- Buysiders

- Posts

- Ground Control to Major Elon

Ground Control to Major Elon

Plus: BP exits Germany and Boralex Goes Private

Short Squeez

March 31, 2026

Together with

Good morning! Well, probably not. I haven’t checked the market yet because I am too scared, but based on last week, I doubt anyone is having a good morning. Despite the market getting absolutely crushed, deals are still happening. Maybe that’s because the firms that can do deals have been amassing war chests and waiting for a moment like this. Or at least, that’s what they will put in their investment memos.

As the dust settles on Trump’s Iran plans, there were still 3(ish) deals done this week:

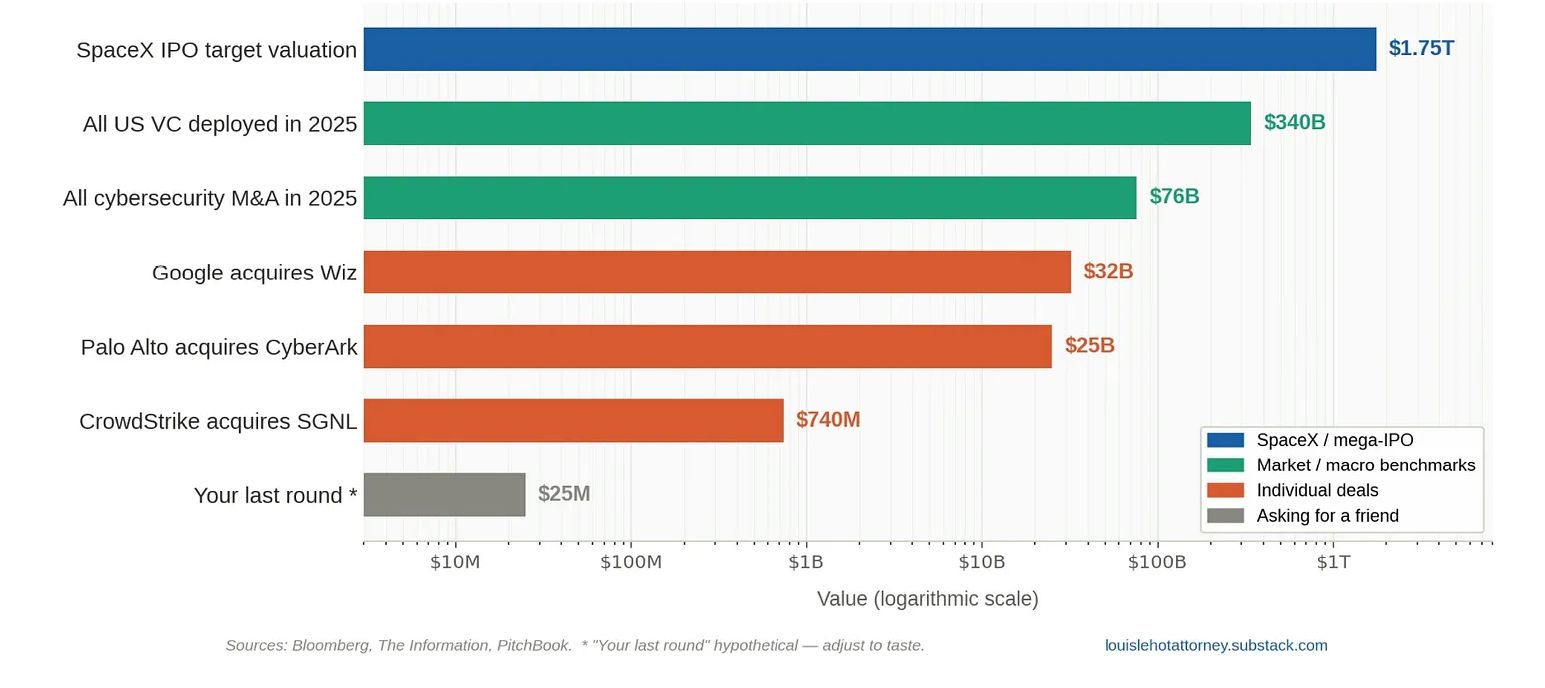

SpaceX’s $1.75 trillion IPO is expected to file in the coming weeks

Boralex goes private for a 34% premium

BP exits its German refinery for an undisclosed price

The best finance workflows start with a plan. Build the perfect agent workflow with Plan Mode from F2.

If you haven't checked out Wall Street 360 yet, now's the time. We built the most complete comp and culture dataset on Wall Street: 600+ firms, every metric from base, bonus and carry to mental health, physical health, weekends worked, and burnout score by firm. See exactly how you stack up against your peers.

DEAL OF THE MONTH

Ground Control to Major Elon

Can you hear me, Major Elon?

I may have dated myself with that reference, but SpaceX has spent 24 years doing things that most people said were physically impossible.

