- Buysiders

- Posts

- SoftBank is Back in Deal Mode

SoftBank is Back in Deal Mode

Plus: Quantum makes $1 billion in 18 months and the largest M&A deal ever hits the tape.

Short Squeez

January 20, 2026

Together with

Good morning! 2026 is kicking off with a bang - Masayoshi Son is once again doing Masayoshi Son things and the US is looking to acquire an island. So, whether you’re updating your LinkedIn to “Seeking New Opportunities”, explaining to your MD why you needed that third espresso martini at the Christmas party, or trying to explain why Claude can’t replace you, buckle up for this month’s top 3 deals:

SoftBank buys DigitalBridge for $4 billion to fuel AI infrastructure dreams

Vistra acquires Cogentrix Energy for $4 billion to power the AI revolution

Rio Tinto and Glencore restart talks on $260 billion mining mega-merger

Deal teams are cutting diligence time by 75% with the most advanced AI agent for financial analysis on the market. Check it out today.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

SoftBank Gets Back Into Deal Mode

When Masa sold his entire $5.83 billion Nvidia stake (a move that literally made him cry, according to his own admission), you probably thought he’d learned his lesson about FOMO. I did too.

We were wrong.

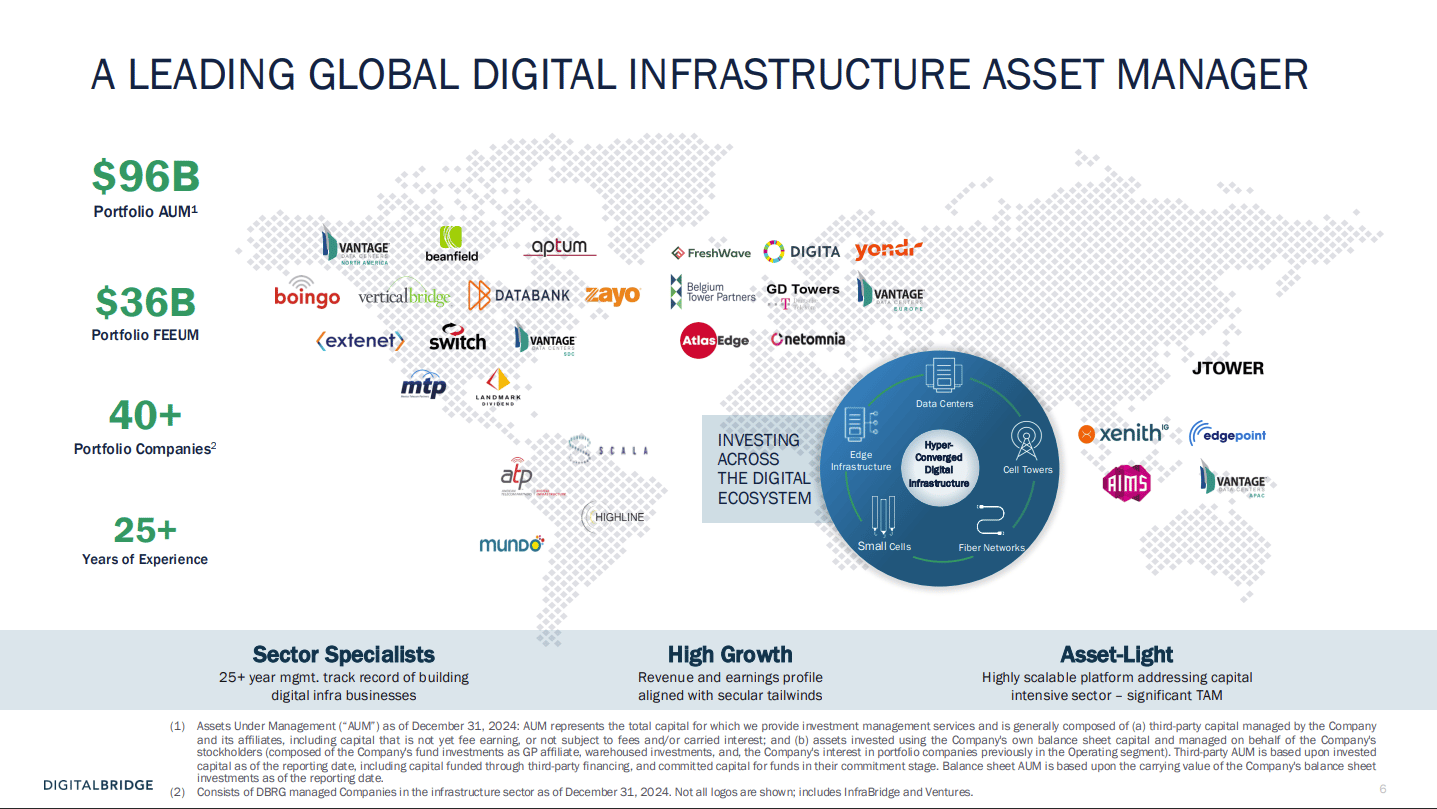

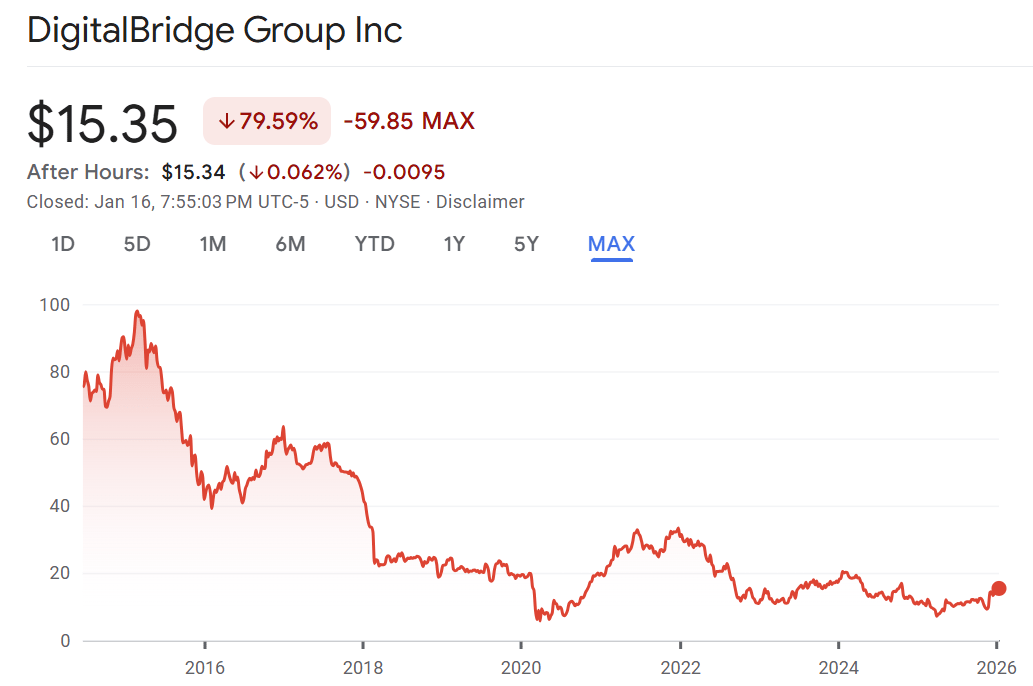

SoftBank is back on the AI train with no regard for purchase price once again after agreeing to acquire DigitalBridge Group for approximately $4.0 billion, paying $16.00 per share in cash - a 15% premium to its December 26, 2025 closing price and a 50% premium to the unaffected 52-week average.

