- Buysiders

- Posts

- One Stream's Instant Take Private

One Stream's Instant Take Private

Plus: Apollo's Dry January and Meta scares away customers.

Short Squeez

January 29, 2026

Together with

Good morning - happy earnings season to all those who celebrate! 2025 was officially the second best M&A year ever topping $5.1 trillion in deals, and 2026 is showing no signs of slowing down.

The markets have been on a wild ride as of late with gold crossing $5,000 / oz, the simp economy continuing to prove its undefeated, and some interesting deals coming down the pipeline to kick off the year.

This week gave us three deals that prove one thing: everyone’s having second thoughts. Whether you’re KKR watching your IPO get taken private 17 months later, Apollo flipping a stake for a cool 0% return, or Meta buying an AI startup so good it scared away its own customers, this week was all about buyer’s remorse and seller’s regret.

So, grab your coffee (or something stronger if you’re in restructuring) and buckle up for this week’s top 3 deals:

Hg takes OneStream private for $6.4 billion

AB InBev buys back its own metal container plants for $3 billion

Meta acquires Manus for $2 billion

Worried AI will take your job? Train the models instead and start using Endex.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

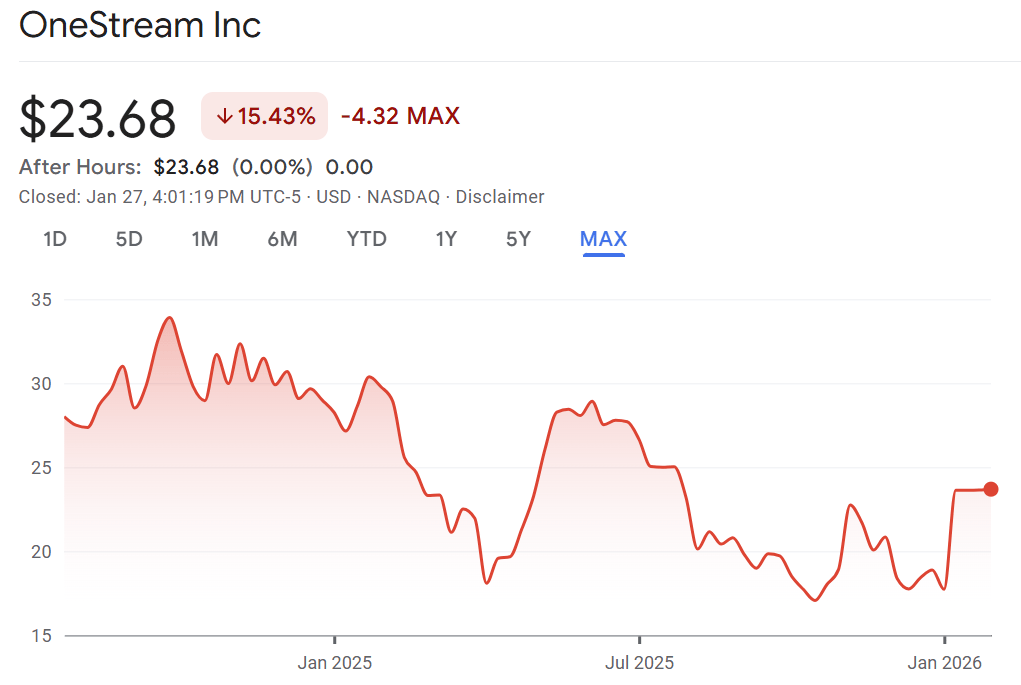

OneStream Goes Private after 17 Months

Nothing says “we believe in you” quite like taking a company private less than 18 months after its IPO. It’s like getting married and then immediately filing for an annulment, except with more Goldman Sachs advisors and fewer emotional damage lawsuits. The legal fees are probably roughly equivalent though.

Hg Capital just agreed to acquire OneStream for $6.4 billion in an all-cash deal, paying $24 per share - a 31% premium to the January 5th closing price. For those keeping track, OneStream went public in July 2024 and performed terribly. Even with a $24/share offer, the stock is still down over 15% all time.

KKR, which took OneStream public in 2024 after buying a majority stake in 2019 for $1 billion, is reportedly thrilled about this outcome. And by “thrilled,” we mean they’re probably wondering why they bothered with the whole IPO charade in the first place. The roadshow. The investor presentations. The regulatory filings. All that work just to have another PE firm swoop in and say “yeah, we’ll take it private again” after a bloodbath in the market.