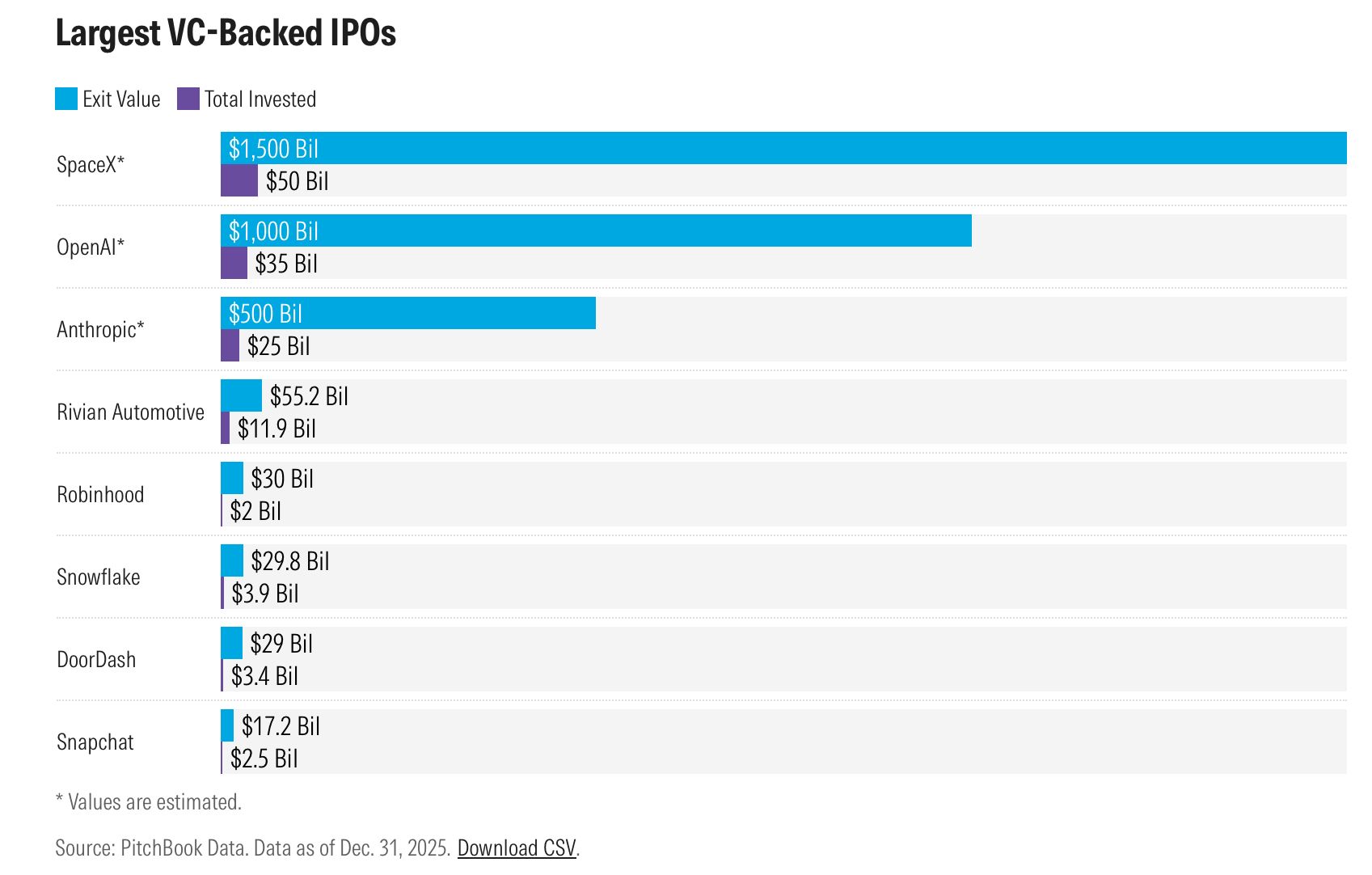

Now, it’s doing something that most people said was financially inconceivable: filing confidentially with the SEC for an IPO targeting a valuation of $1.75 trillion, which, if it prices anywhere near that level, will be the largest public offering in the history of capital markets.

In fact, if SpaceX were a country, it would be the 16th largest country by GDP.

Reports emerged on March 26 that SpaceX is preparing to file a confidential S-1 prospectus with the SEC, targeting a June 2026 Nasdaq listing at a valuation between $1.5 and $1.75 trillion.

The company has lined up Bank of America, Goldman Sachs, JPMorgan, and Morgan Stanley for senior underwriting roles so the four largest banks on Earth are about to spend the next sixty days arguing over tombstone placement on what could be the most lucrative IPO mandate in history. Someone is going to get the top-left box, and someone else is going to be furious about it at the closing dinner.

To understand why $1.75 trillion is at least a defensible number, not necessarily a reasonable one, but defensible none the less, you have to understand what SpaceX actually is in 2026.

It is not primarily a rocket company. It is a satellite internet provider with nine million paying subscribers, a defense services contractor with billions in government commitments, and — following the xAI merger — an AI infrastructure business building orbital data centers powered by the sun. If you told me a year ago I’d write that in a sentence, I would’ve called you insane.