The deal makes perfect sense if you squint and believe in the gospel according to Masa: we’re heading toward Artificial Super Intelligence (ASI), and that requires massive physical infrastructure. While DigitalBridge’s share price graph leaves little to desire - and let’s not forget Altman is rolling out ads to fund OpenAI’s spending - there is no sign of anything slowing down. Bubble? What bubble?

DigitalBridge manages $96 billion in infrastructure assets including data centers, cell towers, fiber networks, and edge infrastructure - basically all the boring physical stuff that makes AI actually work. You know, the parts that don’t get hyped in TechCrunch articles but do jack up your power bill.

This comes right after SoftBank committed up to $40 billion to OpenAI (with $11 billion from third-party investors), plus another $15 billion to OpenAI’s Stargate data center project. For those keeping track at home, that’s approximately $60 billion in AI-related commitments.

“As AI transforms industries worldwide, we need more compute, connectivity, power, and scalable infrastructure,” said Son. Translation: I’m not missing another Nvidia moment, so I’m buying the infrastructure layer this time.

And the most interesting part of the deal? DigitalBridge will continue operating as a separately managed platform led by CEO Marc Ganzi. So SoftBank gets the assets without having to actually, you know, operate them. That may seem smart, but then again…check the tape. DigitalBridge’s share price performance and results have been abysmal.

The deal is expected to close in the second half of 2026, assuming regulators don’t ask too many questions about why a Japanese telecom conglomerate needs to own American data center infrastructure during a time of heightened geopolitical tensions. Maybe Trump will want another Golden Share like he got in the last major Japanese deal (Nippon x US Steel).

