- Buysiders

- Posts

- Lakers Sell for $10B

Lakers Sell for $10B

Plus: Bayview pays a 56% premium for a mortgage lender, and Keyera makes a Plain acquisition.

Short Squeez

July 01, 2025

Together with

Folks, they’re all talking about it. You’ve heard of the One Big Beautiful Buysiders? Very nice. Tremendous newsletter.

It’s the best newsletter on Wall Street, okay? All other newsletters are a total disaster. Sad!

Nobody is breaking down billion-dollar deals like this. Not Bloomberg, not WSJ, not FT, not even the 'Houthi PC Small Group' Signal chat.

The top three deals this month? Absolutely incredible. Can you believe it? It’s an unbelievable amount of dealmaking. Frankly, I’m getting tired of winning in M&A. But we keep doing it, every week.

Guggenheim CEO acquires the Lakers for a $10 billion valuation

Keyera acquires Plains’ Canadian Assets for $3.8 billion

Bayview Acquires Guild Holdings for $1.3 billion

Thank you for your attention to this matter!

This luxury mountain retreat is making some wealthy families (and the investors cashing in) very, very happy. See it for yourself.

First time reading? Sign up here.

Have feedback? Respond here.

EXIT OF THE MONTH

The Biggest Deal in Sports

While some may call it jumping on the bandwagon - or maybe, the Buss - the Lakers have finally changed hands for the first time since 1979.

The Buss family has agreed to sell a majority of the Los Angeles Lakers to Mark Walter - the co-founder and CEO of Guggenheim - at a valuation of ~$10 billion.

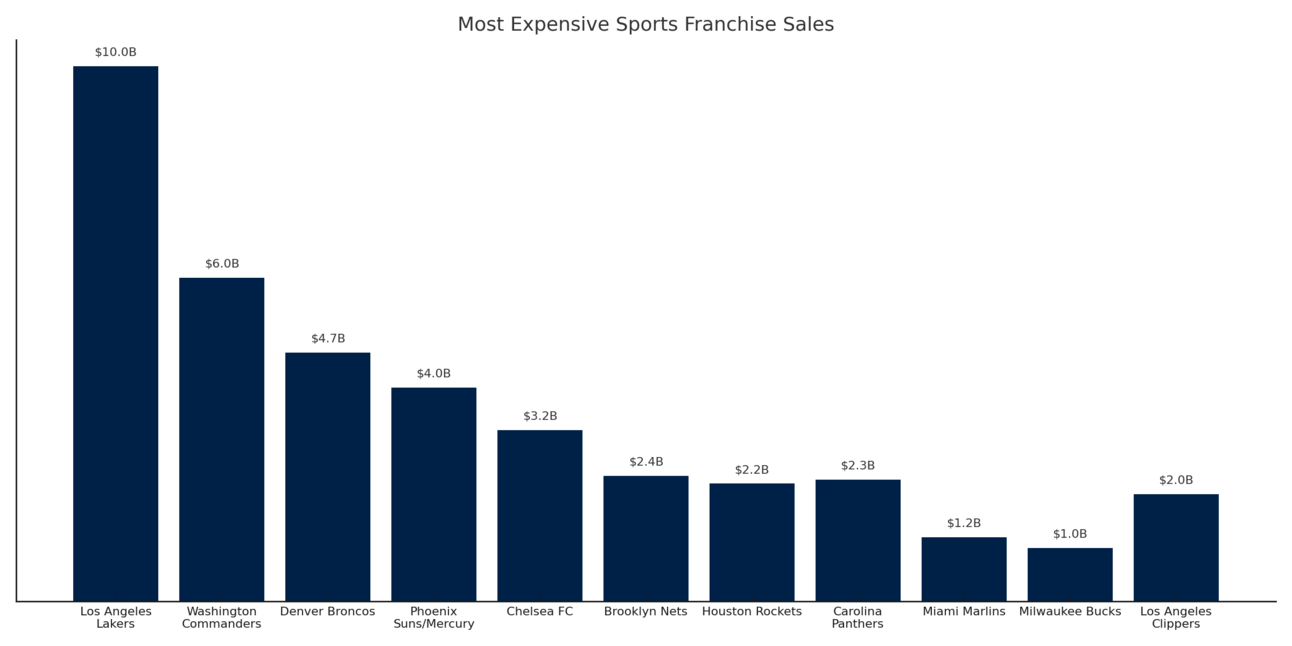

This is now the largest deal ever for a U.S. sports franchise, eclipsing even the Washington Commanders, which sold at a pathetic $6.5 billion valuation.