Starlink alone generated over $10 billion in revenue in 2025, with margins that would embarrass most software companies. SpaceX as a whole reportedly generated $8 billion in profit on $15–16 billion in revenue last year. That is a real business, you know, with cash flow and everything.

Then there is the February merger with xAI, which closed at a combined valuation of $1.25 trillion and which, depending on who you ask, was either a stroke of visionary vertical integration or the most audacious related-party transaction in private market history.

As a refresher, SpaceX acquired xAI in an all-stock reverse triangular merger, with xAI employees given the option to redeem shares for cash. There was no fairness opinion from an investment bank. There was no special committee. There was a blog post from Musk and a valuation that was, by most accounts, set internally.

The SEC is apparently taking a close interest in how all of this gets disclosed in the S-1, which partially explains why the filing is going in confidentially and why a June listing was originally supposed to happen in April.

Elon is no stranger to rubbing the SEC the wrong way. Remember when he tweeted (yes, pre-X) about TSLA going private?

The planned dual-class share structure means that even after going public and raising up to $50 billion in primary capital, Musk, who currently owns more than 40%, will retain dominant voting control over the company.

There is also an unusually large 20–30% retail allocation reportedly being pushed by Musk, who has apparently decided that keeping his fan base liquid and invested is as important as keeping the institutional books covered. Whether that results in a more stable stock or a more volatile one is a question the secondary market will answer on day one.

One detail being underreported: SpaceX plans to take advantage of the confidential filing process, which allows it to meet SEC requirements and address financial disclosures privately before initiating a public roadshow.

This is particularly important given the complexity of integrating xAI’s liabilities, intellectual property, and revenue into SpaceX’s consolidated financials, plus the defense contract sensitivities that come with being the Pentagon’s favorite rocket supplier.

Imagine the poor SEC gremlin who has to look at a rocket launching social media company that also runs a telecom empire and is somehow also an AI company? Oh, and by the way, every time Elon tweets there will probably have to be an 8-K.

When the S-1 goes public, likely in April or early May, it will be the most-read document on Wall Street since the Facebook prospectus. Every number will be stress-tested. Every Musk quote will be pulled for the risk factors section, especially funding secured. Every analyst will be writing a 47-page initiation report by the following Monday.

There is a version of this story where the SpaceX IPO is the defining capital markets moment of this decade, the trade that either confirms or destroys the argument that private market valuations have become untethered from reality.

The June IPO is projected to be the largest in history by cash raised, potentially surpassing the $29.4 billion proceeds of Saudi Aramco’s 2019 debut.

Whether investors ultimately pay $1.75 trillion for the privilege of owning a rocket company, a satellite internet service, an AI subsidiary with a controversial chatbot, and whatever X has become at this point — is also a question for June.

For now, the banks are engaged, Elon Musk is preparing to take the most valuable private company in history public, and, according to the Financial Times, all of it coincides with his birthday and a planetary alignment. Naturally.

PRESENTED BY F2

AI That Won’t ‘Jump the Gun’

Isn’t it the most frustrating thing when you prompt GPT, Claude, Grok (insert your favorite finance AI here), and they immediately jump to working rather than listening and planning?

Thus follows the typical AI workflow in finance:

1) Run it. 2) Review it. 3) Find assumption errors. 4) Redo it.

While AI may be helpful, it has a tendency to act first and ask questions later (unless prompted).

Plan Mode from F2 lets you review the entire workflow before it runs:

the logic

the assumptions

the build path

Build the plan upfront, let the agents handle the grunt work.

This equates to fewer drafts, faster outputs, and way less time retracing steps.

See how Plan Mode works.

PE DEAL OF THE MONTH

Boralex Bids the Public Markets Adieu

There is a specific category of company that private equity, and infrastructure PE in particular, absolutely cannot resist: a well-run, cash-generative, publicly-listed infrastructure business whose shares are trading at half of where they were five years ago because interest rates went up and the market decided it didn’t like renewable energy anymore. Boralex is that company. Brookfield is that buyer. The only mystery is why it took this long.