But, hey, at least Masa has a plan. Whether it’s a good plan is a question for 2028. Though as he famously said, he’d rather be the crazy guy in a fight.

PRESENTED BY F2

Data Room to IC in 75% Less Time

Whether you're a credit analyst doing a covenant analysis or a PE associate building a LBO model, F2 will make your life A LOT easier.

The platform processes excel models, synthesizes data room documents, integrates market sources like FactSet, and generates investment-grade materials with full auditability.

Used across private credit, commercial banking, and private equity. Teams evaluate deals 75% faster while maintaining the standards investment committees demand.

EXIT OF THE MONTH

Vistra Bets Big on Congentrix

Does it smell like gas in here? Nope, that’s just $4 billion dollars being lit on fire.

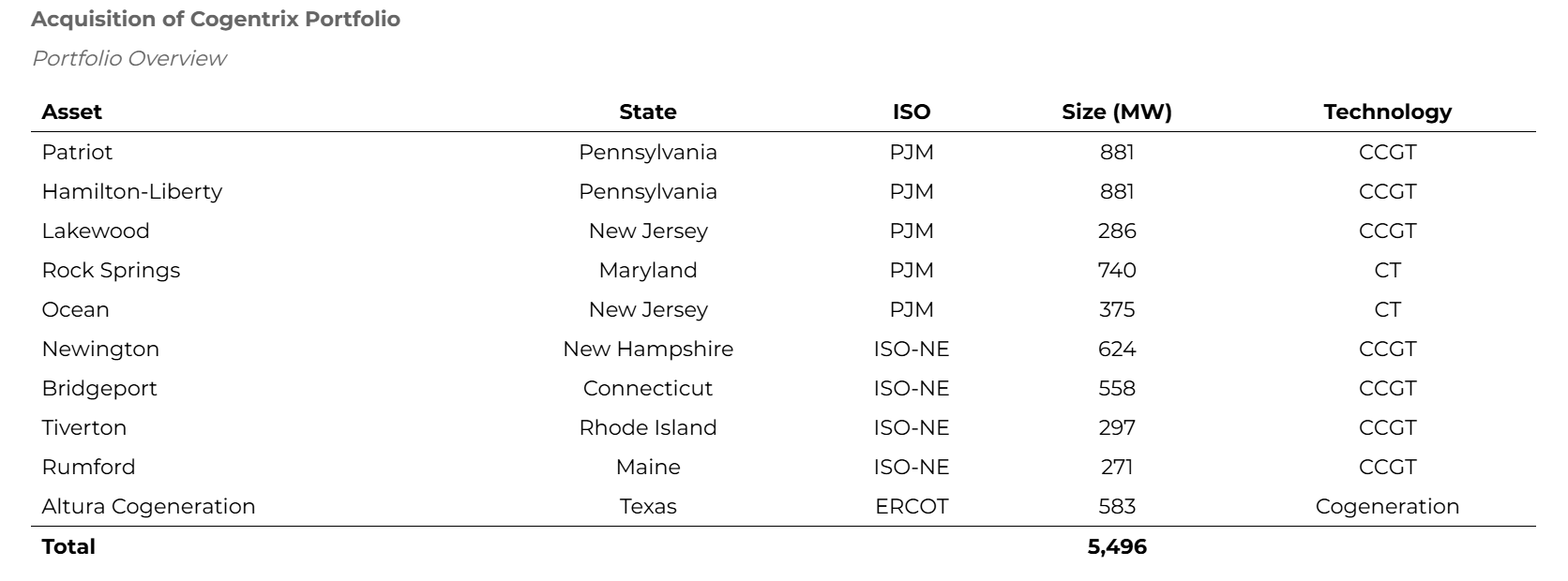

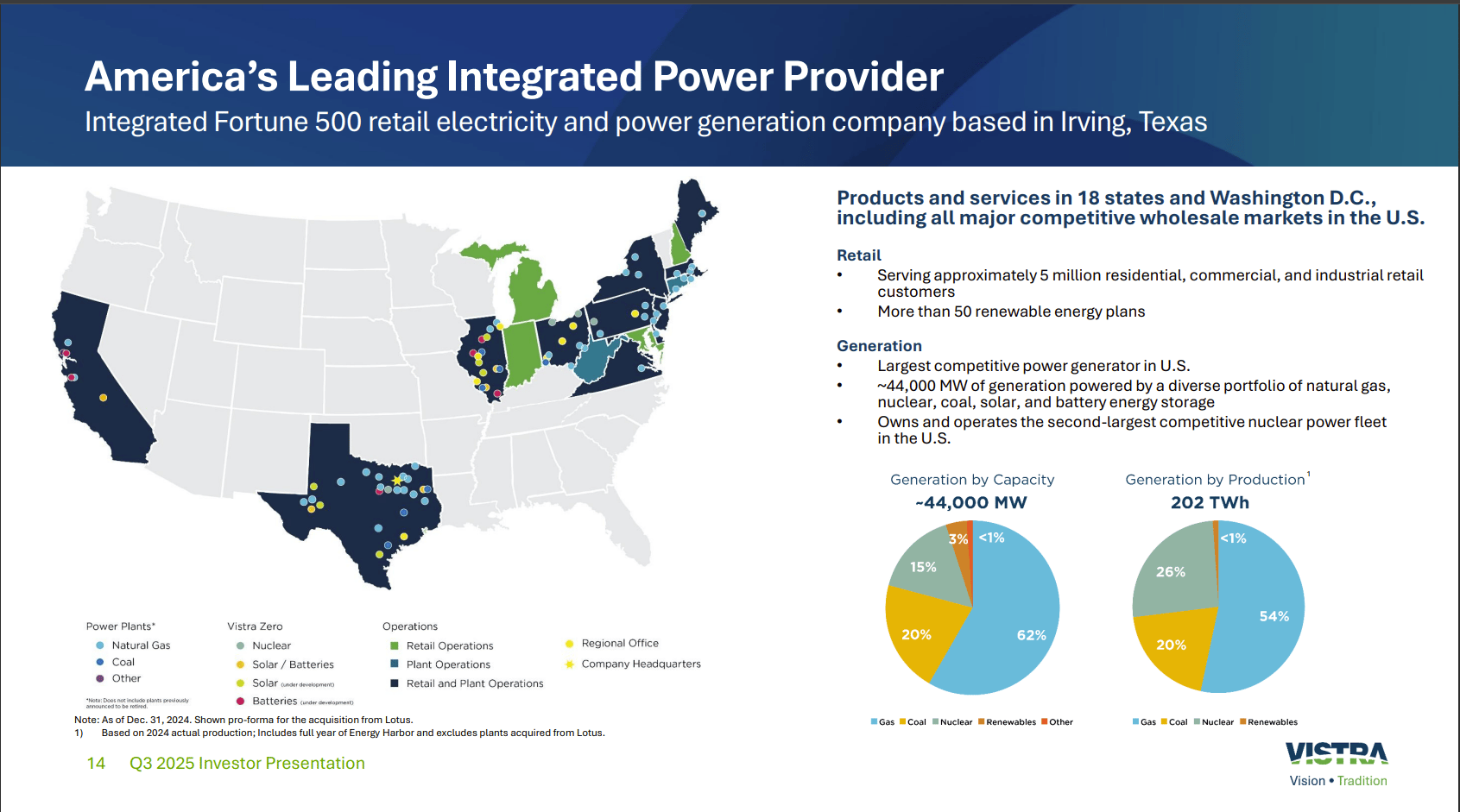

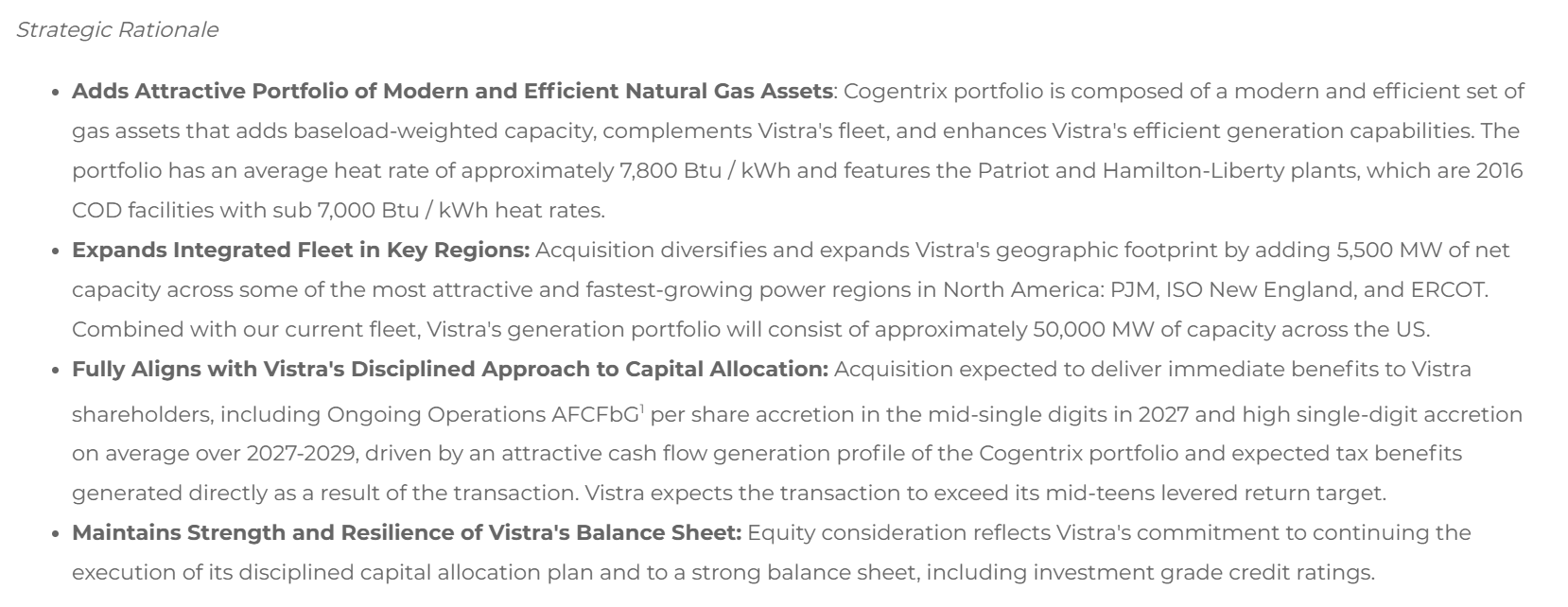

Vistra Corp just dropped $4 billion to acquire Cogentrix Energy and its 10 natural gas generation facilities, adding 5,500 MW of capacity to its already massive fleet. This marks Vistra’s second major acquisition in the past year, following its $1.9 billion deal for Lotus Infrastructure Partners’ assets in May 2025.