The deal itself is being done via TWG Global, which is Walter’s holding company that is comprised of various investments, including stakes in the Los Angeles Dodgers, Chelsea F.C., and the Los Angeles Sparks.

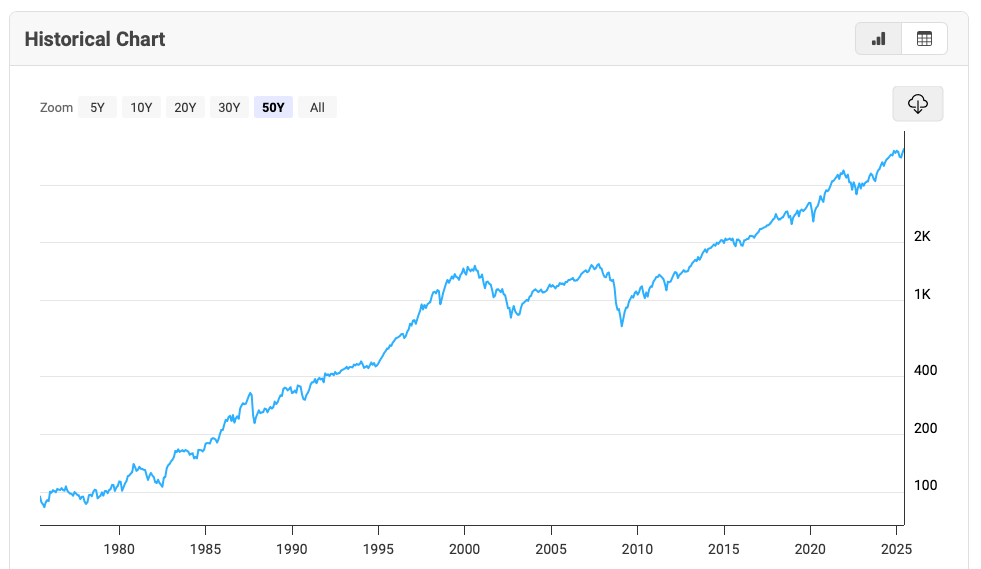

Buss bought the Lakers back in 1979 for $67 million. Since we are all finance bros here, let’s do a little math.

If you invested $67 million in the S&P 500 in 1979, that would be worth ~$12.5 billion today.

While Buss marginally underperformed the S&P 500 (by an amount that would definitely get me to retire from newsletter writing), I would still call a 150x return over almost 50 years a solid win. Also, you can’t flex courtside at the next S&P 500 game.

50 Year S&P 500 Performance

To ensure a smooth transition, the Buss family will retain a 15% stake in the Lakers in the near-term.

From Showtime to Shaq & Kobe, to the LeBron twilight era, the Buss family turned the Lakers into more than a team, they created a legacy. Exiting at the top of the market though? That’s just savvy portfolio management.

Two weeks ago Moelis announced his retirement, last week we retired X as a ticker on the NYSE, this week the Buss family is retiring its ownership in the Lakers. The one thing that remains consistent? It is not about championship banners or jerseys or Patagonias in the rafters, it’s about what multiple you exit at.

PRESENTED BY PACASO

This House Is Insane: Mountain Views. Ski Access. A Hot Tub!?

The Lionshead property in Vail has all the luxuries you’d expect in a $2.1 million mountain vacation home–access to the slopes, panoramic views, a heated deck…

But forget all that. Here’s the real kicker:

You can invest in this property (and its revenue stream) via Pacaso, the platform that turns fractional shares of high-end vacation homes into recurring profits.

Wealthy families share in the ownership, Pacaso handles the logistics, and you get a slice of the $1.3T vacation home market.

Co-founded by the guy who sold Zillow for $16 billion.

Don’t miss out–see all of Pacaso’s luxury offerings here.

NEWS ROUNDUP

Top Reads

Meta seeks $29 billion private credit package for data centers

Europe expands share of global PE infrastructure fundraising

Macquarie Infrastructures closes its sixth fund with $8 billion in commitments

Marlin Equity Partners closed Marlin Heritage Europe III on a hard cap of €1 billion.