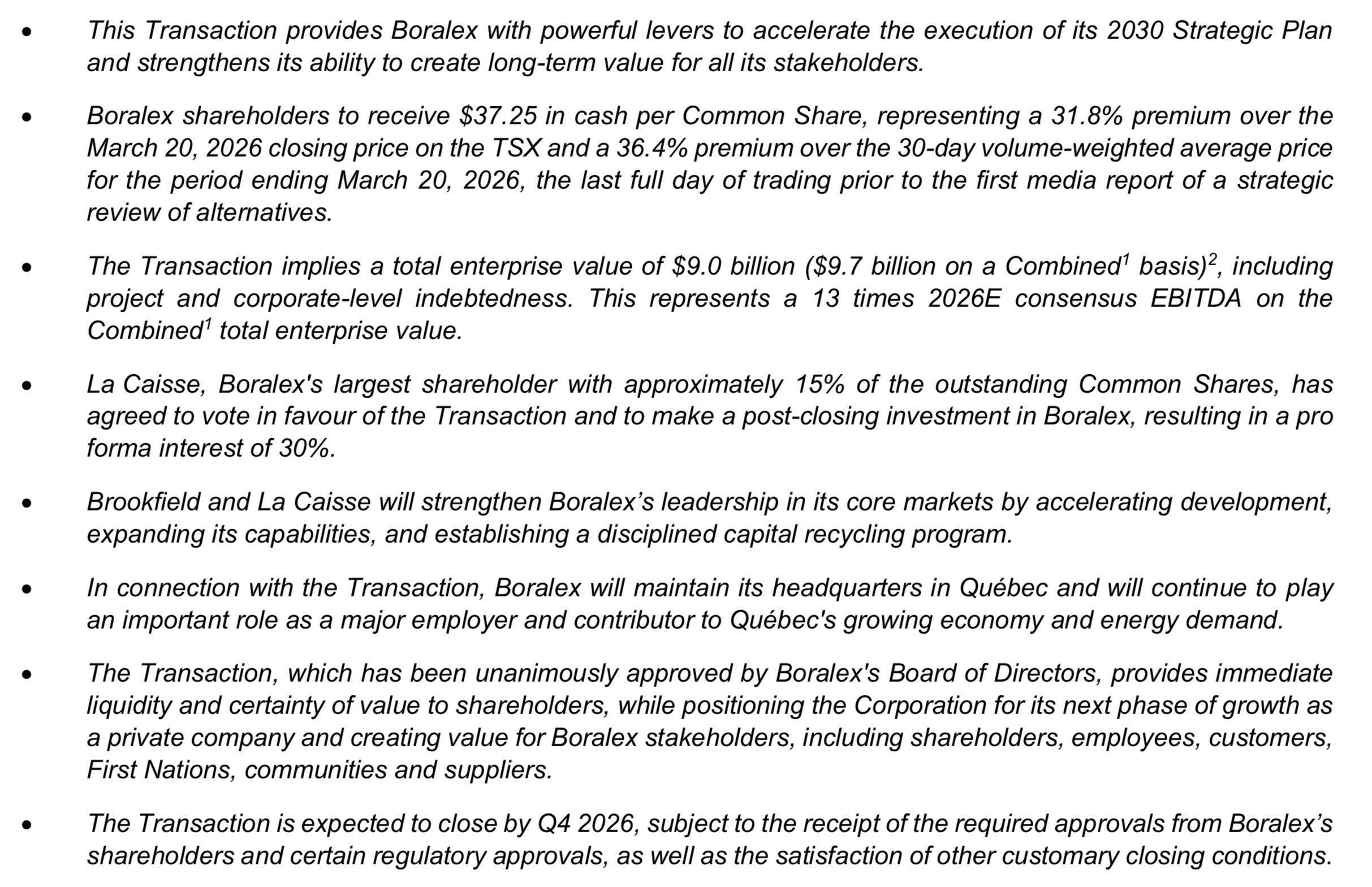

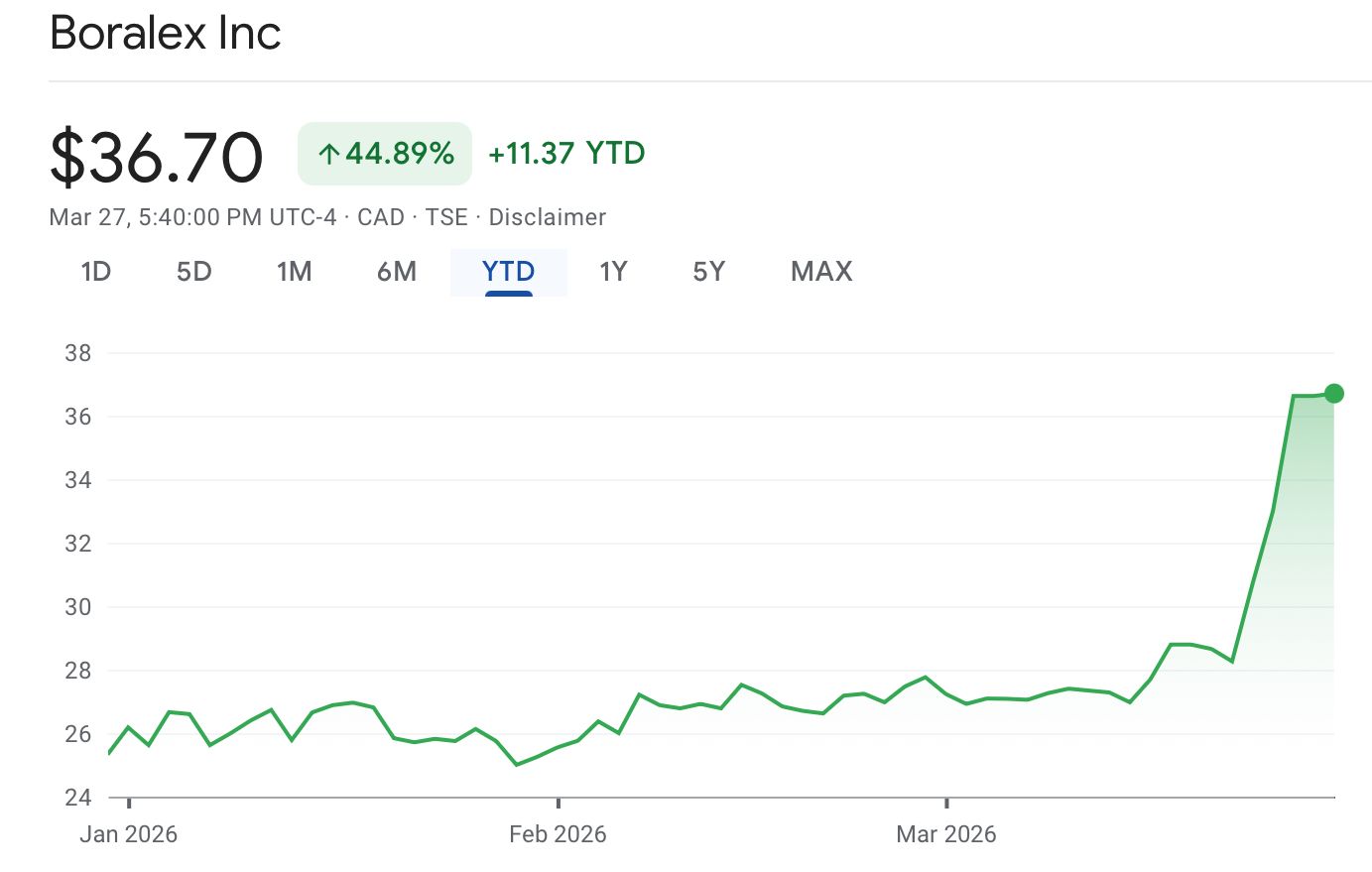

Brookfield Asset Management and Caisse de Dépôt et Placement du Québec (La Caisse) announced on March 25 that they have entered into a definitive agreement to acquire Boralex Inc. for C$37.25 per share in cash, implying a total equity value of approximately C$3.8 billion and a total enterprise value of approximately C$9.0 billion ($6.5 billion U.S.), including debt.

The offer represents a 31.8% premium to Boralex’s March 20 closing price, and a 36.4% premium to the 30-day VWAP preceding the first media report that the company had begun reviewing strategic alternatives. Boralex’s board unanimously approved the transaction. The deal is expected to close in Q4 2026.

La Caisse, already Boralex’s largest shareholder with approximately 15% of the outstanding shares, will vote in favor of the transaction and will make a post-closing investment resulting in a 30% pro forma ownership stake in the newly private company.

Brookfield, through its flagship infrastructure strategy and Brookfield Renewable Partners, will hold the remaining 70%. So the Quebec pension fund is going from 15% of a publicly-traded company to 30% of a private one, which is either a vote of extraordinary confidence or a sign that they’ve been waiting for exactly this structure for a long time. Possibly both.

Why go private? Boralex’s CEO Patrick Decostre said the company’s “strong pipeline” requires financing that being private will facilitate more efficiently, which, translated, means: as a public company, every time we need equity to fund development, we have to go back to a skeptical market that doesn’t want to hear about European wind farms right now. The company’s shares peaked above C$55 in early 2021, when investors were paying premium multiples for anything adjacent to “green” and “infrastructure.”

Now, AI companies and hyperscalers are clambering for power demand, bringing power companies back into favor once again.

Boralex was trading at less than half that level as of last week, not because the assets got worse — the wind still blows in France, the hydro facilities in Ontario still generate power on schedule — but because the macro backdrop moved against rate-sensitive yield vehicles. Classic infrastructure private equity hunting ground.