OneStream is actually a good company. It’s an enterprise finance platform that helps CFOs consolidate, plan, report, and analyze financial data. It’s like Excel that went to business school and won’t stop talking about “AI-driven analytics.”

The company serves over 1,700 customers including 18% of the Fortune 500. Names like Carlyle Group, Nasdaq, and UPS. So we’re not talking about some vaporware startup that spent its entire cash runway on kombucha and standing desks.

OneStream has grown ARR impressively, average 30% growth QoQ, which is great for PE funds to underwrite and something most SaaS companies would kill for. Well…most SaaS companies would probably kill just to have paying customers!

So why go private again? Well, according to CEO Tom Shea, the Office of the CFO is at a “critical AI inflection point.” But also, when someone offers you a 20% premium when your share price is steep enough to be a double black at Stratton, you have a fiduciary duty to take that offer and run.

Hg will invest from its Saturn Fund alongside General Atlantic and Tidemark as minority investors. You know, diversify the risk and all that.

The real winner here is OneStream’s investment bankers. J.P. Morgan acted as financial advisor and provided a fairness opinion. Centerview Partners also provided a fairness opinion. That’s a lot of billable hours to essentially say “yeah, $24 seems about right.”

Public markets are tough, analysts ask hard questions, shareholders expect growth and profitability… how unreasonable. Private equity offers a safe space where you can burn cash on “strategic initiatives” without someone sending passive-aggressive emails about your FCF margin.

But come on - 17 months? That’s not even two full years of audited financials. That’s barely enough time to figure out the good lunch spots in Times Square (spoiler alert - there aren’t any).

The real question is will we be here in 5 years as Hg looks to sell? Only JPM knows (probably).

PRESENTED BY ENDEX

GPT-6 expected Q1 2026. What Will New Launch Mean For Finance?

December’s GPT 5.2 launch brought significant improvements to the LLMs. Analysts, associates, and C-Suites are wondering how close to a true “AI analyst” will we come to in 2026.

Endex, OpenAI’s Excel agent, is already capable of generalist work such as building DCFs, comps, and sensitivity analysis.

Investment banks and PE firms are racing to bring AI agents into their workflows, as they prepare for future LLM breakthroughs.

To request access to Endex, click here.

(WORST) EXIT OF THE MONTH

Apollo’s Dry January

In 2020, AB InBev sold 49.9% of its U.S. metal container plants to Apollo Global Management for $3 billion. The logic was sound: offload some assets, reduce debt from that monster SABMiller acquisition, and retain operational control. You know what wasn’t in the underwriting case? Getting the option to buy it back in five years at the same price.

That’s right, fast forward 6 years and AB InBev is buying the plants back for… $3 billion.

Yes. Apollo held these assets for six years and made…zero dollars in appreciation. Not even a cost-of-living adjustment. Not a “thanks for playing” bonus. Turns out the only thing dry this January was Apollo’s returns.

This might be the most expensive storage unit rental in history. Apollo basically provided AB InBev with a five-year loan secured by aluminum cans. At least U-Haul gives you a complimentary lock. I mean, Apollo could’ve parked $3 billion in treasuries and netted a better return (with less fees too).

Now, to be fair to Apollo (I guess they know what they are doing), they probably collected some cash flows and maybe a management fee or two. But still - $3 billion in, $3 billion out is not exactly the kind of IRR that makes LPs break out the champagne. More like the kind that makes them break out the questions.

Aluminum - the thing that makes your beer can - has been a target for Trump’s trade agenda. The President (who I think just spins a wheel to decide his tariff for the day) imposed a 25% tariff on aluminum imports in March 2025, then doubled to 50% in June 2025.

The US imports a vast majority of its aluminum demand, most of which is primarily from Canada. So, a 50% tariff is pretty bad for margins when you’re producing millions of cans per year from an imported product.

When aluminum costs surge, beer companies have two choices: raise prices and watch Bud Light lose more market share to spirits, or control your own supply chain and pray. AB InBev chose door number two.

The seven facilities across six states produce aluminum cans and lids for AB InBev’s North American portfolio - everything from Budweiser to Michelob Ultra to the new Phorm Energy drink.

AB InBev says the plants are “a strategic component of our business, ensuring quality, cost efficiency, speed of innovation and supply security”, which is corporate-speak for “We realized that letting someone else control whether we can put beer in cans was maybe not our smartest move.”

