- Buysiders

- Posts

- The Largest M&A Deal Ever

Together with

Good morning! It has been a tumultuous week in the markets. Gold shot up to $5,500 then cratered almost immediately, Bitcoin proved that it’s worthless once again, and major tech companies and PE megafunds had volatility that would make penny stocks jealous.

If you’ve been too preoccupied with Anthropic’s new AI tool to track the market savagery, we saw over $1 trillion in market value wiped out from the software sector in two days. Seriously, don’t check your portfolios it’s a bloodbath out there.

And, if you came here looking for respite from the mounds of snow on the sidewalk or as a coping mechanism for your portfolio performance, you seriously need a therapist, but for now, here are this week’s top 3 deals:

SpaceX and xAI merge in the biggest deal in history

Zijin Mining acquires Allied Gold for C$5.5 billion

Boston Scientific acquires Penunmbra for $14.5 billion

Ornn AI has built the financial infrastructure for the AI economy. Trade it here.

First time reading? Sign up here.

Have feedback? Respond here.

DEAL OF THE MONTH

The Biggest M&A Deal in History

Run it back - Elon has done it again.

Just because your girlfriend tells you size doesn’t matter doesn’t make it true. When the largest M&A deal is an option, you tend to ignore all of the average M&A deals who have great personalities…I mean synergies.

Who else but Elon could pull off the largest deal in history, a month into the year?

SpaceX officially acquired xAI on February 2nd in a deal that values the combined entity at $1.25 trillion. Yes, trillion, with a T, as in “Tesla investors are nervous.”

SpaceX is valued at $1 trillion, while xAI comes in at $250 billion. For those keeping track at home, when Elon pulled these shenanigans just 9 months ago merging X and xAI, xAI was only valued at $80 billion.

That’s a cool 3x in 9 months. Not bad for your valuation marks.

The deal is structured as a share exchange, converting each xAI share into 0.1433 shares of SpaceX stock. Documents show xAI priced at $75.46 per share and SpaceX at $526.59 per share. Bank valuations peg SpaceX between $859 billion and $1.26 trillion and xAI between $219 billion and $294 billion, which is banker-speak for “we have no idea but these numbers sound like they will win us the mandate.”

Additionally, this is officially the largest merger in history, surpassing Vodafone’s $183 billion acquisition of Mannesmann in 2000.

Keep in mind, xAI was only founded in March 2023, so it went from zero to a $250 billion (paper) valuation in just 30 months.

