimberly-Clark acquires Kenvue for $49 billion

Coeur Acquires New Gold for $7 billion

Enhanced Games goes public via SPAC at a $1.2 billion valuation

Which direct lenders are winning deals in your sector? 9fin’s private credit database can tell you. See how it works.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

Kimberly-Clark Swallows Kenvue

Mega-deals are so back. So put on your diapers and pop some Tylenol because we have ~$49 billion of value to create here.

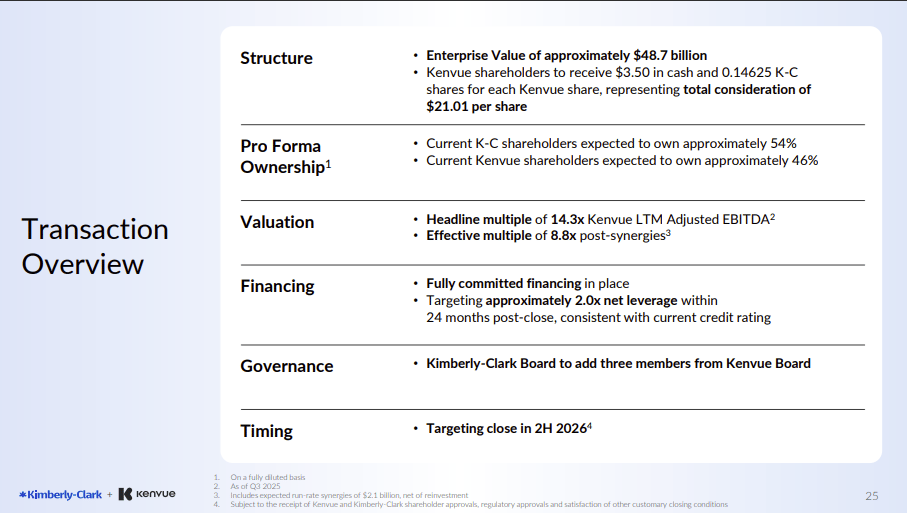

Kimberly‑Clark, maker of Huggies diapers and Kleenex tissues, will acquire consumer‑health company Kenvue in a cash‑and‑stock transaction valued at $48.7 billion.

Kenvue shareholders will get $3.50 in cash plus 0.14625 Kimberly‑Clark shares per Kenvue share, equating to roughly US$21.01 per share, with Kimberly‑Clark shareholders owning about 54% of the pro forma company.

By the way - the acquisition price is 14.3x LTM EBITDA. I think Kimberly-Clark shareholders are going to need some Tylenol (and maybe Huggies and Kleenex) to cope with that premium.

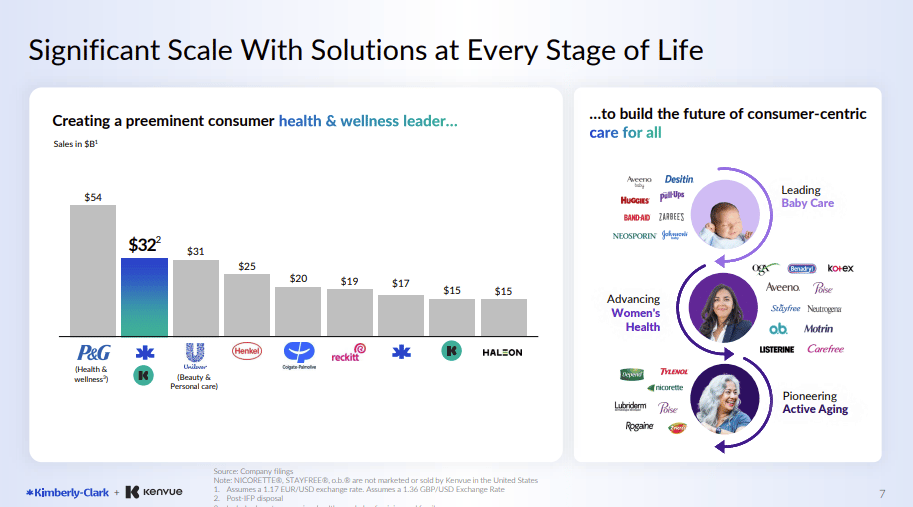

Once the diapers are changed in the second half of 2026, the merged company will have about $32 billion in annual revenue and US$7 billion in adjusted EBITDA.