The consideration is: $2.3 billion in cash, $900 million in Vistra stock, and the assumption of $1.5 billion in debt, partially offset by roughly $700 million in tax benefits. The transaction is being struck at ~7.25x EBITDA, which is a pretty reasonable valuation given the demand hype.

Cogentrix’s portfolio includes three combined cycle gas turbine facilities and two combustion turbine facilities across PJM, four combined cycle gas turbine facilities in ISO New England, and one cogeneration facility in ERCOT.

For those of you who aren’t in the power world, in short, Vistra just bought its way into some of the most attractive power markets in North America.

Of course this all comes back to the same theme driving all unsexy industries these days - AI. See, AI data centers need power, and they need a lot of it.

Meta just signed a deal to purchase over 2,100 MW of nuclear energy from Vistra. Microsoft, Amazon, and Google are all scrambling to secure long-term power contracts. And unlike some starry-eyed tech founders, these companies actually understand that data centers don’t run on vibes - they run on megawatts and thousands of them.

Post-acquisition, Vistra’s generation portfolio will consist of approximately 50,000 MW of capacity across the US, making it one of the largest independent power producers in the country. The company is betting that the AI boom will drive sustained demand for reliable baseload power - and natural gas is the only fuel that can scale fast enough to meet it.

The financial case is solid: Vistra expects the deal to deliver mid-single digit AFCF per share accretion in 2027 and high single-digit accretion on average over 2027-2029. The company is also reiterating its capital allocation plan, which includes $300 million in annual dividends and at least $1 billion in share repurchases each year.

The one small wrinkle (as always) is regulatory approval.

The deal needs clearance from FERC, the DOJ under Hart-Scott-Rodino, and various state regulators.

With a deal of this scale, there is a high likelihood that FERC at least raises an eyebrow. The good news is that FERC often works quickly…not. The standard approval timeline for deals that aren’t complex is ~180 days from filing.

Given that the DOJ recently opposed Constellation’s acquisition of Calpine, there’s some uncertainty here and this deal may get significant scrutiny.

But here’s the thing - Quantum Capital Group bought Cogentrix from Carlyle for $3 billion in August 2024. They’re flipping it to Vistra for $4 billion just 1.5 years later. That’s a $1 billion gain in less than two years, driven entirely by surging power prices and capacity value. That’ll help the fundraising track record.

If that’s not a signal to everyone that the power market is on fire (again, do you smell gas?), I don’t know what is. All of the AI hype is driving demand across many industries crazy, even ones that we don’t typically think about.