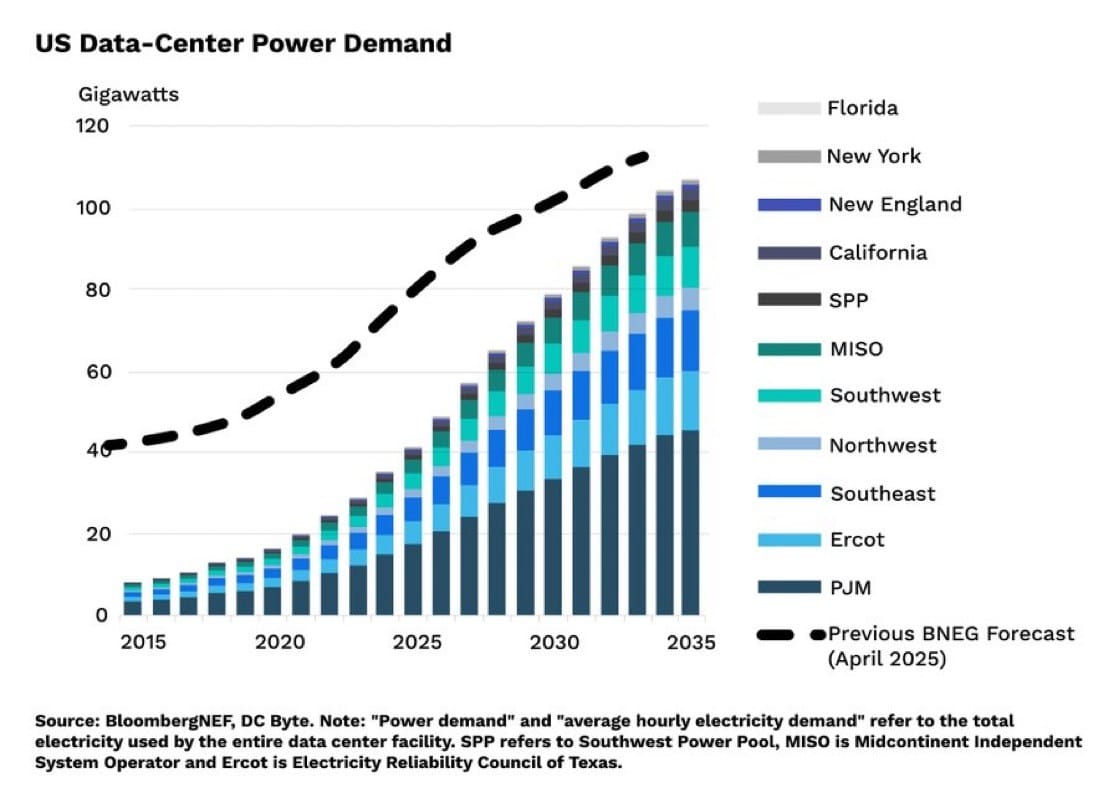

Here’s Musk’s pitch: AI needs compute. Compute needs power. Power is limited on Earth. Solution? Put data centers in space.

Recognizing you can’t just accept what Elon says (obviously), I did some digging because - while Elon has generated insane amounts of shareholder value - he also has a tendency to say some out of this world things.

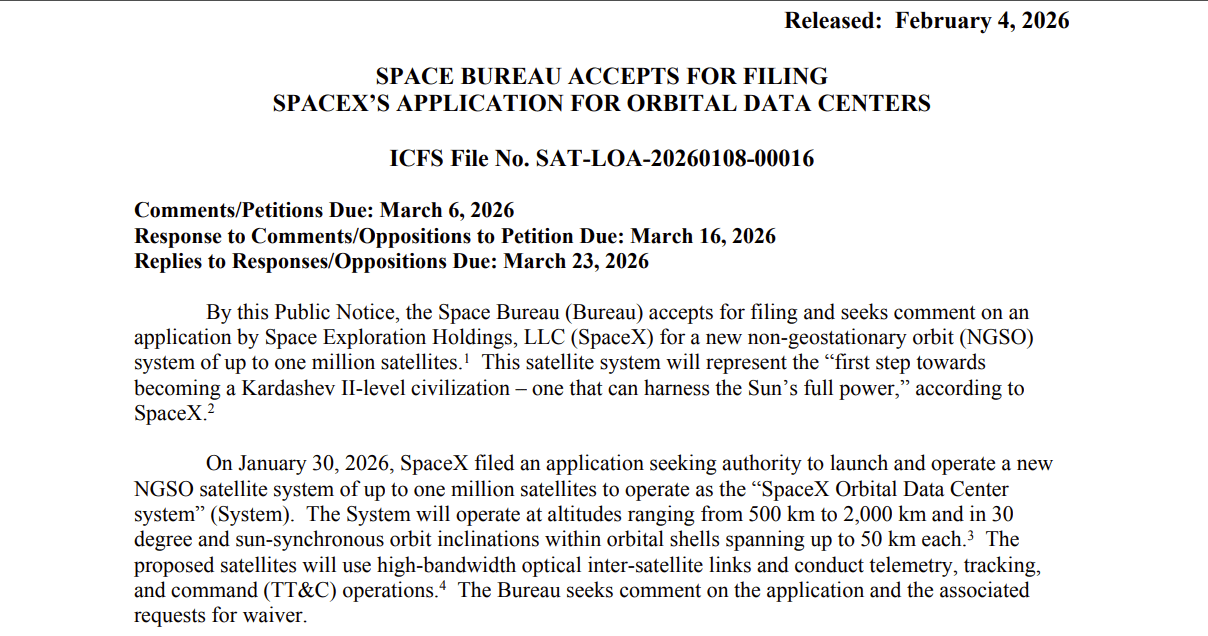

Turns out, on January 30th, SpaceX filed with the FCC requesting permission to launch up to 1 million satellites to support orbital data centers… because apparently 8,000 Starlink satellites weren’t cluttering low Earth orbit enough.

I’m not going to comment on whether or not Elon can pull this off, I am the furthest thing from a rocket scientist, but filing with the FCC proves this isn’t just a moonshot idea.

In a break from his normal cadence of “Interesting” and “Good” retweets on X, Elon wrote in a memo: “Current advances in AI are dependent on large terrestrial data centers, which require immense amounts of power and cooling. Global electricity demand for AI simply cannot be met with terrestrial solutions.”

And he’s not wrong. Global electricity demand is going to struggle to keep up with AI needs. That’s a fact (think about that next time you ask ChatGPT to write your confirming receipt emails). But certainly there are options before datacenters in space… I can’t think of any, but if I could, I wouldn’t have to write a newsletter at 1am now, would I?