The rationale makes sense, Kenvue boasts ten brands that each generate more than US$1 billion in annual sales, from Neutrogena skin care to Tylenol pain relievers, and the pro forma company will jump up to right below P&G in terms of revenue.

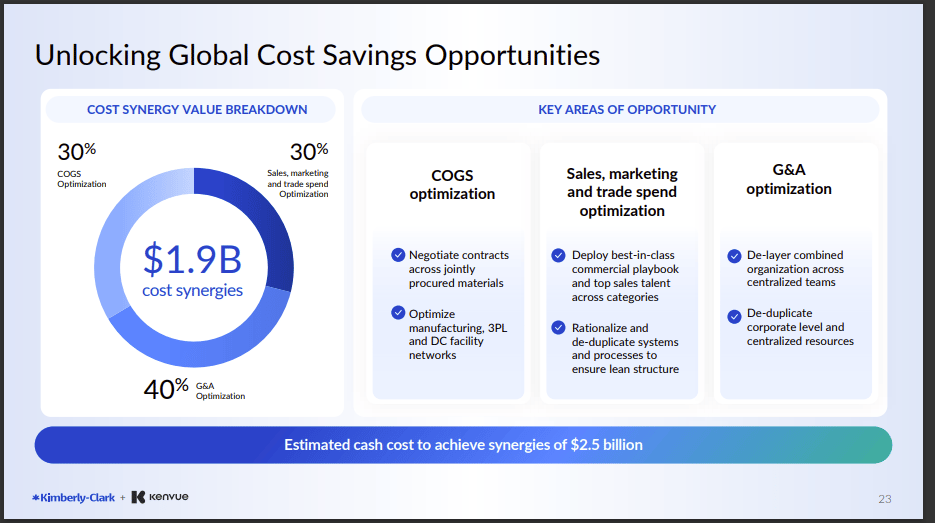

It is not just investors who may need some Kleenex, however. I doubt this was included in the pitch deck, but Kimberly-Clark has a self-proclaimed “Relentless Culture of Cost Discipline”.

That’s all well and good until you realize that the company focused on cost discipline sees $1.9 billion of cost synergies coming as part of the deal. I mean, they literally mention de-duplicating roles across in two buckets that account for 70% of their estimated cost synergies.

Yea, that’s a lot of LinkedIn updates coming down the pipe, but hey, at least they may have to purchase some extra products while they do it. I wonder if that also made it into the synergies calc…