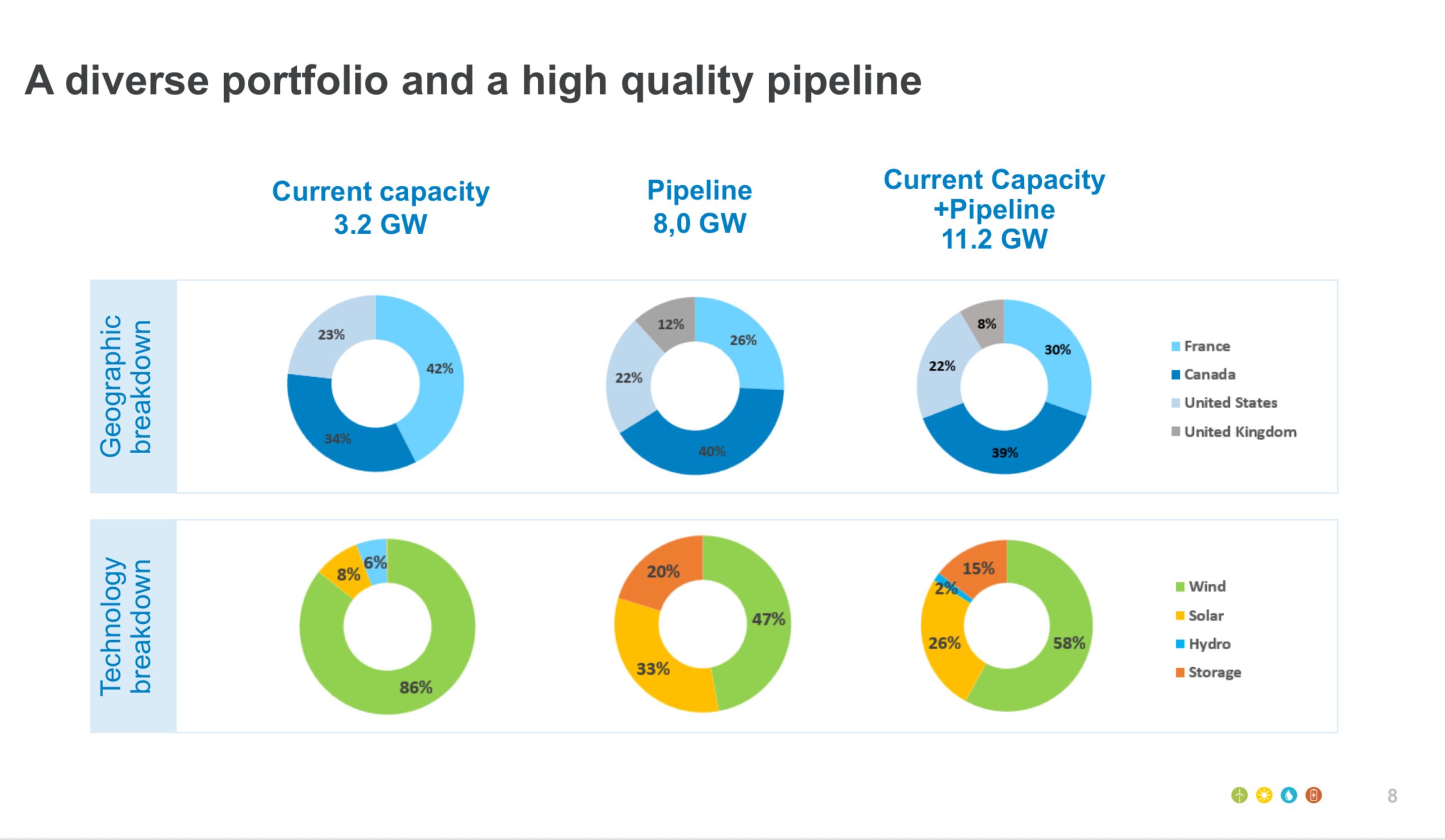

Boralex adds roughly four gigawatts of operating clean power capacity to Brookfield’s existing global fleet of 46 gigawatts, plus another eight gigawatts of development pipeline in Canada, France, the United States, and the United Kingdom.

The transaction is valued at ~13x 2026 EBITDA, reasonable for a high-quality renewable portfolio with long-term contracted revenue and inflation-linked tariffs in regulated European markets.

The deal is being funded by Brookfield Renewable Partners through its flagship infrastructure strategy. No bank financing details were disclosed, but given Brookfield’s balance sheet and La Caisse’s scale, the capital structure conversation was presumably brief.