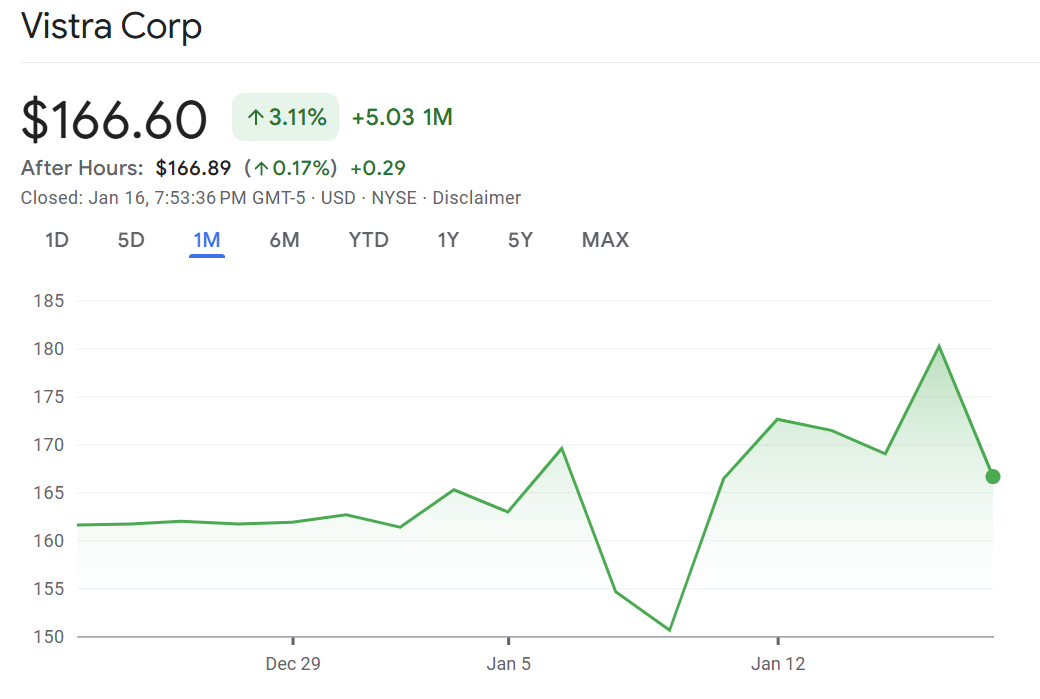

Vistra’s stock jumped 3%+ on the news, and CEO Jim Burke is out here talking about “growing customer demand in our key markets” like he’s selling iPhones instead of electricity.

All of this to say, we basically have two AI deals this month.. .just neither of them are as sexy as we all expected and that’s okay. It’s been a long time since one macro trend has caused such a significant shift across every facet of life.

Nowadays just saying AI gets you a capital raise from a VC in SF, and that is spreading to every industry. I bet if I used AI to write this newsletter - rather than burning the midnight oil and reinventing the wheel each month - I could probably get a few million dollar seed round.

INT’L DEAL OF THE MONTH

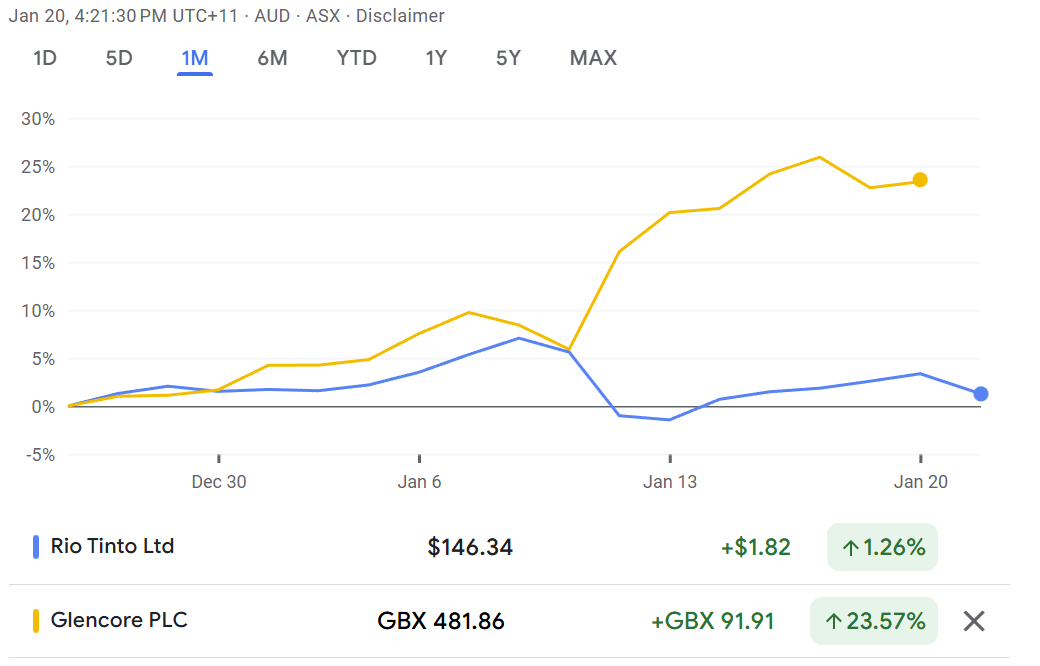

Glencore and Rio’s Tango Continues

Some love stories just won’t die. Rio Tinto and Glencore have flirted with a merger no fewer than four times over the past dozen years, and here we are again - except this time, there’s actual momentum.