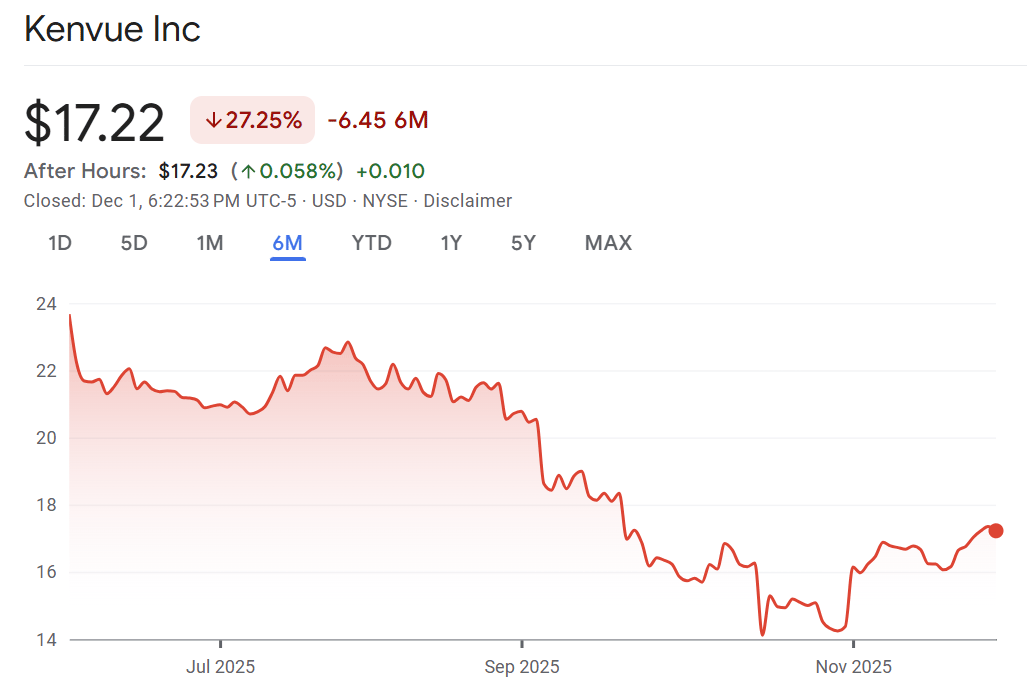

Kimberly Clark shareholders have been having a rough go of it recently, with the share price down 23% in the past 6 months. A majority of that fall came when the company announced earnings and the acquisition back-to-back. I’d probably be putting on some Huggies if I were long KC right now.

Kenvue’s share price over the past 6 months is equally as horrific, down ~27% including the acquisition bump.

This is primarily due to the political noise around Tylenol recently, however. The acquisition did cause a ~12% jump in share price, though the company is still not trading anywhere near the acquisition price. Likely this is due to a large amount of perceived risk in the transaction and probably some legal overhang on the Tylenol front.

This one will be fun to watch due to the political nature of Tylenol after the Trump administration linked it to autism. At least the Kenvue shareholders will get some Kleenex (and a nice premium) to ease some of their share price pain since the Administration’s announcement.

PRESENTED BY 9FIN

The Debt Market Platform PE & Credit Teams Rely On

Evaluating opportunities in private credit means knowing which lenders are active, how terms are shifting, and where stress is emerging across the market.

9fin tracks deal flow in real time, from direct-lender mandates to covenant packages and pricing trends, and pairs it with industry-leading BDC research covering non-accruals, watchlists, and quarterly performance.

Built on 10 million+ data points across leveraged loans, private credit, and structured products, 9fin brings transparency to markets that traditionally operate in the dark. With 20+ years of historical deal data following our Bond Radar acquisition, you get a complete view of market dynamics in one platform.

They're giving the Buysiders audience exclusive access to a free 30 day trial. Click below to get started, and see how 9fin keeps you ahead of every market move.

NEWS ROUNDUP

Top Reads

STRATEGIC DEAL OF THE MONTH

Coeur’s New Golden Ticket

While there is no food deal (maybe for the best coming out of Thanksgiving), the mining industry decided to give me a little early Christmas gift with a gold deal popping up in late November.