So, you’re probably wondering why Elon would do this. I mean, surely shareholders won’t let him just empire build because he feels like it before SpaceX’s IPO, right?

SpaceX gets immediate access to xAI’s Grok chatbot (which is best known for letting users generate questionable AI images before anyone noticed) and the xAI Colossus supercomputer cluster. They also inherit all of xAI’s regulatory headaches, including ongoing probes in multiple countries for enabling non-consensual AI-generated imagery. Have fun putting that in your football field.

xAI gets saved from burning ungodly amounts of cash. xAI was hemorrhaging money trying to compete with OpenAI, Anthropic, and Google, none of whom have the benefit of being able to launch their servers into orbit. Now they have SpaceX’s $8 billion in estimated 2025 profit to fund their computing needs.

X is just along for the ride at this point. The platform generates $2.9 billion in revenue (down from $4.4 billion in 2022) and carries $1.2 billion in annual debt costs, so it’s basically break-even. The obvious solution? Fold it into an AI company and then fold that into space company.

The combined company is reportedly preparing for an IPO in mid-2026, potentially June 28th to coincide with Musk’s birthday and a planetary alignment. I want to know what brave banker said “Elon, you’re an asparagus, so let’s IPO in June”.

Whether or not this is just another half-baked insane Elon idea or a stroke of true genius remains to be seen. The one thing I know for sure is I am probably not betting against the guy who has a substantial amount of his $850 billion net worth riding on getting datacenters into space.

Love or hate Elon, the guy has conviction. Whether that conviction is enough to get one million satellites into space, I have no idea. But if anyone can do it, it’s probably him.

(For those that won’t to go further down the rabbit hole, here’s a 3 hour podcast from this week where Elon discusses space data centers)

PRESENTED BY ORNN AI

The Ornn Index: S&P 500 for Accelerated Compute

GPU compute pricing is messy because compute isn’t interchangeable. An H100 in Dallas is not the same as an H100 in Norway, and the same chip can behave very differently depending on the provider, networking, uptime, and counterparty risk.

But capital providers still have to price it.

Right now, lenders, neoclouds, and data center builders are making multi-year commitments using list prices, surveys, guesswork, and assumptions that don’t map to reality.

Ornn is building the missing reference layer: indices based on actual GPU compute transactions, not quoted rates. Think of it as WTI for high-performance compute, giving the market a common benchmark without pretending everything is identical.

Compute doesn’t need to be fungible. It needs to be observable.

NEWS ROUNDUP

Top Reads

Global M&A hits $5.1 trillion in 2025, second-best year ever as mega-deals return

JPMorgan predicts 2026 could be “banner year” for M&A as CEOs seek safety in scale

Merck reportedly in talks to acquire Revolution Medicines for up to $32 billion

Rio Tinto-Glencore mega-merger talks continue with February 5th deadline looming

INTERNATIONAL DEAL OF THE MONTH

Zijin’s Golden Ticket

Here’s a skill testing question for you all: what happens when the price of gold clears $5,000 / ounce and western companies have larger ESG departments than corp dev departments?

The answer - China snaps up everything it can.

Zijin Mining Group agreed to acquire Allied Gold for C$5.5 billion (what is that, like $12 and two moose in real currency?) on January 26th, marking China’s most aggressive move yet to dominate African mineral resources.

This is Zijin’s eighth major gold acquisition since 2020. For comparison, most Western miners completed zero. But hey, at least you have a banging sustainability report to point to.

The deal is all cash, being struck at C$44 / share, and representing a 27% to the 30-day VWAP.

Unsurprisingly, Allied Gold has traded up pretty materially, and has well exceeded the rip in gold prices.

What’s more offensive is the multiple. The deal is being struck at a 12.7x TEV / EBITDA multiple. I mean talk about overpaying at the peak of the cycle.

Allied Gold operates three producing mines and one development project in Africa and offers the world’s largest gold producer an opportunity to expand its footprint in the region with several long-lived assets.

Combined, these assets were expected to deliver ~400,000 ounces of gold in 2025. Post-acquisition, Zijin’s African gold production will approach 1 million ounces annually by the end of the decade.

For context, Barrick Gold—the Western world’s second-largest gold miner—is guiding towards 3.1 million ounces of gold produced globally in 2025. Zijin is now a quarter of that size just from African assets alone.

Zijin’s Chairman Hongfu Lin called Sadiola and Kurmuk “generational assets which we expect to provide multi-decade production”, which is corporate-speak for “your grandchildren are going to be mining these.”