Apollo Provides $750 Million High Grade Capital Solution to Mumbai International Airport

DEAL OF THE MONTH

Keyera Makes a Plain Acquisition

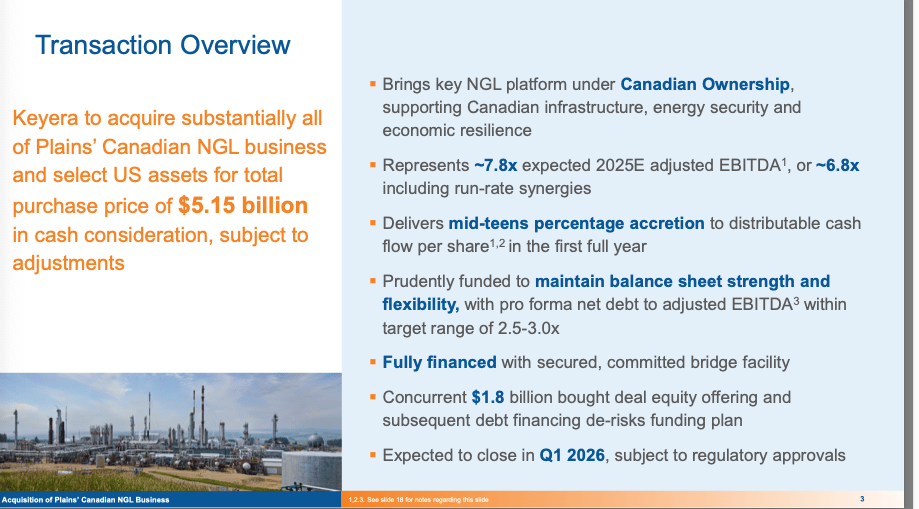

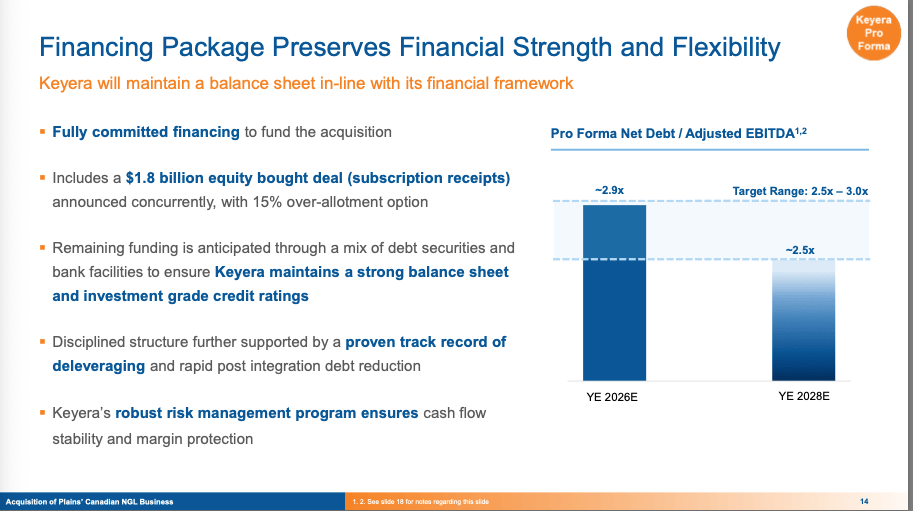

Keyera, one of Canada’s leading midstream energy companies that owns and operates pipelines and gas processing plants, has agreed to acquire Plains’ Canadian natural gas liquids business for a whopping C$5.2 billion. (Since most of us don’t know the conversion from hockey pucks and maple syrup to freedom bucks, that is ~$3.8 billion in real money)

The deal is being struck at ~7.8x 2025E EBITDA, and is expected to be funded partially by a new equity offering as well as a following debt financing.

Given Keyera is looking to raise debt for the transaction, we have to take a look at the pro forma credit metrics to think about how the market will react to this one.

Keyera indicated that its target net debt range is 2.5 - 3.0x; however, this deal will push them up to the higher end of that range, pushing ~2.9x.

In a world with so much uncertainty, it’s hard to believe equity holders are thrilled to be flirting with the upper end of leverage guidance.

That said, shareholders didn’t react as negatively as we’ve seen in other deals lately. The share price only dipped about 1% post-announcement, suggesting investors might actually be giving some credit to the potential synergies instead of fixating on the debt burden.