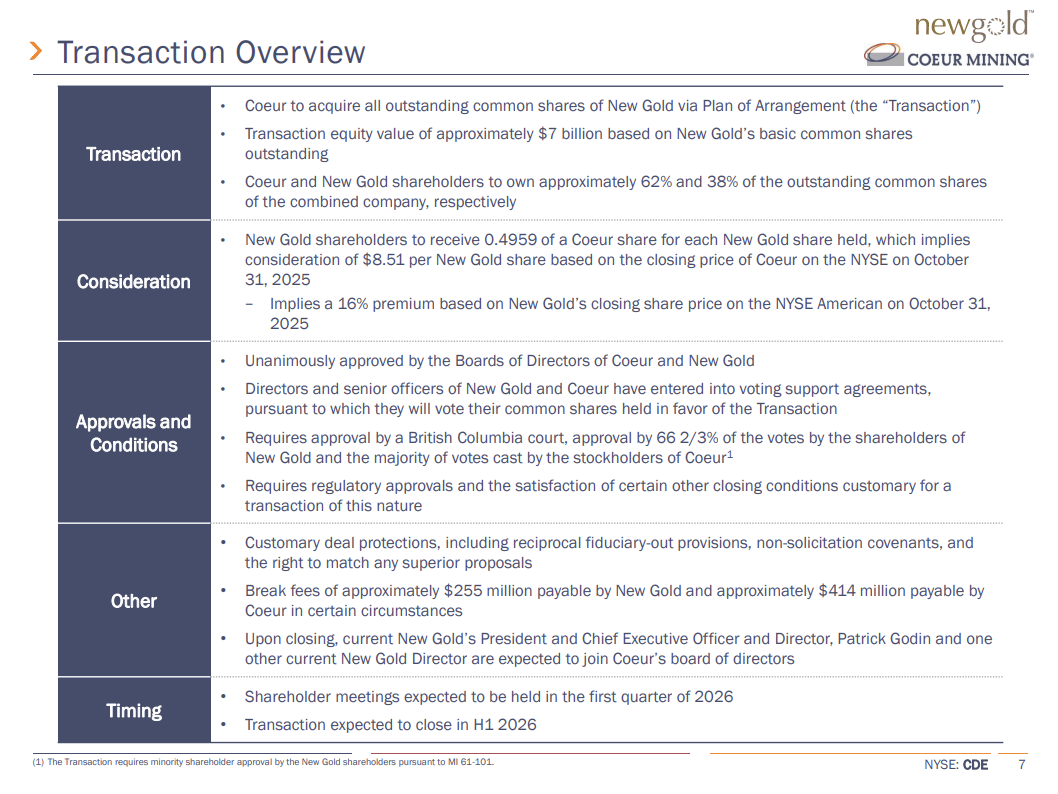

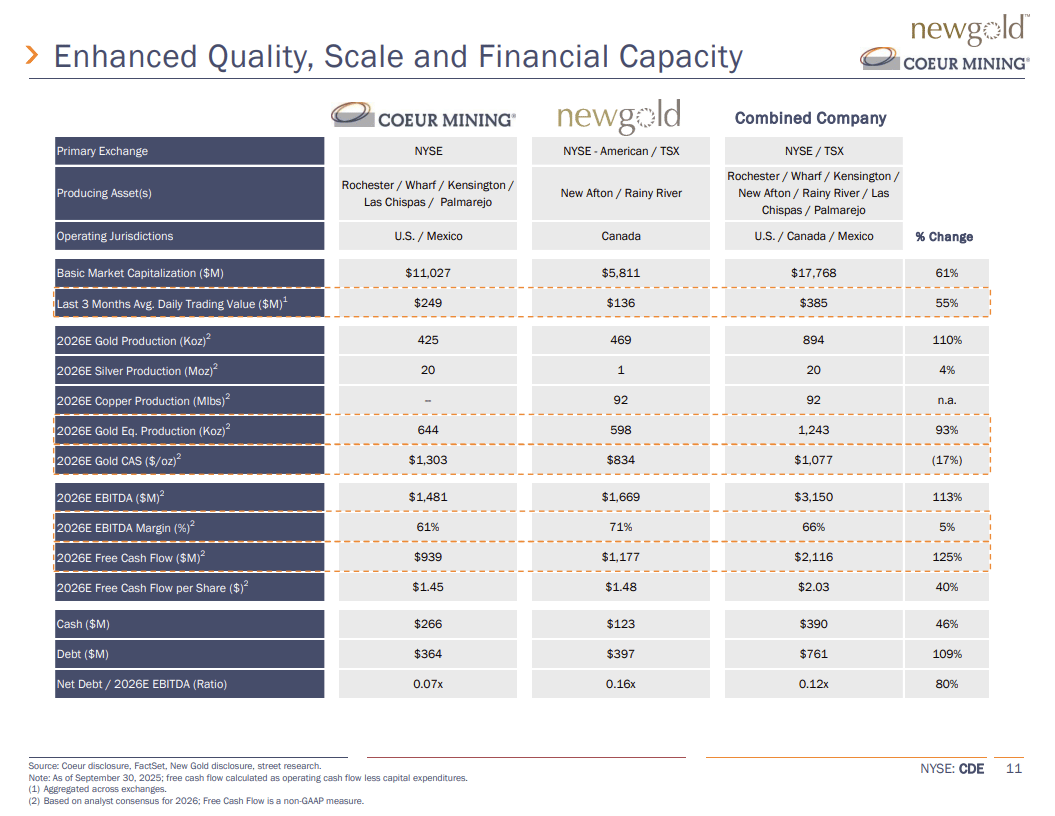

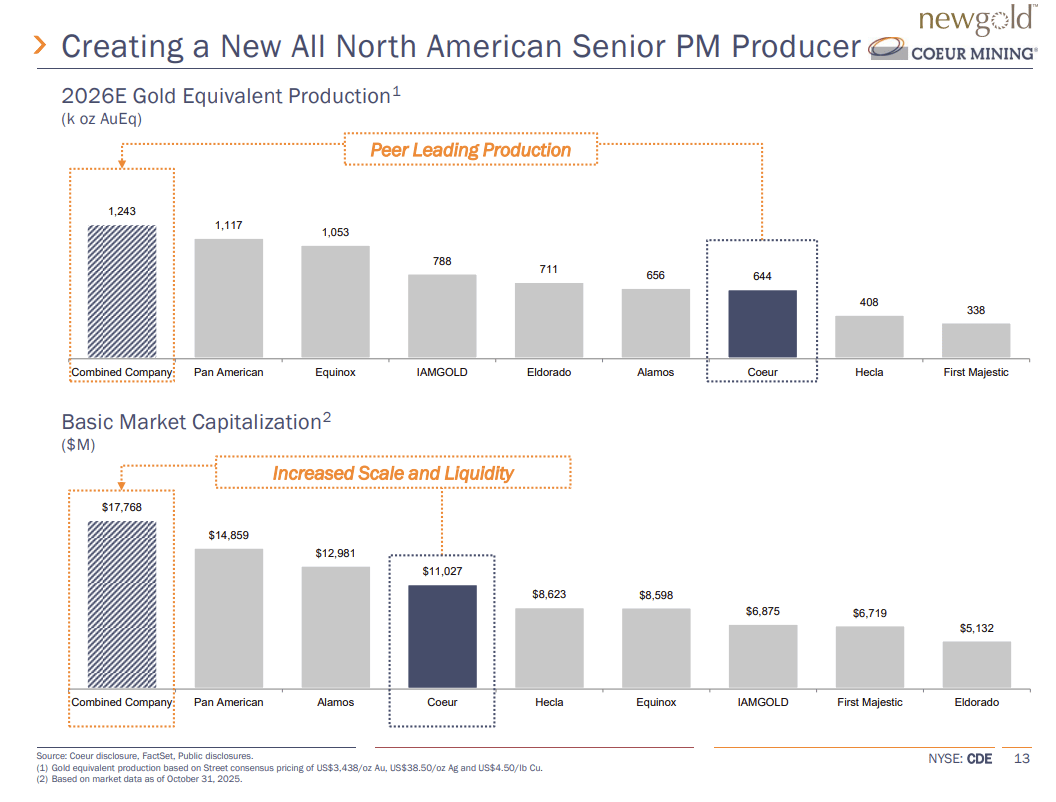

So, it’s time to get our hands dirty once again because Coeur Mining has agreed to acquire Canada’s New Gold in an all‑stock merger that values the target at roughly US$7 billion.

Each New Gold share will be exchanged for ~0.5 Coeur shares, implying a value of US$8.51 per share and a16% premium.

When the dust settles in the first half of 2026, Coeur shareholders will own about 62% of the combined miner and New Gold investors roughly 38%. Coeur is paying around 8.7x New Gold’s EBITDA. Not bad for a mining deal, though it is no 21x like we saw a few weeks ago.

So what’s in the pan besides glitter?