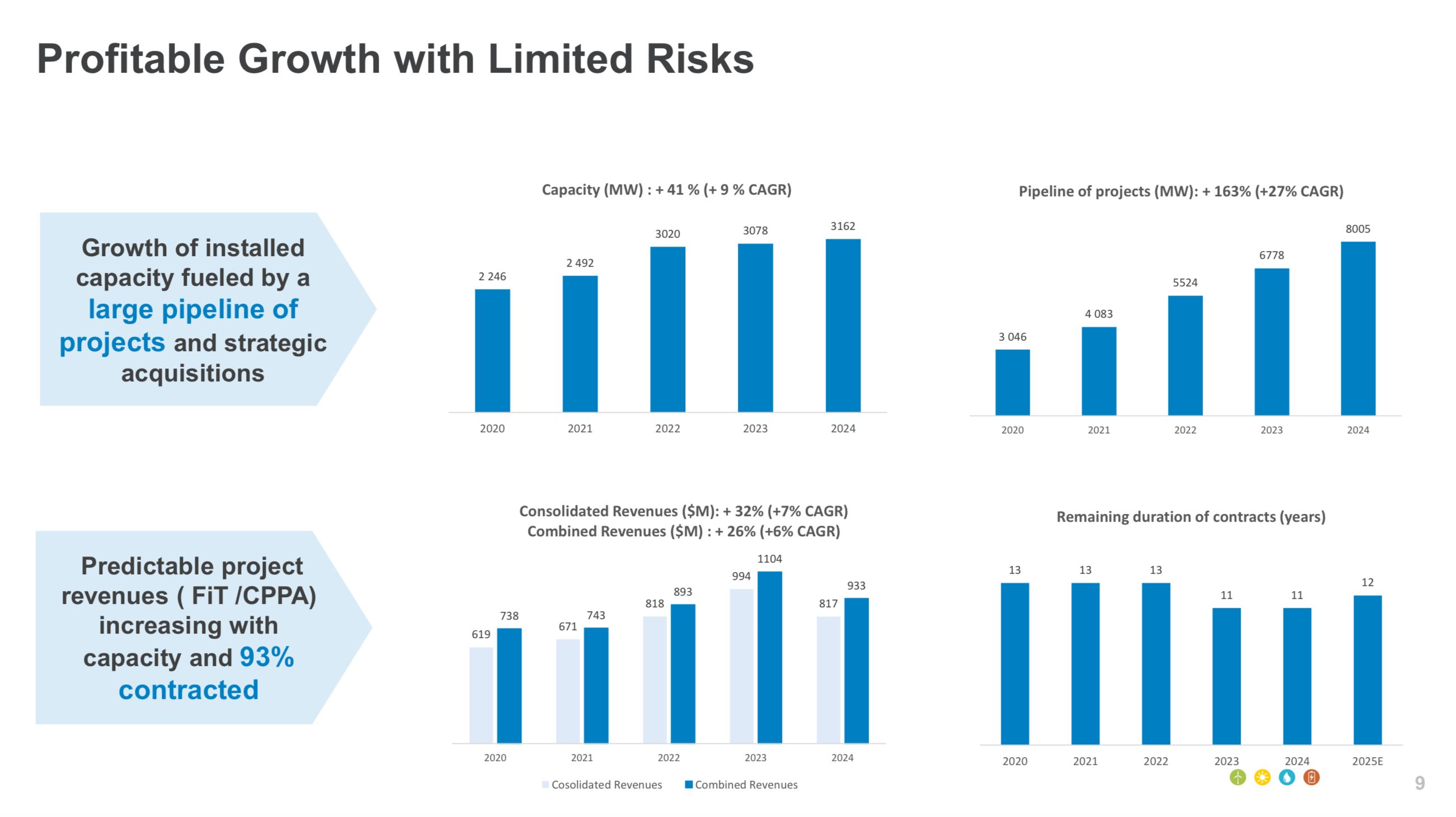

One detail worth noting: Boralex’s 2030 Strategic Plan targeted 6 GW of installed capacity by the end of this decade. As a public company, hitting that number was going to require regular trips back to equity markets in an environment where renewable energy stocks were being treated like a category error.

As a private company backed by Brookfield’s global development capabilities and La Caisse’s institutional firepower, the path is materially cleaner. Whether it actually gets to 6 GW is a question for 2030, but at least now they don’t have to explain their progress on a quarterly earnings call.

All we can say is bon chance to Brookfield and La Caisse and bravo to the Boralex team (and their shareholders).

INT’L DEAL OF THE MONTH

BP Says Auf Widershen to Germany

There is a version of corporate strategy where you sell everything that isn’t your core business, repeatedly raise your cost-savings target as you do it, and at some point the press releases start to feel less like strategy updates and more like a man furiously throwing things overboard to keep a boat afloat.

BP has been writing that press release for about fourteen months.