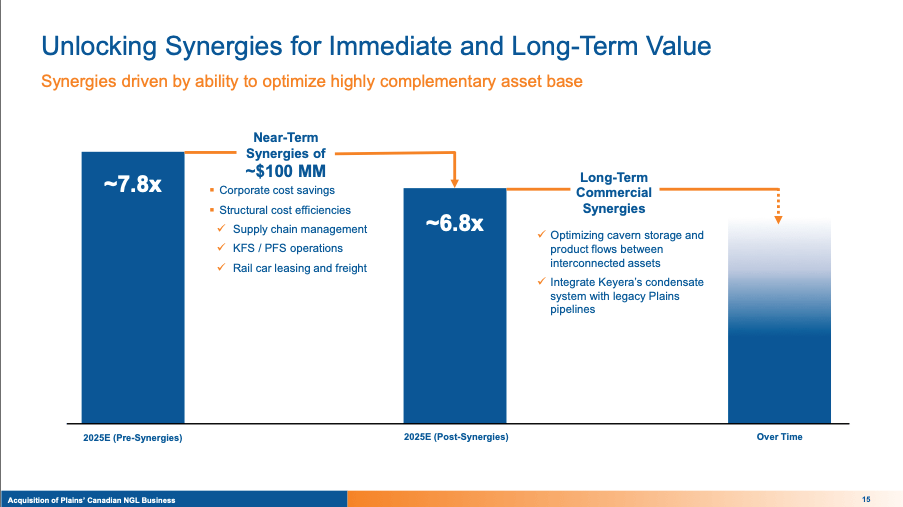

Synergies in midstream oil & gas aren’t exactly rocket science. To put it simply: I have a pipeline, you have a pipeline, let’s make one big pipeline.

That being said though, Keyera anticipates that it will be able to generate $100 million of cost savings (RIP to anyone with a plains.com email address), which brings down the acquisition multiple a whole turn to 6.8x…talk about banker math.

Unlike the ice they skate on, Canada–U.S. relations are anything but smooth right now, so it’s no shock to see Canadians keeping this one on home ice.

To put it in terms my relatives up North will understand: it’s 3–0 with two minutes left in the third period. The opposing team has pulled the goalie. Don’t screw it up, bud.

TAKE PRIVATE OF THE MONTH

Bayview Takes a View on Guild

When most people think of guilds, they probably remember their days playing RuneScape or WoW. These days, though, guilds can be anything, including mortgage companies worth $1.3 billion, apparently.

Bayview Asset Management has agreed to acquire all of the remaining common equity of Guild for $20 per share, a 56% premium.

Guild is a U.S. mortgage lender and servicer that originates, sells, and services residential mortgage loans. Basically, they help people buy houses, and then keep collecting the payments for years afterward.

If the merger isn’t completed in 2025, existing shareholders (including Bayview) will be entitled to a $0.25 per share dividend, a little gift from Guild for your patience, though it doesn’t adjust the purchase price.

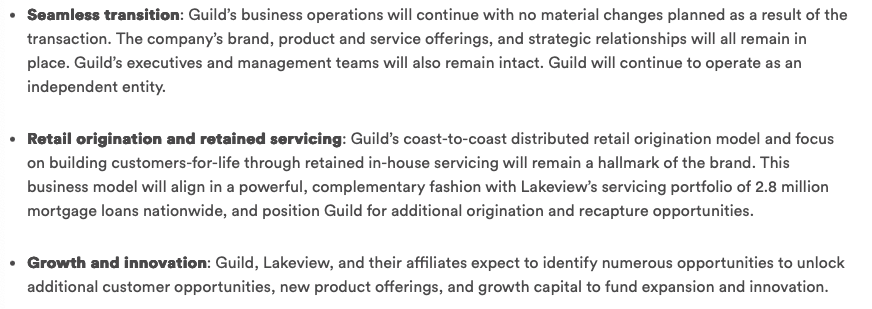

This deal looks and smells like a standard take-private, but Guild already owns another mortgage servicing entity, Lakeview Loan Servicing, so it looks like there will be some synergies on the horizon.

The only FIGs I enjoy are in Fig Newtons, but it’s always fascinating how every industry has its unsexy corners that keep the wheels of capitalism turning.

Sure, everyone knows the big banking giants and flashy mergers like Capital One x Discover. But did you know there’s a mortgage company being acquired at a 56% share price premium and a 26% premium to book value? I didn’t.

So next time you’re putting together strip profile about a business so dull it could put you to sleep halfway through its Wikipedia page, remember: that’s probably the one that will hit.

What'd you think of today's newsletter? |