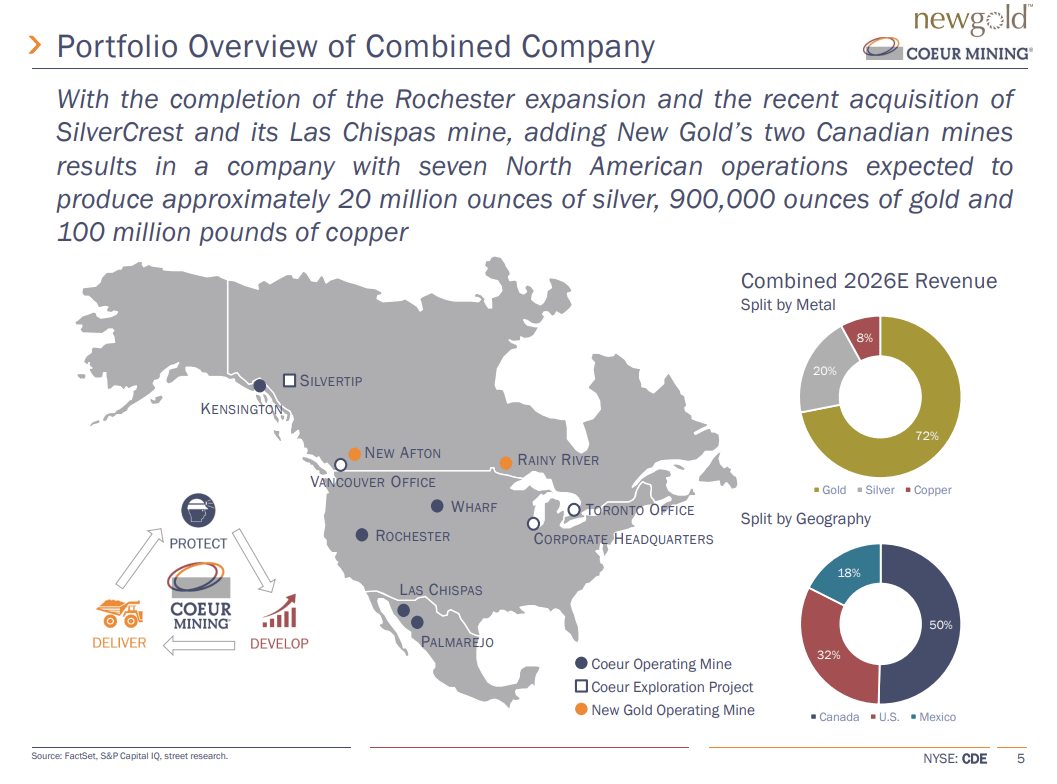

By combining New Gold’s Rainy River and New Afton mines with Coeur’s five operating pits, the enlarged group expects to churn out 20 million ounces of silver, 900 thousand ounces of gold and 100 million pounds of copper next year.

The pro forma company will generate around US$3 billion of EBITDA and US$2 billion of free cash flow in 2026 with more than 80% of revenue will come from stable U.S. and Canadian operations.

The combined company aims to climb into the top ten precious‑metals producers and plans to use the extra cash to extend mine lives and fund exploration.