On January 8th, both companies confirmed they’re in “preliminary discussions about a possible combination of some or all of their businesses” that could include an all-share merger.

The combined entity would have a market value of more than $200 billion (or $260 billion by some estimates), making it the largest mining company in the world.

So what’s changed since talks collapsed in late 2024:

New Leadership: Rio Tinto’s new CEO Simon Trott took over in August 2025. Unlike his predecessor Jakob Stausholm (who rejected Glencore’s 2024 approach), Trott was reportedly selected because the board wanted someone more open to large-scale deals.

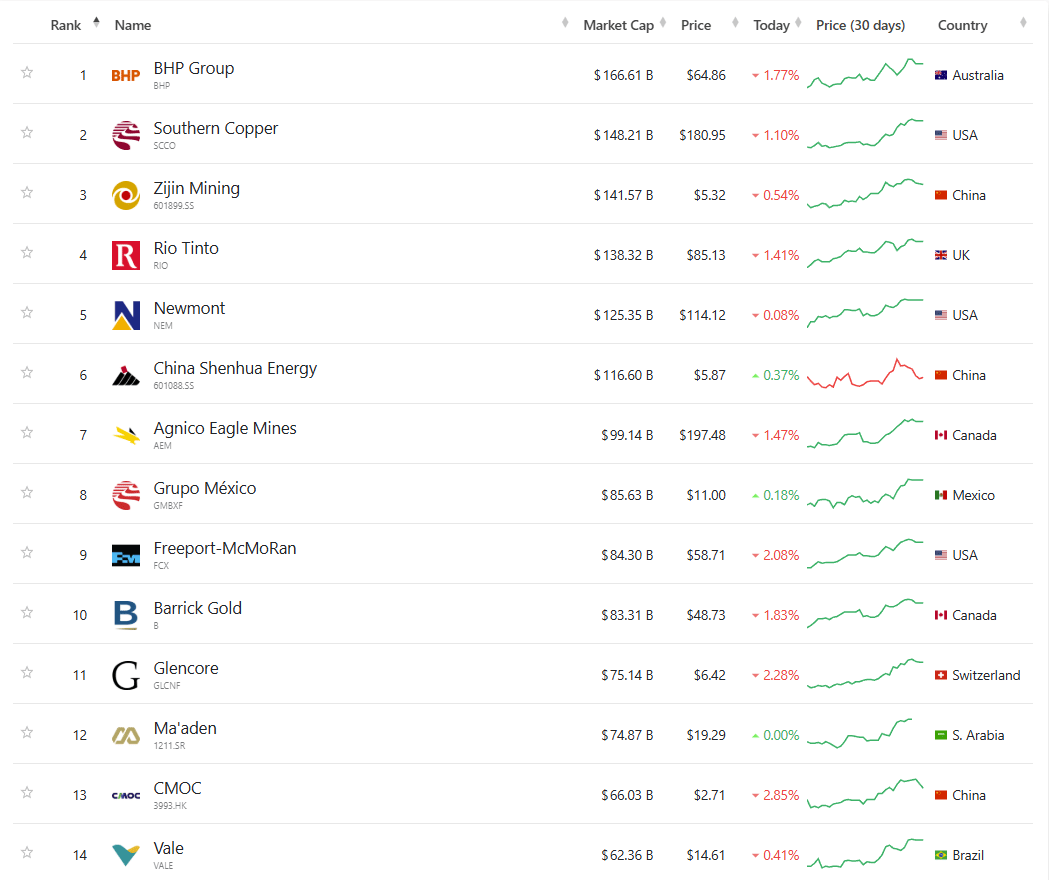

Copper Hype: Global miners are in an arms race for copper assets. The metal is critical for the energy transition and AI infrastructure (hey, there’s that AI theme again). Rio Tinto wants more copper exposure. Glencore is copper exposure.

FOMO: Anglo American and Teck Resources agreed to a $53 billion copper-focused merger last September. BHP has been trying to buy someone - anyone - to bolster their copper portfolio. This deal would leapfrog all of them.