This comes as AB InBev is investing $300 million in U.S. manufacturing, including $7.4 million in Los Angeles alone, for packaging and brewing equipment upgrades. They’re also expanding in St. Louis and Baldwinsville, New York because comparative advantage doesn’t exist any more.

AB InBev is up 6% since the announcement, meaning just announcing the deal generated more returns in a week than Apollo did in 6 years.

Over all, the deal is a home run for AB InBev. They sold the plants for $3 billion, paid down debt and got a share price bump, then generated enough cash to buy them back with cash on the balance sheet. Hard to draw it up better than that in your investor decks.

STRATEGIC DEAL OF THE MONTH

Manus’ Customers Tell Meta to Get Zucked

You know your acquisition has problems when customers start fleeing before the deal even closes.

Meta just dropped over $2 billion to acquire Manus, a Singapore-based AI startup that makes autonomous agents for complex tasks. It’s like ChatGPT, but it actually does things instead of just talking about them.

Manus can screen resumes, create trip itineraries, analyze stocks, write code, and perform market research. It launched its first product in early 2025 and was one of the fastest platforms to cross $100 million in annual recurring revenue.

The deal valued Manus at ~$2.5 billion, which includes a $500 million employee retention pool - because apparently you need to bribe people to work for Mark Zuckerberg now.

This is just Meta’s latest attempt to justify spending $70 billion annually on AI infrastructure which has amounted to…nothing. I mean, seriously, the AI on Instagram is just in the way of my doom scrolling of AI slop from other platforms.

It’s not all fun and games for Meta or Manus though, with some customers immediately bailing when they heard Meta was buying Manus.

Seth Dobrin, CEO of Arya Labs, told CNBC that Manus was his “favorite agentic AI platform” - past tense. He’s no longer using it under Meta ownership because, and I quote, “I do not agree with a lot of Meta’s practices around data and how they essentially weaponize people’s personal data against them.” Sounds like Mr. Dobrin didn’t read the T&Cs before he joined Instagram.

Dobrin added that he’s “legitimately sad that this has happened.” Which is the professional way of saying “way to f*ck that up”.

This isn’t just one disgruntled customer. Multiple businesses are reportedly reconsidering their Manus subscriptions because they don’t trust Meta with their data, which is probably fair! Meta’s track record on data privacy is like Lehman Brothers’ track record on risk management - technically they tried, but also, gestures vaguely at Cambridge Analytica.

Meanwhile, Flo Crivello, CEO of Manus competitor Lindy, is basically doing cartwheels. His company saw a “bump in users after news of Meta’s acquisition” due to what he calls a “halo effect.”

Now, Meta is trying to spin this as a huge win. They’re integrating Manus into WhatsApp Business API so AI agents can handle complex transactions like rebooking flights and processing payments. So now you can get Instagram ads for places you go to work trips on (the Holiday Inn in Ohio) while an AI agent fights with your admin about a first class ticket it booked on the corporate card.

The great irony while people leave over privacy concerns is that Manus was founded in China before relocating to Singapore. Its backers included Tencent Holdings and HongShan Capital (formerly Sequoia China).

As part of the deal, all Chinese investors were completely bought out to satisfy U.S. national security concerns. So I guess Xi Jinping can know your preferences but once Zuck does it, it’s bad??

China is now investigating the deal for potential export control violations. So Meta has spent $2 billion to buy an AI startup, immediately alienated existing customers, just to now have to explain to Beijing why they’re taking Chinese technology to California.

Meta says Manus will “continue operating its subscription service” and that CEO Xiao Hong will report directly to COO Javier Olivan. The team of about 100 employees will stay in Singapore, Tokyo, and San Francisco (but not Menlo Park).

In short, Meta spent $2 billion on a company so good it scared away its own customers the moment Zuckerberg’s name appeared on the cap table. That’s either the worst pitch deck in history or the most honest customer feedback Meta’s ever received.

NEWS ROUNDUP

Top Reads

China investigating Meta’s $2 billion Manus acquisition for export control violations

China investigating Meta’s $2 billion Manus acquisition for export control violations

JPMorgan M&A chief says CEOs seeking “safety in scale” amid mounting risks

2025 global M&A hits $5.1 trillion, second-best year on record despite Trump volatility

Private equity confidence surges: 86% confident in Q4 vs 48% in Q1

Vistra acquiring Cogentrix Energy for $4 billion as power demand surges

SoftBank closing $4 billion DigitalBridge acquisition in AI infrastructure push