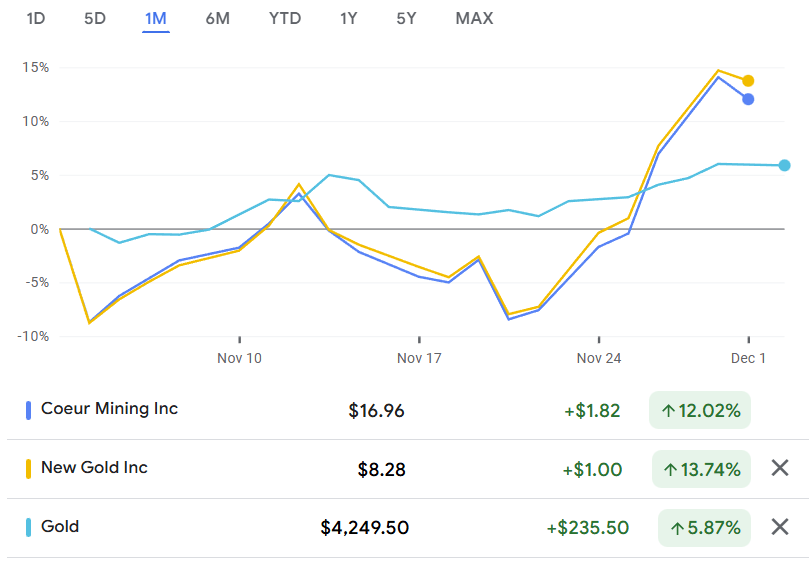

As we do with all of these deals, you have to look at the share price moves in the context of gold price moves.

Gold prices are up ~6% over the month, with Coeur and New Gold up 12% and ~14%, respectively. Meaning there is some noise outside of the gold price moves that can be attributed to the acquisition. I guess you could say these companies may have hit the motherlode with this one.

Executives are pitching the merger as a “free cash machine,” yet the real question is whether combining a bunch of mid‑life mines turns you into King Midas or just gives you carpal tunnel from all the pan‑shaking. Consolidation in the mining industry is common, and it does not always work.

Investors seem intrigued, but don’t start polishing your bullion bars or ordering matching prospecting hats quite yet. This one is not a guaranteed home run. It is being done when gold prices are relatively high, which means everything needs to go right for this to pan out.

SPAC DEAL OF THE MONTH

SPACs Get Juiced Up

How I feel jumping in my local pool

Listen, I was a college athlete and I totally could’ve gone pro if not for my shoulder injury…or was it my knee…or my elbow? Jokes aside, I was a college athlete - though no where near a professional level - and like every athlete I once had Olympic dreams…that were quickly crushed.

There is some much the Olympics do right…but the one thing that is missing is that you never get to see the true upper limit of human potential. I mean Usain Bolt is ridiculous. Michael Phelps is the greatest to ever do it. Hell we’ve even seen investment bankers win Olympic golds in rowing. If that isn’t enough, we have even seen Eddie Hall deadlift 500kg (over 1,000lbs) while ~allegedly~ not on steroids (I know that wasn’t an Olympic event, but it was still an absurd feat).

But what could these guys do if they could ~officially~ enhance their performance. How much could a human pick up? How fast could they sprint? How high could they jump?