The deal requires no financing conditions, Zijin is paying entirely from cash on hand and existing liquidity. Meanwhile, Western mining companies are out here doing bought-deal financings and desperately trying to divest non-core assets despite all time high pricing.

Zijin’s market cap now exceeds $70 billion. Its publicly-traded subsidiary, Zijin Gold International (listed in Hong Kong in September 2025), hit a record high after announcing the deal, jumping 13% in a single day (helped by high gold prices as well).

Compare that to Western miners who are barely outperforming the commodity while most junior miners are still trying to explain why their feasibility studies keep getting delayed.

This deal highlights China’s systematic strategy to control strategic resources in Africa while Western companies divest. Newmont—the world’s largest gold producer—has been actively selling African assets, including the Akyem mine in Ghana which it sold to…Zijin Mining.

The geopolitical implications are staggering. Gold has transformed from a commodity into a strategic reserve asset for China. These African mines will feed into “South-South” trade routes, with bullion refined and cleared through Shanghai and Hong Kong instead of London or New York.

China is building a parallel commodities ecosystem that operates outside the USD-dominated financial system. And they’re doing it by buying actual mines with actual gold while Western institutions debate the merits of gold-backed ETFs.

The deal requires approval under the Investment Canada Act because it’s a significant Chinese acquisition of a Canadian company with strategic mineral assets. There’s no guarantee Ottawa will approve it, especially given current geopolitical tensions.

All in all, Zijin is buying at the peak - for sure - but it’s also partially state owned, which means it has practically unlimited money and a relatively low cost of capital. So even if the returns are not something that may get you excited, for Beijing, this is a strategic play more than an IRR play.

STRATEGIC DEAL OF THE MONTH

Boston Scientific Buys Back into Neurovascular

Nothing says “we screwed up” quite like paying $14.5 billion to re-enter a market you exited for $1.5 billion and a firm handshake 15 years ago, but hey welcome to my healthcare corner.

Boston Scientific agreed to acquire Penumbra for $14.5 billion on January 15th, marking its largest acquisition in over two decades and a spectacular admission that selling its neurovascular business to Stryker for $1.5 billion in 2011 was…suboptimal.

Back in 2011, Boston Scientific was convinced neurovascular wasn’t strategic. The market was small. Growth was uncertain. Better to focus on core cardio assets and let someone else deal with stroke devices (get your head out of the gutter).

Fast forward to 2026: The neurovascular market is booming, mechanical thrombectomy is a multi-billion dollar category, and Boston Scientific just agreed to pay 10x what it sold for to get back in. Absolutely tremendous foresight. I hope the corp dev team get’s a round of drinks for that one.

The deal values Penumbra at $374 per share, a 19% premium to its mid-January closing price.

The consideration is 73% cash ($11 billion) and 27% stock, which Boston Scientific will fund through cash on hand and new debt. Considering their current cash balance is sitting at right around $1 billion, it’s safe to assume that the cash on hand piece is a pretty small part of the overall pie.

Penumbra makes mechanical thrombectomy devices (fancy name for “clot removal tools”) used to treat stroke, pulmonary embolism, and deep vein thrombosis. Its flagship products include the Lightning Bolt and Lightning Flash systems, which are legitimately best-in-class technology.

Boston Scientific CEO Mike Mahoney tried to spin this as a strategic masterstroke: “We’ve really been looking for a long time on how to become a scaled, market-leading neurovascular company, not one that’s coming from a distance behind the pack.”

I get waiting for the right opportunity, but hear me out. You could’ve just… not sold the business in the first place?

The initial market reaction tells you everything: Penumbra shares surged 14% to meet the offer price. Boston Scientific shares dropped as investors processed the valuation and debt load.

Shares of Boston have come off further (dropping 17% on February 4th) after its most hyped medical device hit a snag. Not great when you just loaded up on $10 billion of debt.

Penumbra co-founder and CEO Adam Elsesser elected to receive 100% of his consideration in Boston Scientific stock, which is either a massive vote of confidence or evidence that he believes his tax advisor more than his investment banker.

I will be the first to tell you that the healthcare space is probably my least favorite industry. I don’t understand it, I never have, and to be honest I find the hassle of doctors and insurance insufferable.

That being said, a $14 billion deal is a $14 billion deal. While I can make fun of Boston Scientific for buying in at over 10x what they sold out for, I do hope that this works out for them, though the market doesn’t seem too bullish on the added leverage.

What'd you think of today's newsletter? |