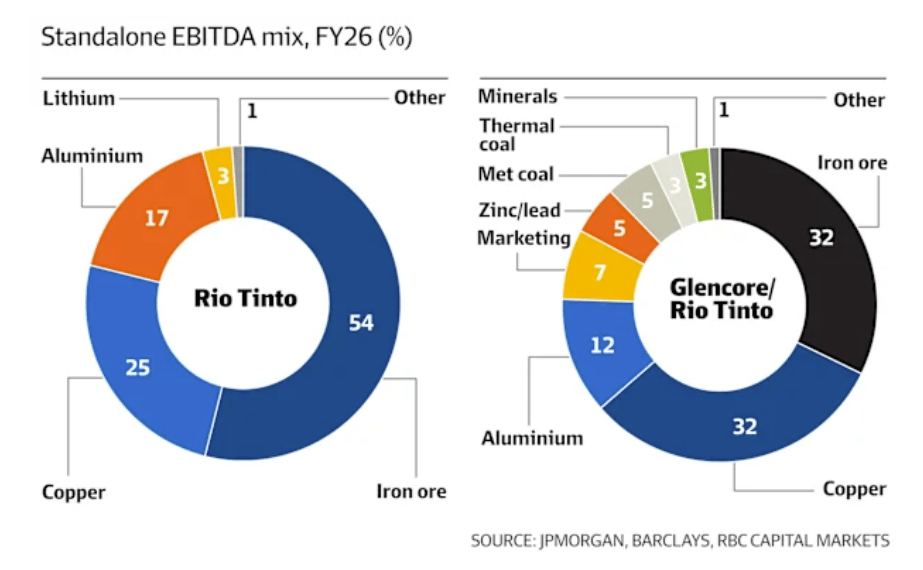

Strategically, a deal makes a lot of sense for Rio Tinto. It gives access to Glencore’s world-class copper assets, plus exposure to cobalt, nickel, and zinc. The combined entity would control approximately 17% of global copper supply marketing and 7.5% of mine production globally.

On the Glencore side, they are looking at a nice premium, plus access to Rio’s iron ore and aluminum portfolios. Glencore CEO Gary Nagle has made it clear: “everything is for sale at the right price, including the entire company.”

Barclays estimates the combined company would generate $10 billion in synergies through cost-cutting and operational efficiencies. I mean, with the ability to basically remove an entire corporate office, you are already looking at significant cost savings before you include all of the operational efficiencies being a $260 billion behemoth would provide.

While this all sounds like a no brainer during your MD’s pitch - this deal faces some serious hurdles:

The China Problem: Beijing has to approve any deal of this scale, and they’re likely to demand asset sales. When Glencore bought Xstrata for $35 billion in 2013, China forced them to sell the Las Bambas copper mine in Peru for nearly $6 billion. Expect similar demands this time, especially for African assets.

The Coal Problem: Glencore owns massive thermal coal assets that Rio Tinto probably doesn’t want. Most expect Glencore to spin off coal in a tax-free transaction before any merger - which would be ironic given Trump’s “coal is coming back” rhetoric. Glencore shareholders previously voted to keep the steelmaking coal assets as they offer strong recurring cashflows to fund expansion projects.

The Valuation Problem: Rio Tinto’s Australian shares fell 6.4% when talks were announced, suggesting shareholders think Rio might overpay. Glencore shares jumped 10%, suggesting the opposite. Someone is going to be disappointed.

Under UK takeover rules, Rio Tinto has until February 5, 2026 to either make a formal offer or walk away. That’s about two weeks from now as of this writing.

The enterprise value could exceed $260 billion, which would make this one of the largest M&A deals in history, surpassing Vodafone’s $183 billion acquisition of Mannesmann in 2000.

As a former mining junky myself, I think this deal has better odds than the previous attempts, but it’s far from certain.

If Rio can structure it as a nil-premium or low-premium merger (as some reports suggest Trott is considering), shareholder resistance might ease. If they have to pay a 20-30% premium to Glencore shareholders, it’s going to be a tough sell.

Either way, we’ll know in a few weeks whether mining gets its mega-merger or if Rio and Glencore go back to their respective corners for another year.

NEWS ROUNDUP

Top Reads

Big Pharma enters 2026 with appetite for deals at JPMorgan Healthcare Conference

JPMorgan M&A head says 2026 could be banner year as CEOs seek safety in scale

Global M&A volumes hit $3 trillion in 2025, up 33% YoY with 45 mega deals over $10 billion

Bain reports 2025 marked second-highest M&A total on record at $4.8 trillion

Private equity firms increasingly confident with 86% feeling confident in Q4 vs 48% in Q1

Anglo American-Teck Resources $53 billion copper merger nearing completion

What'd you think of today's newsletter? |