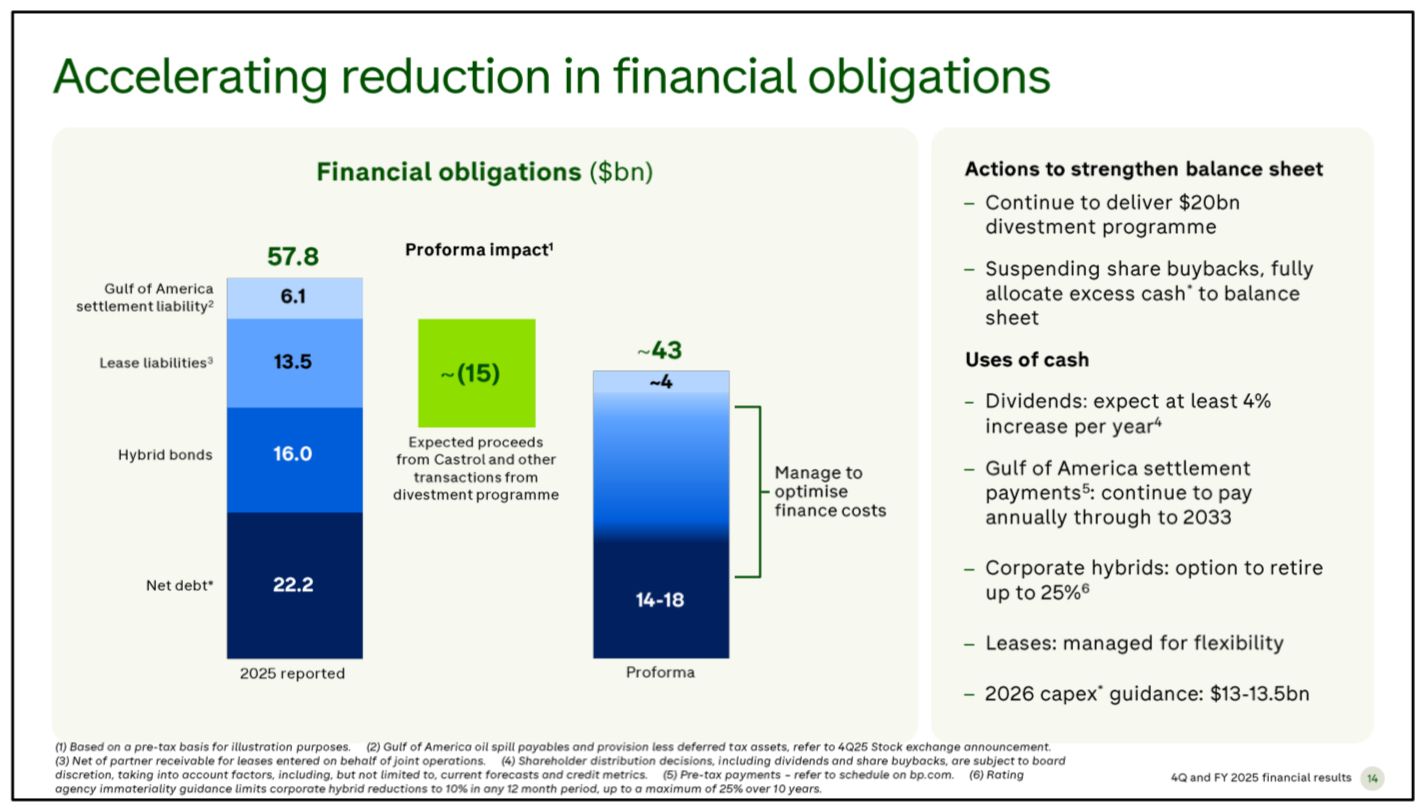

On March 19, BP announced it has entered into a definitive agreement to sell its Gelsenkirchen refinery and associated businesses to Klesch Group, an independent European refiner, for an undisclosed price. Which means, one party was certainly not thrilled about the price.

The refinery complex — operating two sites in Horst and Scholven in Germany’s Ruhr region under the legal entity Ruhr Oel GmbH — processes approximately 12 million tonnes of crude oil per year, with a crude distillation capacity of 265,000 barrels per day.

It produces petrol, diesel, jet fuel, heating oil, and more than 50 other products for the European chemical industry. About 1,800 employees are expected to transfer to Klesch upon completion, along with offtake arrangements that allow BP to continue sourcing ground fuels, aviation fuel, and coke from the site.

The undisclosed price is doing a lot of work in that announcement. BP invested approximately $2 billion in modernizing the Gelsenkirchen site since 2017 — upgrading steam and power infrastructure, distributed control systems, and tank farm and pipeline refurbishments. BP’s underlying operating expenditure associated with the site runs around $1 billion per year.

Disposing of that $1 billion annual cost base is what allowed BP to raise its 2027 structural cost reduction target for the third time in fourteen months — to a range of $6.5 to $7.5 billion, up from its original $4 to $5 billion target set in February 2025.

The progression, if you’re keeping a tally at home: $4-5B → $5.5-6.5B → $6.5-$7.5B.

Each increase comes with a refinery sale. At this rate, by 2027 BP will have announced $15 billion in savings and will own exclusively a headquarters, a logo, and a very good sustainability report.

Klesch Group, the buyer, is a Geneva-based independent European refiner controlled by chairman A. Gary Klesch. The company’s existing portfolio includes the Heide Refinery in Germany and the Kalundborg Refinery in Denmark, the first acquired from Shell in 2010, the second from Equinor in 2022.

There is a pattern here: Klesch buys high-quality European refinery assets from oil majors who have decided they are no longer in the European refinery business, then runs them.

This is the third time that playbook has worked. It will almost certainly not be the last, given how many oil majors are currently in the process of deciding they are no longer in the European refinery business.

Patrick Wendeler, BP’s head of country for Germany, offered a statement that was, by corporate press release standards, almost poignant: “We have a long history of operating successful assets and brands in Germany, and we are deeply grateful for the refinery’s decades of contribution to our business.”

Translation: so long, farewell, auf wiedershen, goodbye - but, we would like to be remembered kindly.

The transaction is expected to close in the second half of 2026, subject to regulatory and governmental approvals. The deal is free-cash-flow accretive for BP based on historical performance, which, again, is doing quite a bit of euphemistic heavy lifting given the $1 billion annual cost structure that is about to leave the books.

BP has now announced or completed more than $11 billion of its planned $20 billion divestment program.

Whether the strategy ultimately works, selling everything at sufficient speed and raising your cost savings target enough times eventually fixes BP’s underlying return on capital problem, is a question above this newsletter’s pay grade.

But credit where it’s due: they are executing. Every quarter, something gets sold. Every sale comes with a press release. Every press release comes with a higher savings target. It is, in its own way, a beautiful system.

NEWS ROUNDUP

Top Reads

What'd you think of today's newsletter? |