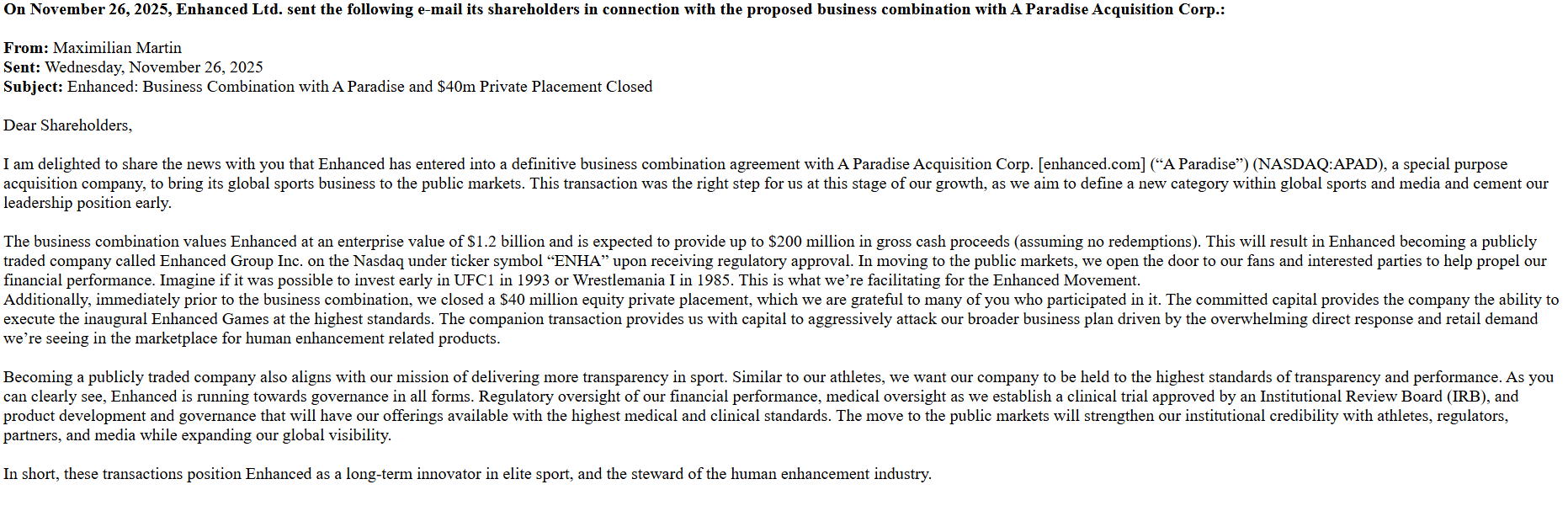

Well, the Enhanced Games has a $1.2 billion answer to that question.

Enhanced is going public via a SPAC merger with A Paradise Acquisition Corp. SPAC’s are confusing, but the short version is that in addition to the merger into the SPAC, Enhanced could get up to $200 million of cash as a part of the deal, depending on redemptions.

In addition, there is also a $40 million private placement that will be consummated immediately prior to the transaction.

In an email to investors, Enhanced CEO Maximilian Martin likened the opportunity to the ability to invest in UFC in 1993 or Wrestlemania in 1985.

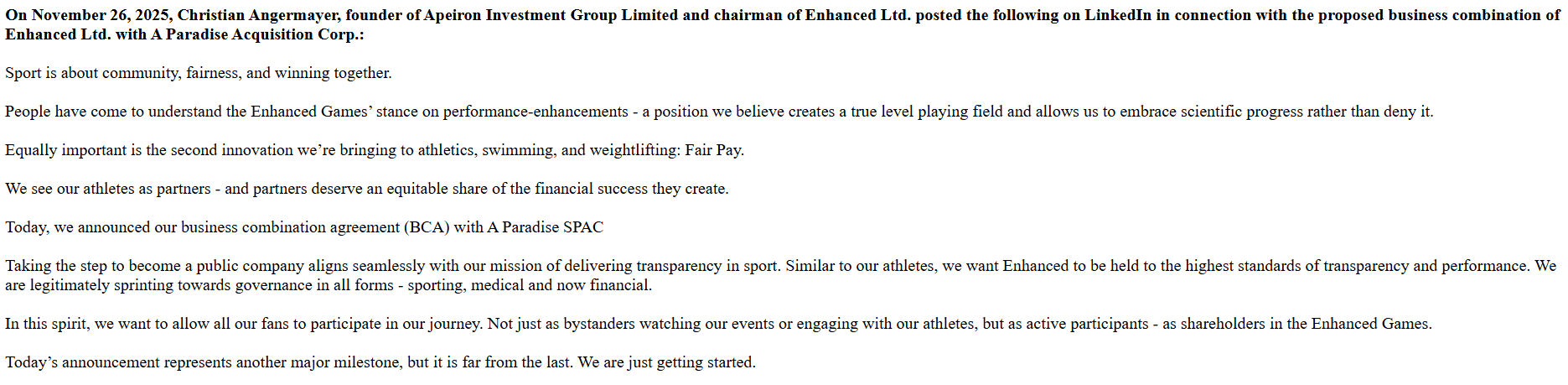

One of Enhanced’s largest shareholders - Aperion Investment Group - also entered into a support agreement as part of the transaction, and the founder of Aperion / chairman of Enhanced expressed his excitement about the transaction on LinkedIn (which of course made EDGAR).

While the SPAC mechanics are messy, one thing is clear. Enhanced is here to stay, and it plans on making a name for itself at its inaugural event in May 2026 in Las Vegas.

Who knows, maybe this business combination is just the juice Enhanced needed to fully take off. All I know is that I am excited to see what true human potential looks like.

What'd you think of today's newsletter? |